- The Breakdown

- Posts

- 🟪 Crypto investing charts

Brought to you by:

“A cynic is a man who knows the price of everything, and the value of nothing.”

— Oscar Wilde

Crypto investing charts

Crypto prices have been floundering lately and here’s why I think that’s good news: We can’t expect President Trump, Michael Saylor and Larry Fink to drag us higher forever.

For the crypto industry to hit escape velocity, it will have to attract users, not just promoters.

Fortunately, crypto is now for the first time consistently producing real revenue: Real people are paying real money to use the chains.

A cynic would say this revenue is low quality because most of it is derived from memecoin trading and how long can that possibly last?

I don’t know, but people are paying a lot to trade memecoins and I take that as evidence that they’ll eventually be willing to pay for other onchain things, too.

If nothing else, the real revenue that crypto now generates lets us start talking about tokens in the same way we talk about stocks.

Tokens have fundamentals, at last.

It’s still early though: If, as is often said, valuing stocks is more art than science, then we're probably still at the finger-painting stage of valuing tokens.

But we’re past the stage where it was only narratives in crypto — there are numbers, too — and I consider that important progress.

If nothing else, enough users are now paying to do enough things onchain that the best way to stay on top of what's going on may be to follow the numbers — in convenient chart form, of course.

So, let’s see what’s been going on.

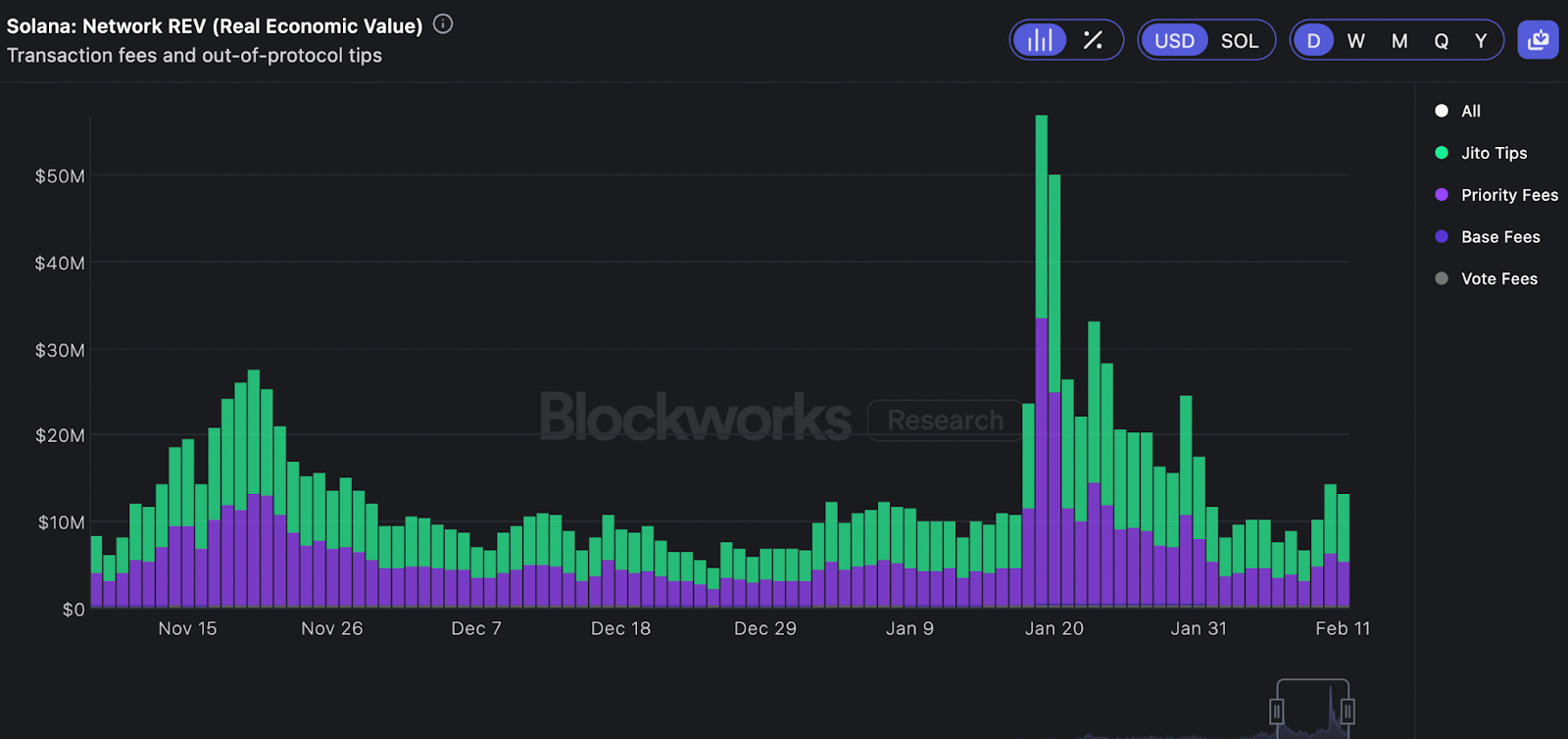

REVing down?

This bar chart shows that Solana generates nearly all of its “Real Economic Value” (REV) in tips (in green) and priority fees (in purple), the combination of which is essentially how much users are willing to pay to get their transaction onchain. REV is down from its peaks in November (when the US elected its first crypto president) and January (when said president issued a memecoin), but the base level of demand for Solana blockspace seems pretty high.

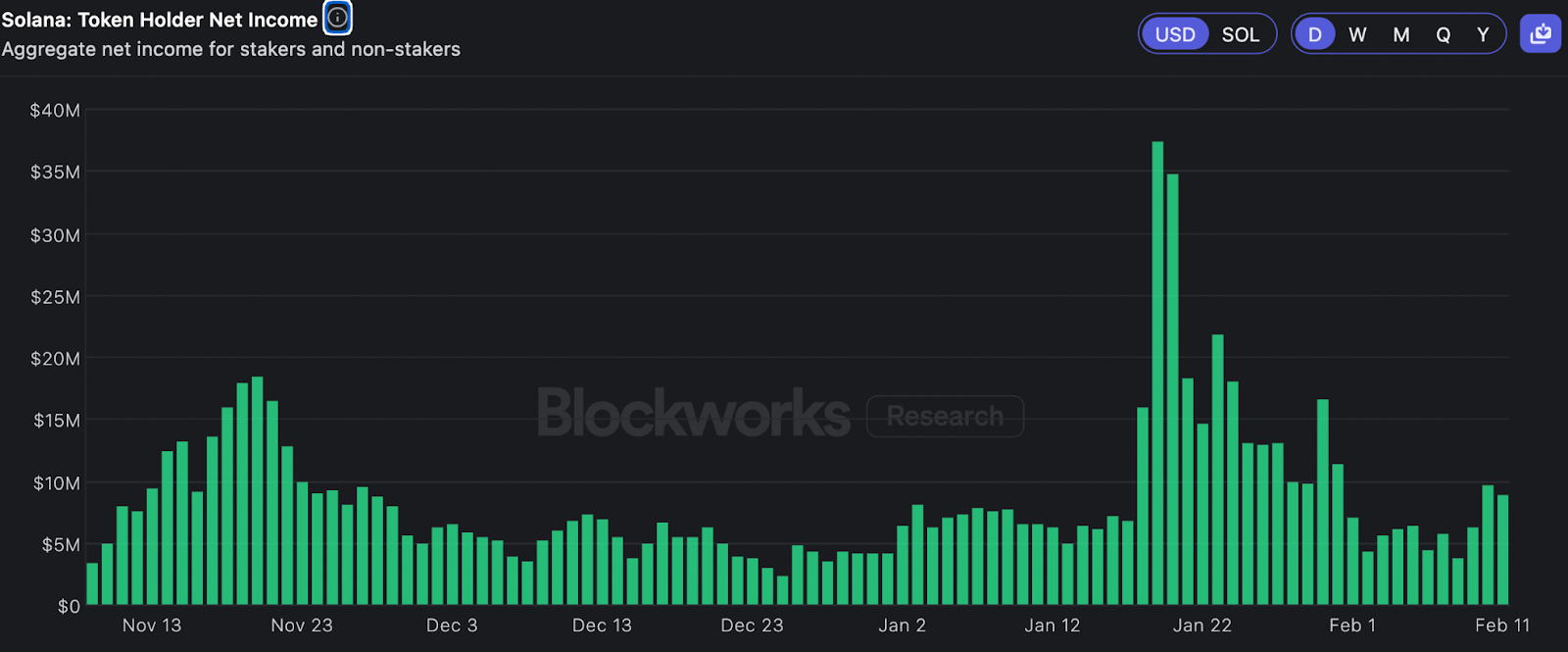

Crypto’s P/E ratio:

Blockworks Research also charts Solana’s “Total Holder Net Income,” which subtracts “operator payments” from REV. If you strip out the two one-off events in November and January, Solana is doing about $9 million per day in net income, which annualizes to $2.3 billion. That would put SOL on about 40x earnings — which will seem cheap if you think memecoins are here to stay, and expensive if you don’t.

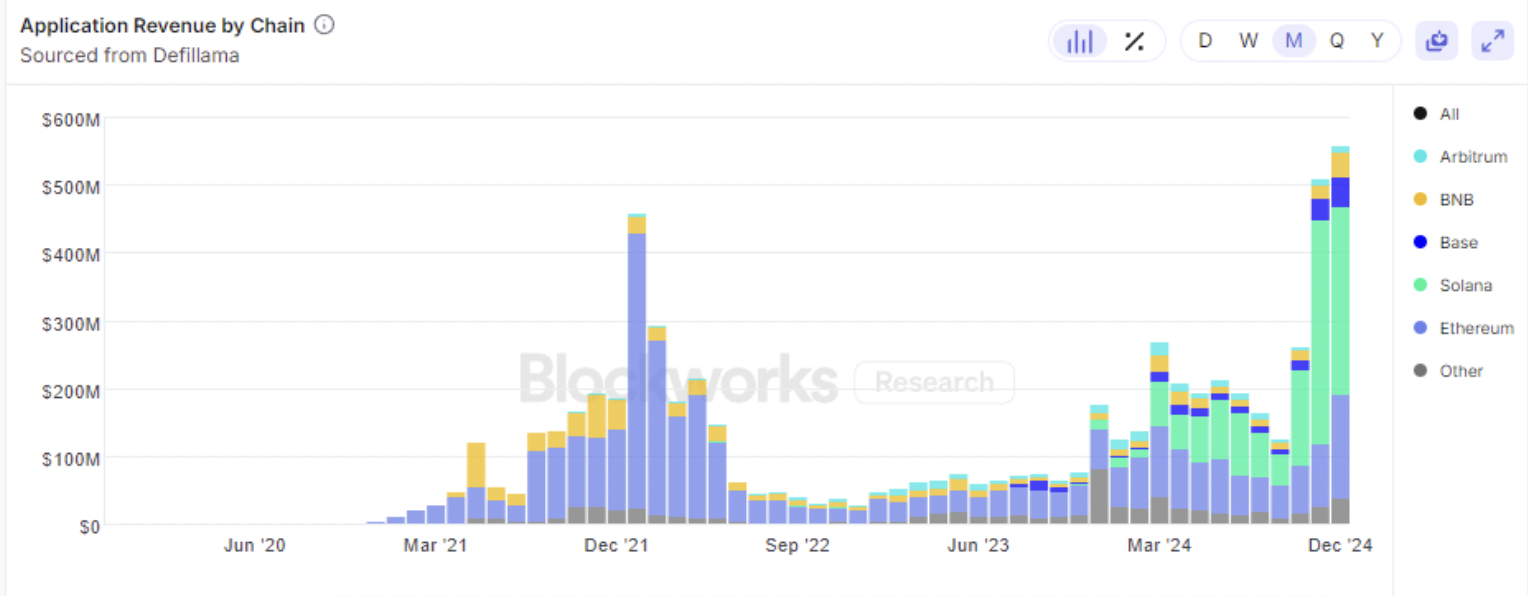

Application revenues:

Blockworks’ Dan Smith notes that applications built on Solana generated $751 million of revenue in Q4, vs. $314 million for Ethereum-based applications. Nearly a third of that Solana total is attributable to the memecoin platform pump.fun, however — which makes it either very low quality or very high, depending again on your opinion of memecoins.

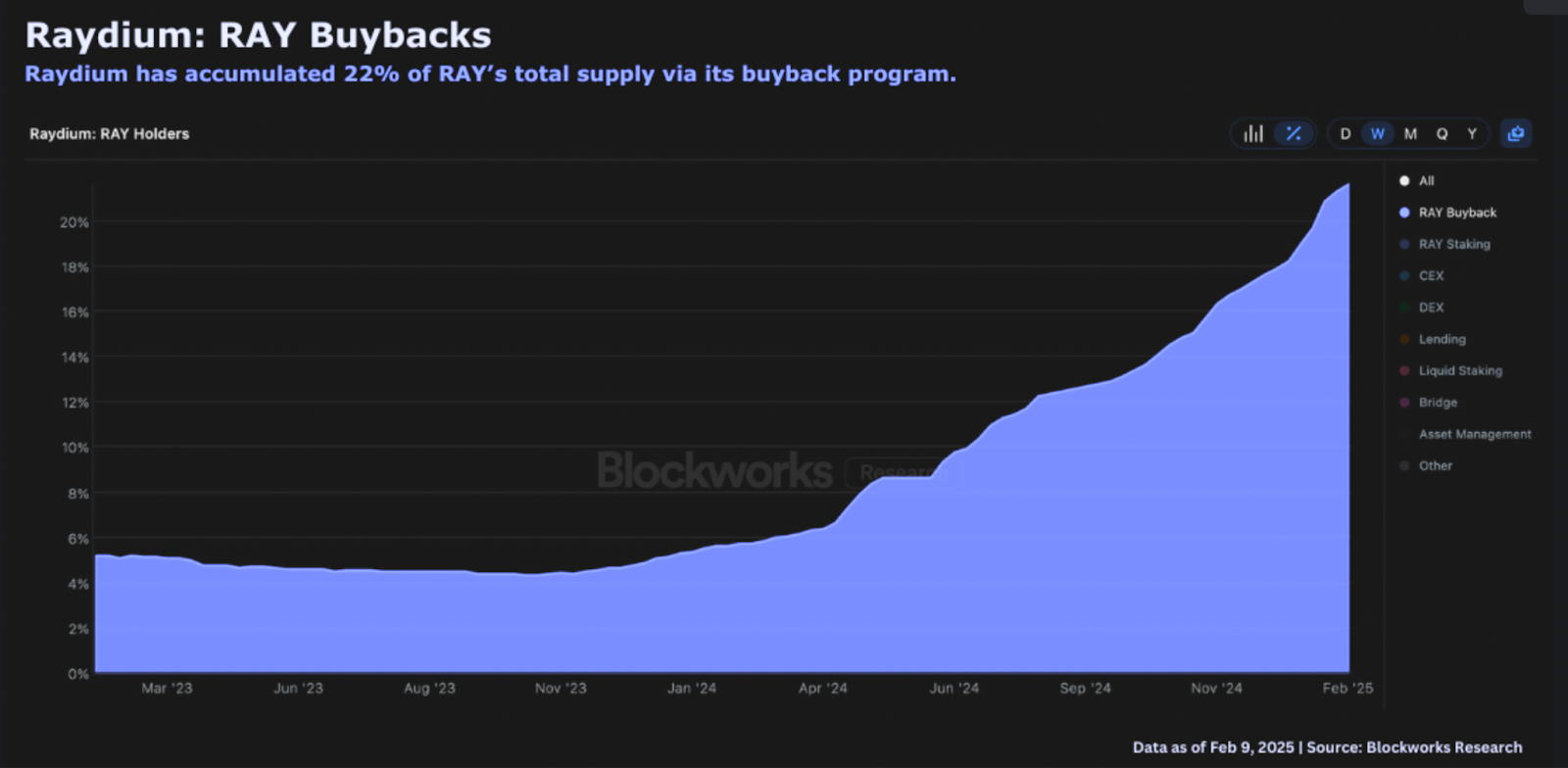

Token buybacks:

Blockworks’ Marc Arjoon notes that the second most profitable crypto application, Raydium, has now bought back 22% of its token's circulating supply (worth about $307 million at the current price of RAY). That, too, is mostly thanks to memecoins (and mostly memecoins from pump.fun) — so, if you’re buying SOL on its reasonable 40x multiple, or RAY for its prodigious cash flow, know that most of your eggs are in the memecoin basket.

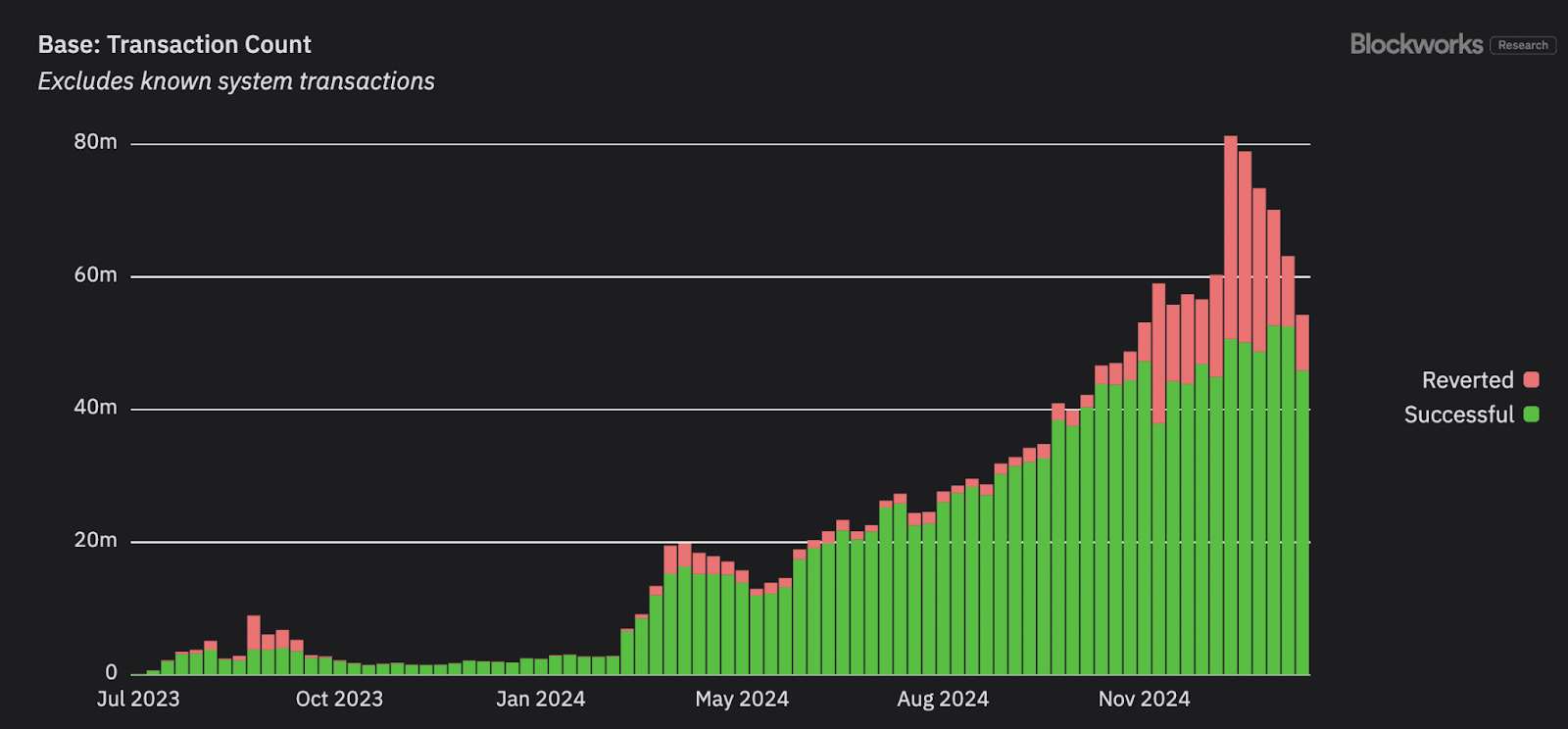

The layer-2 champion:

Base collected $12.1 million of fees over the last month, well ahead of the second-place L2, Arbitrum, at just $3 million. The above chart of weekly transactions on Base shows that activity peaked with the mini-bubble in AI agent coins.

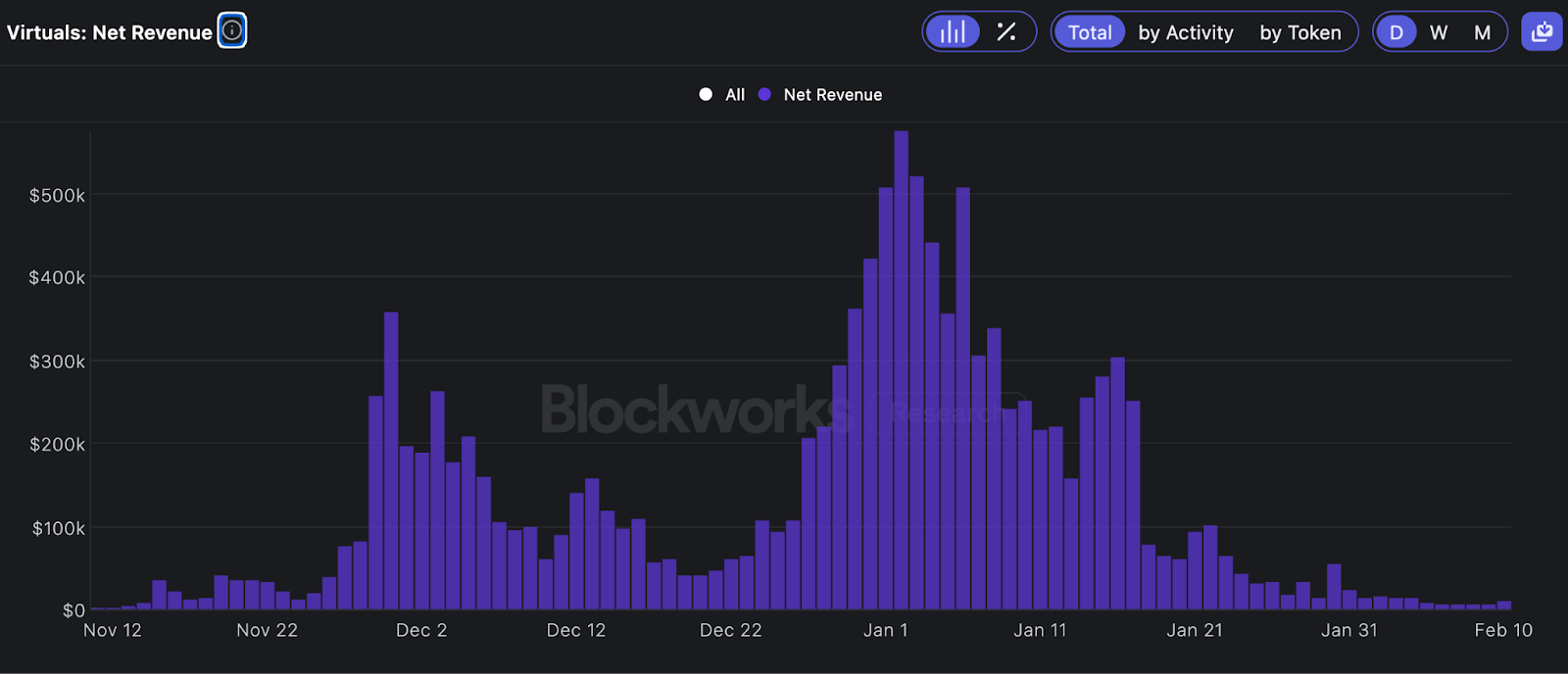

The mini-bubble:

People are no longer paying to create semi-autonomous AI agents with the Virtuals protocol. The bubbles come and go quickly in crypto, which makes forward-looking forecasts nearly impossible.

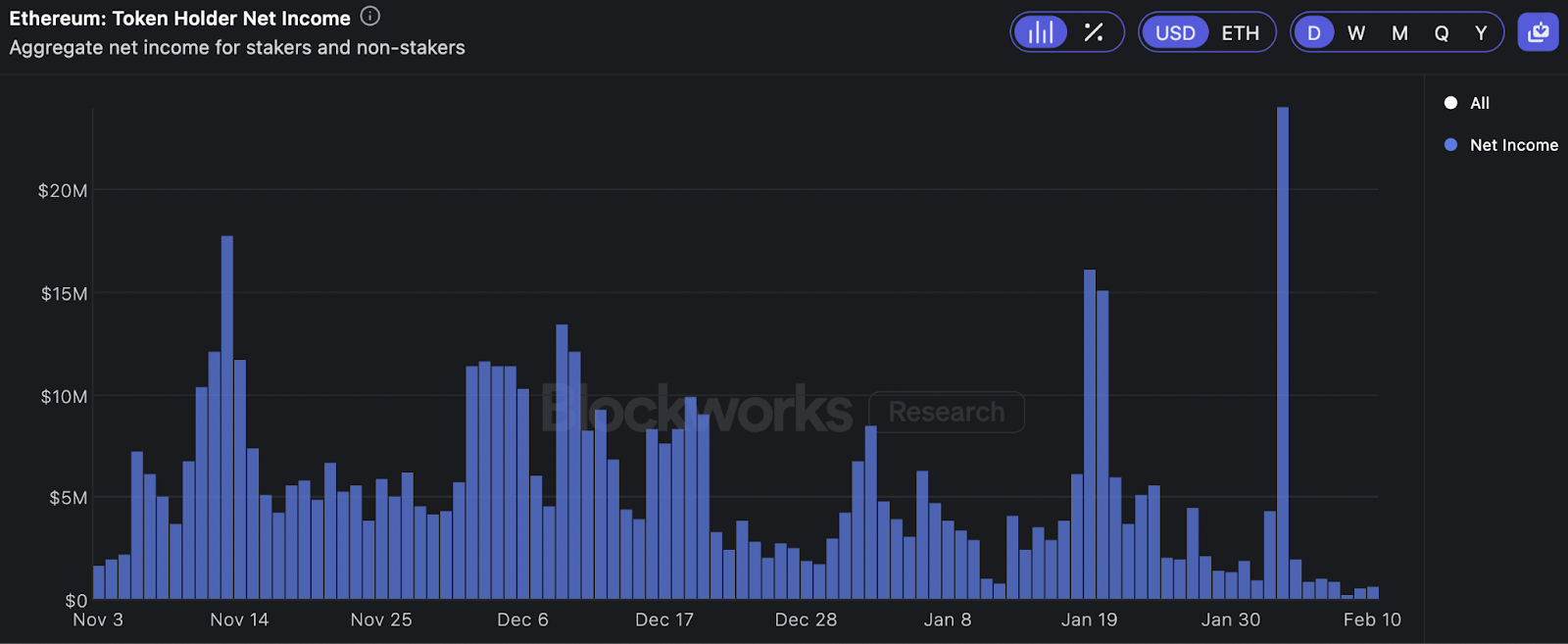

People are paying to use Ethereum, too:

Per Blockworks’ data, ETH token holders earned $663,000 of net income yesterday. That annualizes to $240 million, which is a lot, in absolute terms — and welcome evidence that people remain willing to pay for access to Ethereum. Relative to ETH’s $313 billion market cap, however, it’s not a lot: It puts ETH on a P/E ratio of 1,289x. (And, yes, annualizing one day of earnings is something you’re allowed to do in crypto. Try it, it’s fun!)

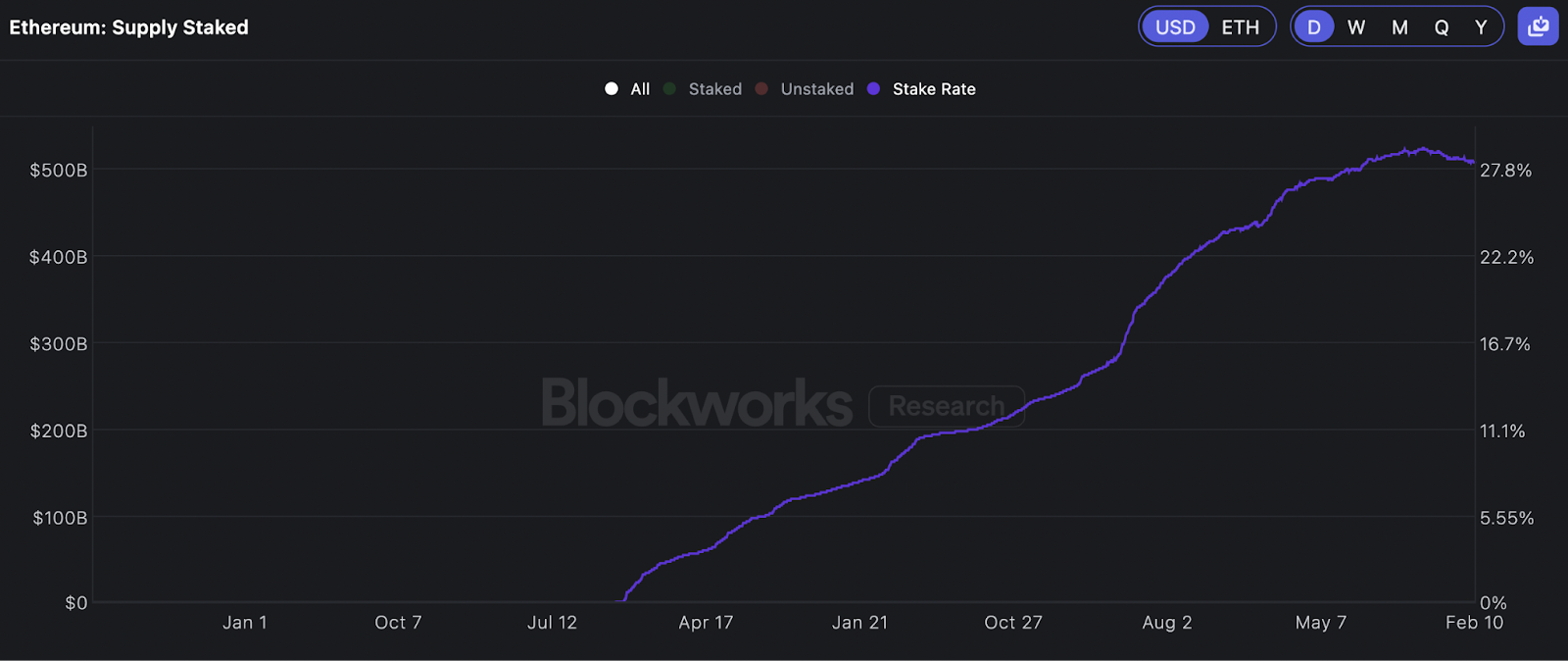

Unstaking:

For the first time, the percentage of ETH staked is trending lower. The stake rate is only down one percentage point so far, but the change of trend might suggest that some long-term holders are throwing in the towel on ETH after its long stretch of underperformance.

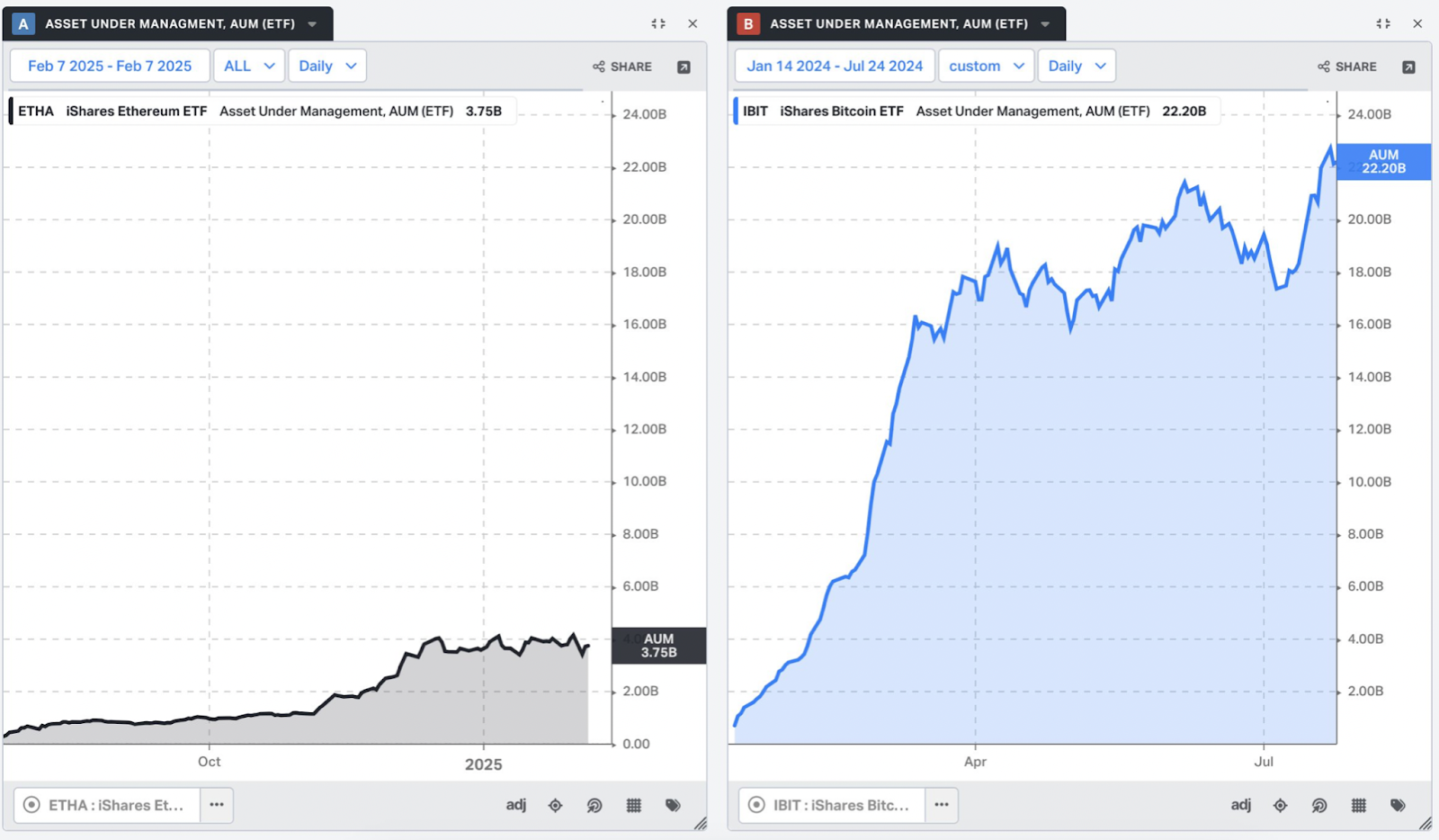

ETF flows:

Source: Koyfin

The AUM of ether ETFs vs. bitcoin ETFs is roughly proportionate to their market capitalizations, but the trend seems to favor bitcoin.

Non-crypto revenue:

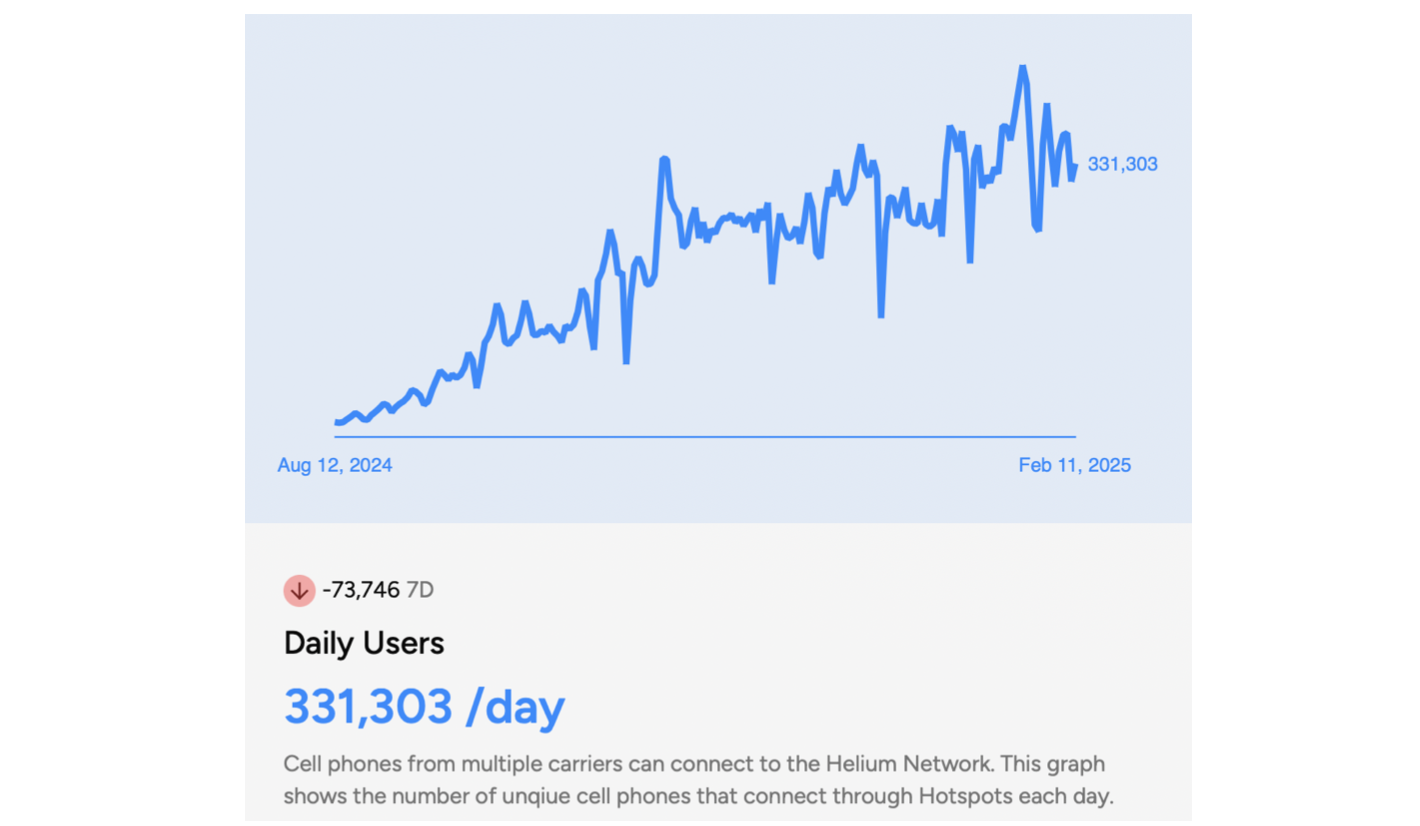

We’re still looking for a breakout crypto application not related to crypto, and Helium’s DePIN cell phone service is still the one that gets mentioned the most. The trend looks pretty good, but it still hasn’t quite caught on (T-Mobile has 130 million subscribers, by comparison).

Digital map demand:

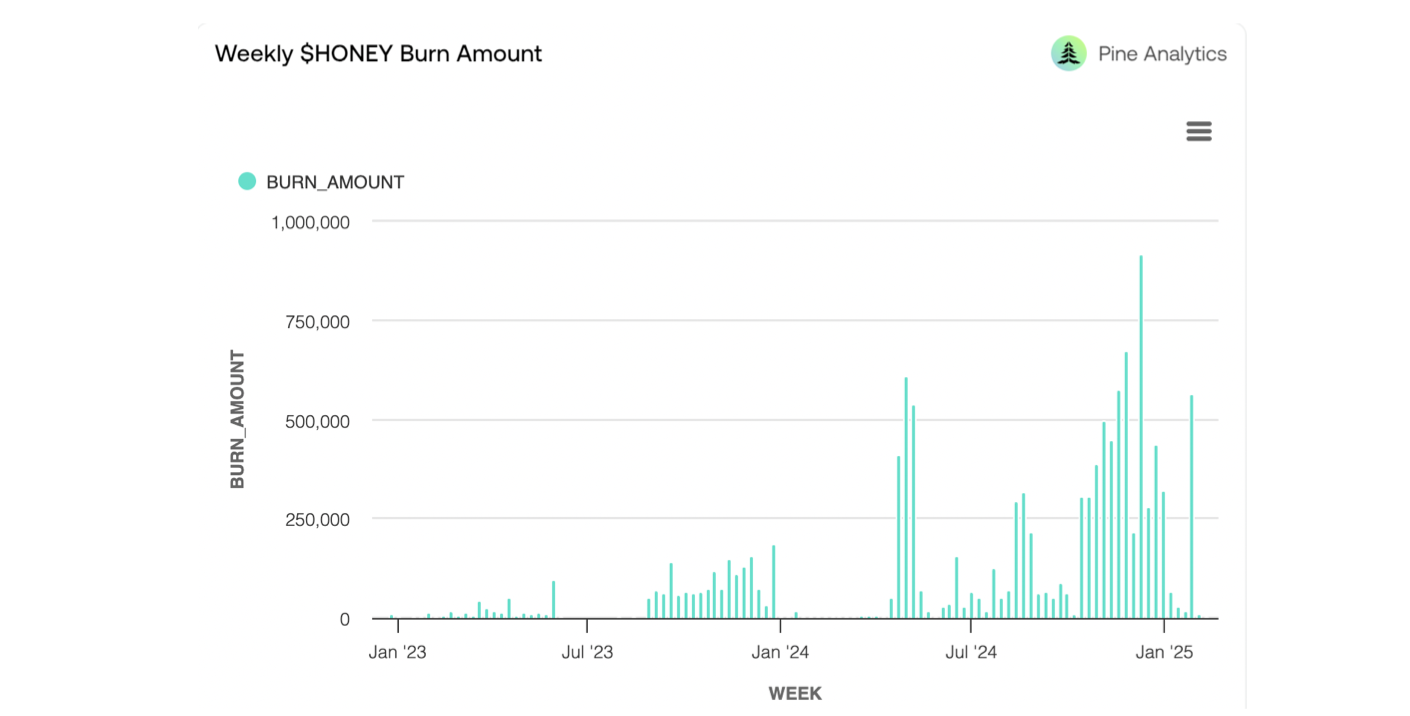

DePIN’s other most-cited champion, Hivemapper, is doing well selling digital map data, but maybe not well enough to get traditional investors interested. At the current rate of burn, Hivemapper’s HONEY token trades on about 230x annualized revenue.

Crypto compute:

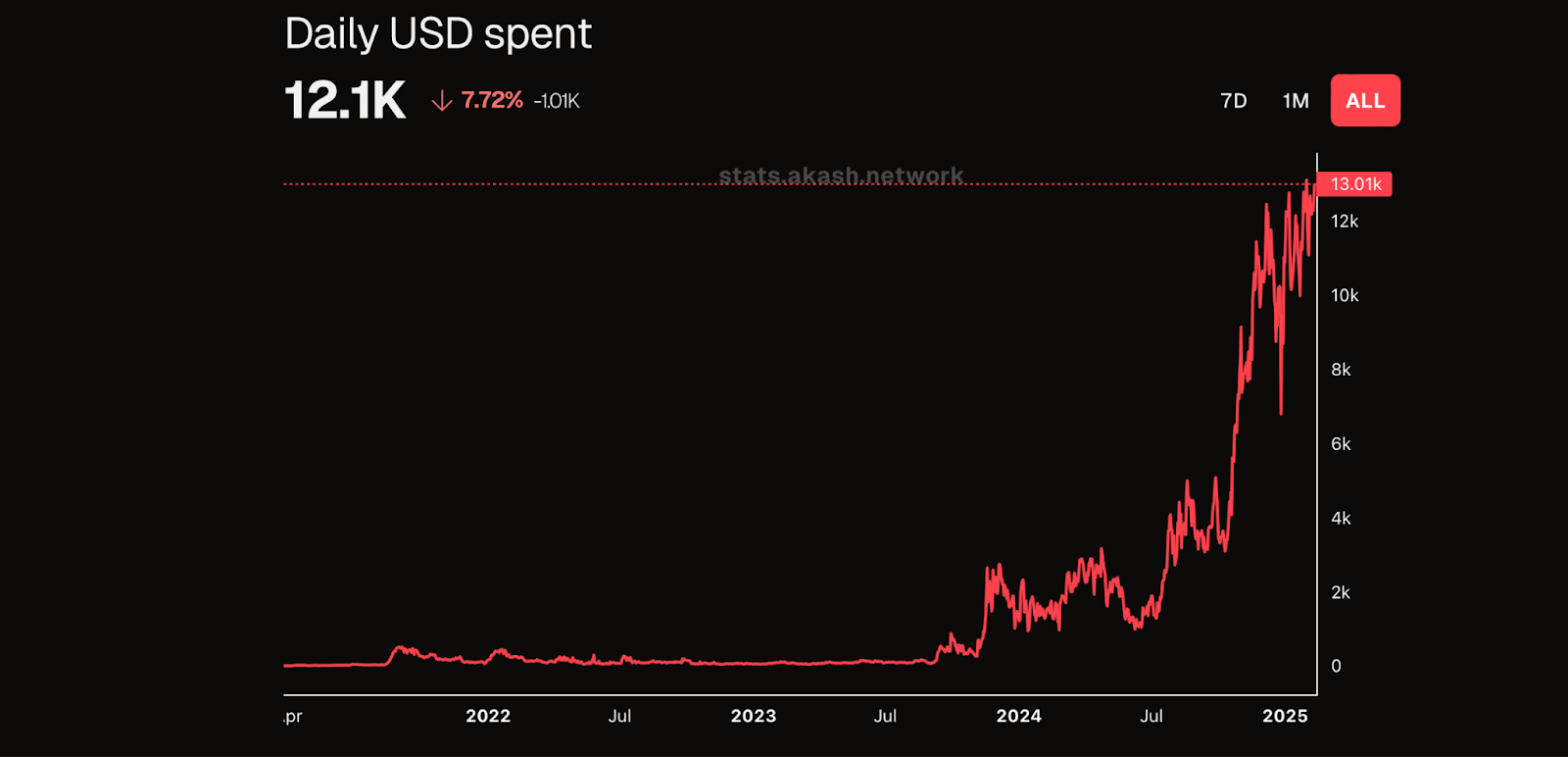

This chart of dollars spent on Akash’s marketplace for decentralized computing power is particularly encouraging for those of us hoping that crypto will generate more revenue unrelated to crypto. But it’s also pretty modest, annualizing to $4.4 million (vs. AKT’s $490 million market cap).

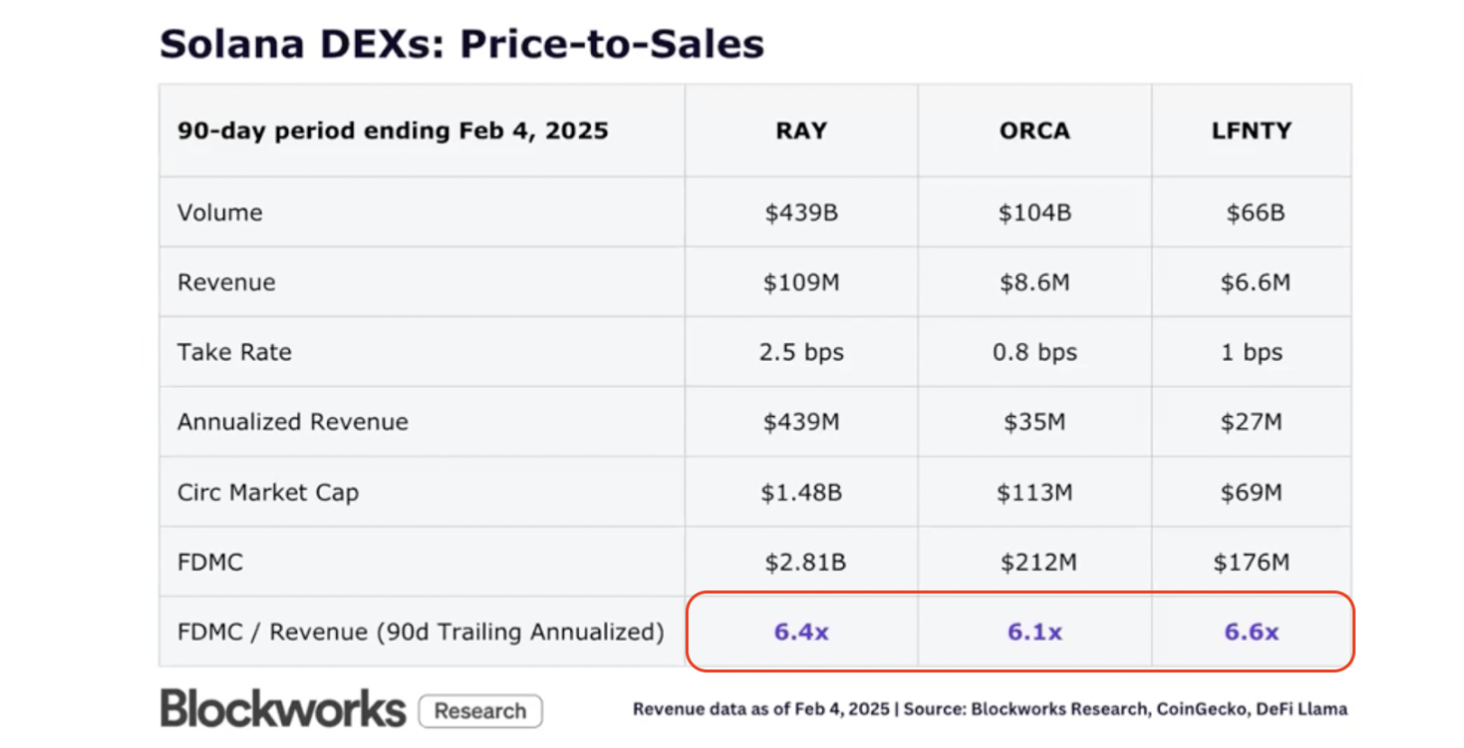

Efficient crypto hypothesis?

Here’s my closing argument for why we should take crypto fundamentals seriously: Three major Solana DEXs trade at valuation multiples within half a point of each other, which looks weirdly efficient — even by TradFi standards.

And maybe cheap, too?

In equities, a 6x multiple would be considered deep value for a non-dying business.

But we’re still painting with our fingers in crypto and the revenue we have to work with is too new and volatile to make a serious forecast of how things might look even a few months out.

The above multiples are based on trailing revenue, as most crypto metrics are, so forward multiples remain anyone’s guess.

But that’s what makes crypto investing fun — like finger painting!

More importantly, all this data gets us closer to not only knowing the price of crypto tokens, but their value, too.

Brought to you by:

Morpho is the first and only DeFi protocol integrated by Coinbase.

As the go-to infrastructure for onchain loans, Morpho’s immutable code sets the gold standard for decentralization, giving builders full ownership and control. Leverage Morpho’s flexibility to create lending and borrowing solutions tailored precisely to your users’ needs.

Try Morpho today.

The Credit Cycle Is Just Getting Started

Andreas Steno Larsen joins the show to discuss the outlook for liquidity and expectations around inflation. Get his thoughts on Powell’s QE comments and the idiosyncratic drivers of gold.

Listen to Forward Guidance on Spotify, Apple Podcasts or YouTube.

The lines between crypto, traditional finance, and policy aren’t blurring, they’re disappearing. The people making that happen? They’re speaking at DAS NYC.

Cathie Wood (ARK Invest) on the seismic shift in capital allocation and why the biggest bets are still ahead.

Caitlin Long (Custodia Bank) on the battle for crypto-friendly banking and why regulators are playing catch up.

Dan Tapiero (1RT & 10T Holdings) on the real institutional play — where the biggest money is quietly positioning.

This is where the people with real skin in the game lay it all out.

📅 March 18-20 | NYC

1) Fun fact: there are ~280 payment companies today building on cryptorails (!)

I've written a piece explaining the current financial system, major use cases for cryptorails, adoption challenges they're facing, and what the future might look like.

paragraph.xyz/@archetype/cry…

— Dmitriy Berenzon (@dberenzon)

4:46 PM • Feb 12, 2025

TIA staking rewards should be locked when staking locked tokens

This CIP fixes that

To date, unlocked staking rewards have been the default for PoS chains from Sui and Aptos to practically every Cosmos chain including Celestia.

If implemented, this CIP would make Celestia… x.com/i/web/status/1…

— Nick White 🦣 (@nickwh8te)

8:28 PM • Feb 12, 2025