- The Breakdown

- Posts

- 🟪 The Curious Case of Crypto’s Only Normal Valuation

🟪 The Curious Case of Crypto’s Only Normal Valuation

MakerDAO is complicated: subDAOs, the Endgame, PSM, DSR, crypto vaults, stability fees... all of the core terms that describe the MakerDAO protocol have been invented to describe the MakerDAO protocol.

This issue is brought to you by:

“A bank is a place that will lend you money if you can prove that you don't need it.”

The Curious Case of Crypto’s Only Normal Valuation

MakerDAO is complicated: subDAOs, the Endgame, PSM, DSR, crypto vaults, stability fees… all of the core terms that describe the MakerDAO protocol have been invented to describe the MakerDAO protocol.

The underlying business, however, is not complicated: It’s a bank.

Maker creates deposits, accepts collateral, extends loans and collects interest in much the same way a regular bank does, with a crypto twist but in each case that necessitates the coining of all that novel terminology.

The outputs, however, look surprisingly familiar — as I’ve learned from the new Blockworks Research dashboard that presents Maker’s business in a form that is both amazingly detailed and easily digestible.

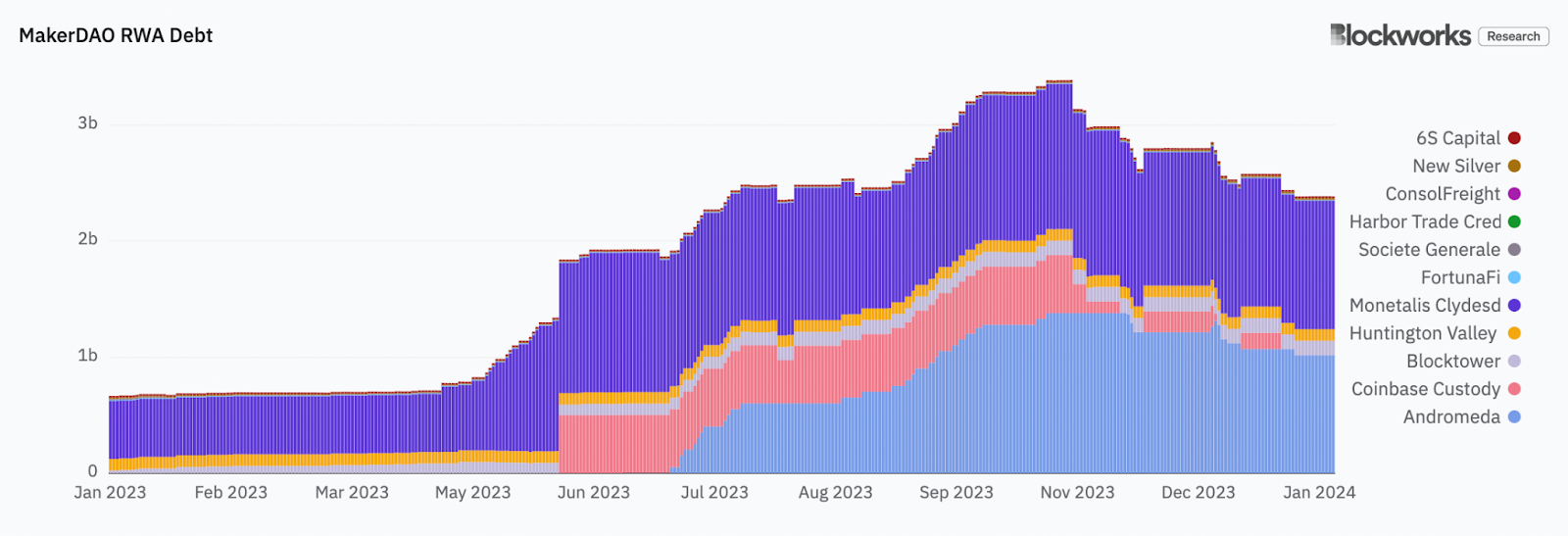

Maker’s shift into “real world assets” is evident in the dashboard’s chart of its surging revenue. The income statement created for the dashboard looks just like what the SEC would expect to find in a 10-K filing, and the chart of Maker’s “PSM balances” illustrates how the protocol operates on a reserve model, just like a traditional bank.

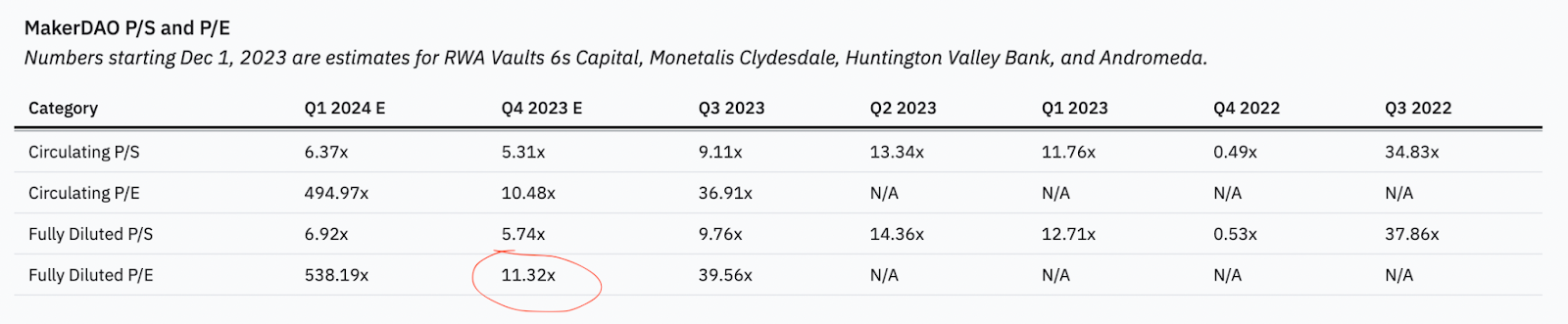

Weirdly, the most familiar thing on the dashboard — the valuation table — happens to also be the most unexpected thing.

Unexpected because Maker’s valuation looks so incredibly normal.

MakerDAO’s MKR token trades on 11x earnings — just like a regular bank!

11x earnings is a multiple that would feel right at home in TradFi, and that is the last thing I was expecting from Maker given that 1) Maker is not a normal bank and 2) crypto doesn’t do normal multiples.

JPMorgan, Bank of America and Wells Fargo, for example, all trade on about 10x earnings.

I’m not sure what to think about this.

It might mean that crypto markets are efficiently pricing a mature business in the same way it would be priced in equities markets — or that crypto markets are underpricing the one digital asset that has both real revenue and close comparators in TradFi.

But crypto markets are not known for their efficiency — nor for a propensity to underprice things.

So either conclusion would be equally surprising to me.

Which is good: Surprising means there’s opportunity there — but I couldn’t tell you in which direction.

Crypto natives, I expect, will see opportunity to the upside.

They’ll imagine sDAI (Maker’s yield bearing stablecoin) becoming the collateral asset of choice in DeFi; they’ll expect growing demand for loans against appreciating crypto collateral; and they’ll love the crypto-centric roadmap in “the Endgame” that includes a 1 for 24,000 stock split — the best stock split ever!

TradFi types are likely to see opportunity to the downside.

They may not have an opinion on the prospects of sDAI as DeFi collateral and they probably won’t read all the way through the Endgame roadmap — but they won’t think they have to.

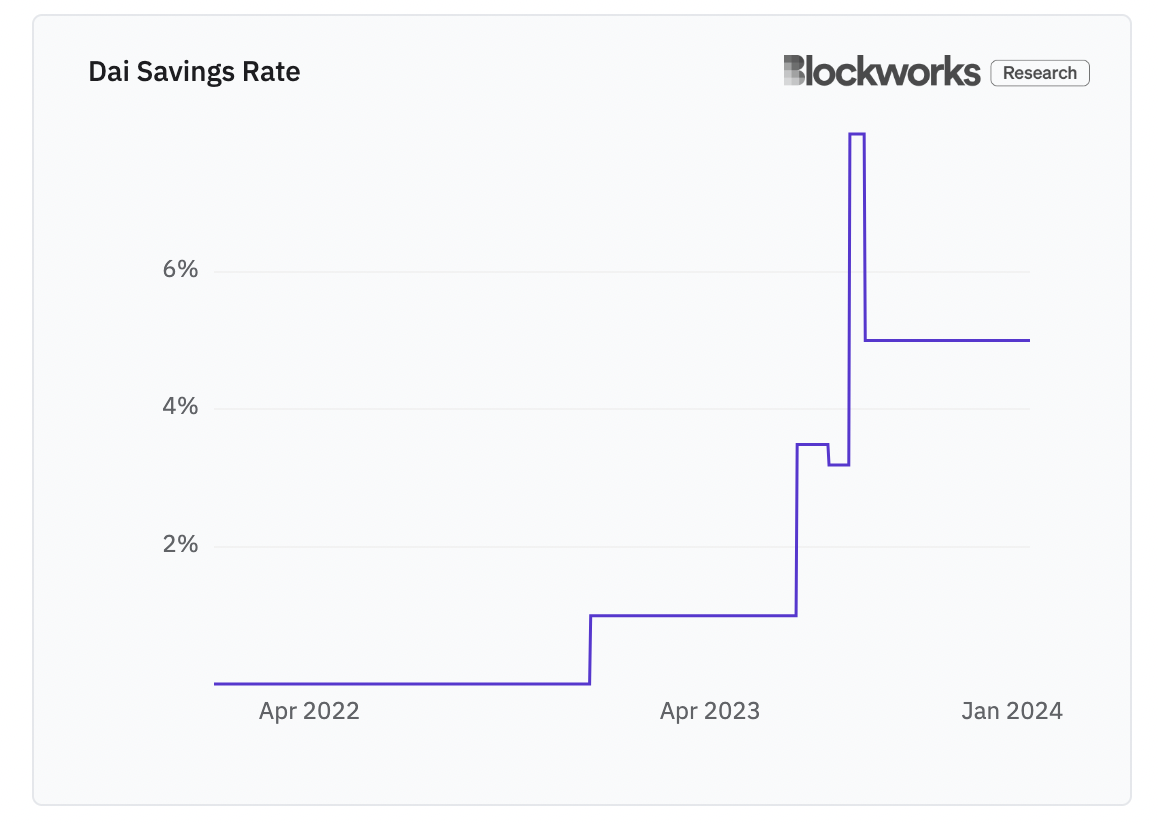

Instead, they will take one look at the dashboard’s “DAI savings rate” (which shows what Maker is paying to attract deposits) and decide that Maker is not a good bank.

TradFi types will assume that a bank paying 5% to attract deposits is either 1) taking too much risk or 2) struggling to find customers.

In Maker’s case, both are possible, as it’s not entirely clear what risks they’re taking or where they’ll find new customers — Maker offers fully collateralized crypto loans, which makes for a limited pool of potential customers.

(Lending to people who don’t need the money, as Bob Hope says, rather than to the much larger market of people who do need the money, as George Bailey did.)

I don’t think anyone from TradFi would pay 11x earnings for a bank of that sort — not when they can buy JPMorgan (which pays almost nothing for its deposits) for 10x earnings.

This does not, however, solve the mystery of Maker’s valuation.

The crypto market doesn't generally need TradFi investors to make tokens trade at sky-high valuations — we are perfectly capable of wildly overpaying for everything on our own.

So why aren’t we doing the same for Maker?

Perhaps because it's not crypto enough.

It’s not a wonderful life

There’s a lot of trust involved in the Maker’s business model.

Investors have to trust that the off-chain entities tracked on the Blockwork’s dashboard will invest Maker’s deposits wisely, conscientiously keep track of the revenue earned and reliably return the agreed share of revenue to Maker.

This is normal in TradFi — trust is what the traditional banking system is built on.

But it’s not what crypto investors are here for — trust is the very risk that crypto is designed to eliminate and Maker may be doing the opposite.

The narrative behind Maker’s surging revenue is that the protocol is “bringing real-world assets on-chain” — but I think it’s at least as accurate to say that what Maker is bringing on-chain is real-world risks.

If you’ve swapped your ETH for DAI, for example, you’ve exchanged mostly on-chain risk (something going wrong in the smart contracts) for mostly off-chain risk (something going wrong with Maker’s real-world borrowers).

There is, of course, a cohort of people that are happy with that trade-off (there is $5.3 billion in DAI outstanding, after all) — people willing to accept those risks in return for holding the best attempt at a decentralized stablecoin with a money-market-like yield.

Maker may be an elaborate, inefficient and only partly decentralized way to deliver off-chain yield to on-chain investors, but there’s a market for that (those who can’t pass KYC, for starters). And that market might be growing (holding the largest centralized stablecoin, Tether, increasingly comes with the risk of having your funds frozen).

A TradFi person will see Maker’s structure as a regulatory arbitrage and steer clear, possibly at any valuation.

But a crypto person may see the same regulatory arbitrage and think that’s a good and growing market opportunity.

Maker’s multiple suggests to me that, as an investment, it’s stuck somewhere in the middle.

This issue is brought to you by:

Arbitrum is the leading Ethereum Layer 2 scaling solution, home to over 600+ applications.

Arbitrum allows you to interact with Ethereum the way it was meant to be - with lower fees and faster transactions. Whether you're exploring the leading DeFi ecosystem, the strong infrastructure options, a flourishing NFT and creator ecosystem, and a rapidly growing gaming hub, the Arbiturm ecosystem has a solution for you.

Top Stories

Electric Capital finds veteran Web3 devs are on the rise — Read

Jamie Dimon is crypto’s most boring villain — Read

BlackRock bitcoin ETF raking in flows as GBTC continues to bleed assets — Read

Spot bitcoin ETF issuer VanEck to shutter BTC futures fund — Read

Mercado Bitcoin starts 2024 with listing of TRON network’s native token: TRX (Sponsored) — Read

We're Watching

This week, Jonah Van Bourg Director at Onyx & Former Global Head of Trading at DRW joins the show for a discussion on his 2024 outlook for both commodity and crypto markets. We deep dive into Jonah's Bitcoin thesis, the U.S debt end game & the outlook for an Ethereum ETF in 2024 & beyond. To hear all this & more, you'll have to tune in!

We’re Hosting

Happening Tomorrow: Why a Spot ETF is a Game-Changer for Ethereum

Discover why a spot ETF is a game-changer for Ethereum, opening new avenues for accessibility, liquidity, and investor participation. Plus, we’ll discuss the exciting possibility of staking and yield strategies within ETFs and how institutions can use ETH staking derivatives.

Daily Insights