- The Breakdown

- Posts

- 🟪 DAS London Preview: Tyrone Lobban on Tokenization

🟪 DAS London Preview: Tyrone Lobban on Tokenization

Anti-establishment bitcoin is back within spitting distance of its all-time highs and for that, we have the establishment to thank

This issue is brought to you by:

“Crypto wants to be a revolution and blockchain wants to be an evolution.”

- Tyrone Lobban

DAS London Preview: Tyrone Lobban on Tokenization

Anti-establishment bitcoin is back within spitting distance of its all-time highs, and for that we have the establishment to thank — ETF investors poured over $500 million into bitcoin on both Monday and Tuesday of this week.

$1 billion! In two days!

This unprecedented level of inflows is forcing us to reassess just how much demand there is for bitcoin among traditional investors.

That, in turn, has fueled not just the price of bitcoin — $62,000! — but also the perception that TradFi’s adoption of crypto is finally in full swing.

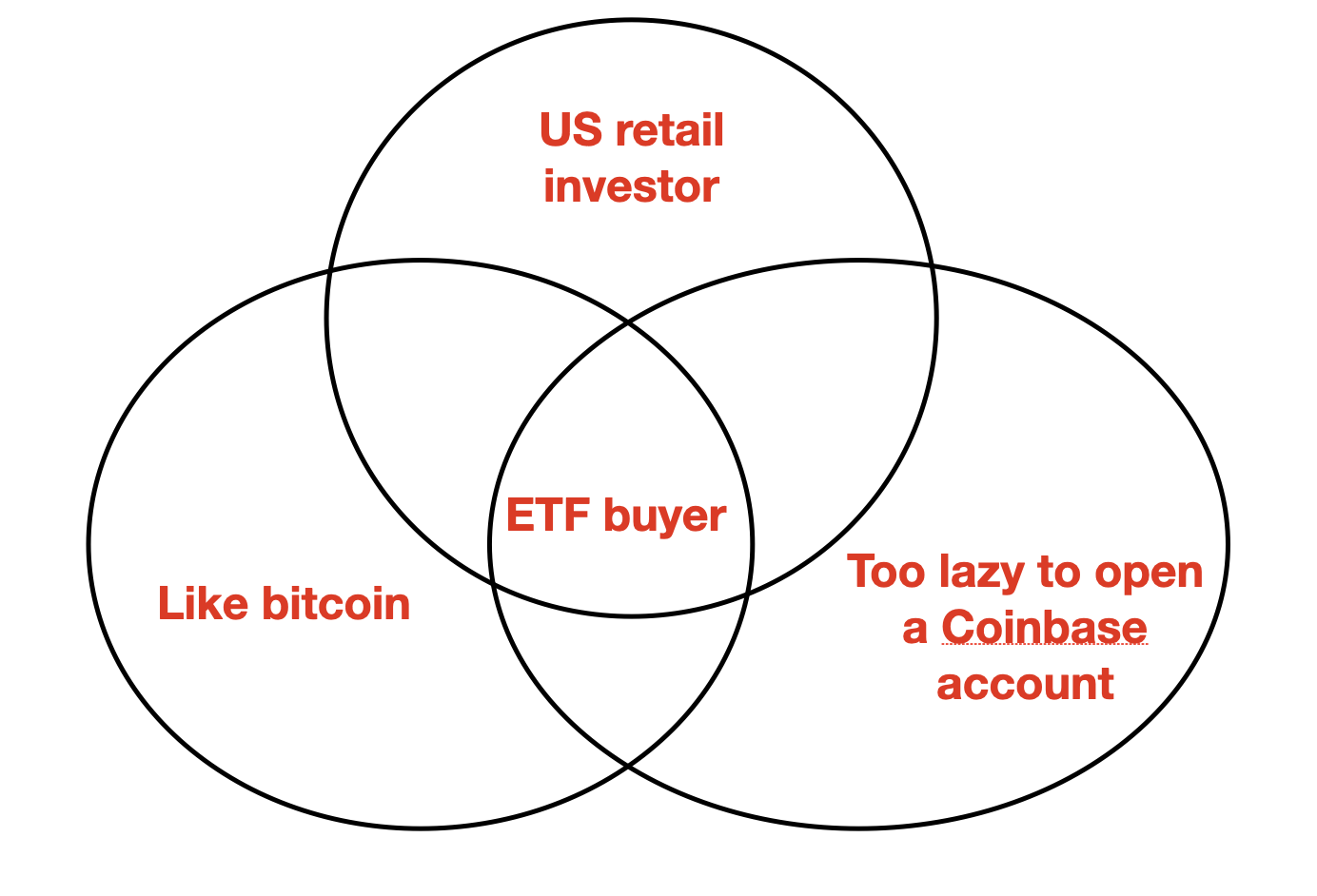

It isn’t.

ETFs are a retail product, so the true revelation here is that the Venn diagram of US retail investors, people eager to buy bitcoin and people too lazy to open a Coinbase account has far more overlap than we had expected.

Yes, there are some institutions buying ETFs too, but I’m guessing not many.

(We’ll have a better idea when asset managers file their Q1 13Fs in mid-May.)

For the most part, institutional investors remain more interested in blockchain than they are in crypto.

This is also welcome!

Larry Fink’s comments that tokenization “solves all corruption” and his belief that stocks and bonds should trade on “a general ledger that is all created together” are a remarkable expression of where crypto and TradFi have come to agree: Everything should be tokenized!

Where we still disagree, however, is on what this means.

When crypto natives hear “tokenization,” they imagine re-staking their Apple shares in EigenLayer for 5x points that will earn them an airdropped iPhone.

TradFi has something more prosaic in mind — but that something may prove to be just as impactful.

To pin down what “tokenization” really is, I thought it would be helpful to speak to someone who is in the arena, tokenizing assets.

No one fits that bill better than Tyrone Lobban, who leads JPMorgan’s firm-wide Blockchain Program as the head of Onyx Digital Assets and Blockchain Launch.

Tyrone will be speaking on tokenization at DAS London in March, but he was also generous enough to take an hour out of his day to field my questions.

As it turns out, an hour of talking generates far more words than would normally appear in this newsletter.

But I found Tyrone’s answers so helpful in thinking about what tokenization is, what’s being tokenized now and what might be tokenized in the future, that I thought I should share our conversation in full.

So, we will now make Blockworks Newsletter history by running the entire text of an interview, word count be damned.

(Tyrone, feel free to update your LinkedIn with this historic achievement.)

My conversation with Tyrone Lobban:

Are tokenized traditional assets “crypto”? Or just blockchain?

Tokenized traditional assets are not cryptocurrencies because they’re not an asset created by a protocol to incentivize usage and good behavior in that protocol. So, they are clearly very different from pure cryptocurrencies, but I think about them as a use case of blockchain, and you could argue that “crypto” is a use case for blockchain as well.

For traditional finance, tokenized assets are the killer use case [of blockchains].

What’s the overlap between crypto and blockchain?

In my view, the overlap is a drive toward a rewired financial ecosystem.

The path to getting there is a little bit different in each case, and maybe the end state goals are different. But clearly the overlap is this push toward a new and more efficient way to conduct finance.

I think more generally crypto is somewhat of a philosophy. Crypto is the desire to be permissionless and in some cases not be controlled by the rules of the status quo.

I think crypto wants to be a revolution and blockchain wants to be an evolution. But both of them can exist together, one’s success doesn't mean the other’s failure. This is not a zero-sum game by any means.

Is Onyx disrupting traditional markets? Or just making them more efficient?

We definitely have a mandate to disrupt, but by that I don't mean that we actively go out and break things. But we do have the ability to try to change the way things work and where or how revenue is generated.

I actually look at it through the lens of enabling new products. So yes, there's always the efficiency that you get from simplifying some processes and enabling parties to communicate with each other in a more trusted, real time, accurate way.

But the thing that we think about more than efficiencies or disrupting markets is, how do we create new products? How do we create new ways for our clients to do business? How do we enable different financial services to be established? That's the true focus for us.

This might be a bit philosophical, but do tokenized assets only “represent” an asset? Or is the asset itself on-chain?

I don't think it’s philosophical at all in fact.

There's a really important point, legally speaking, to recognize that tokenized assets are just a representation of the actual asset in almost all cases. It's very important for us to show that we're not issuing new assets because then you very quickly step into the realm of unregistered securities.

So, when we think about tokenized assets, we think about them representing the ownership rights to a legacy, traditional asset. Where this varies is when you have traditional, but digitally native assets. For example, if you're issuing a bond natively on a blockchain and there isn't an equivalent bond that's sitting in some custody account, then that bond truly is a new asset that lives on-chain.

That's a really good distinction.

Yeah, it's kind of interesting because when we tokenize assets, one of the biggest bodies of work that we undertake is the legal assessment of what tokenization of that asset means: What is this new form? And by new form, I mean the new form of recording ownership of that asset and how it fits within the existing regulatory and legal construct for whatever jurisdiction it’s in.

Would JPM be using public blockchains if regulators allowed it?

Right now, our use cases leverage permissioned blockchains. Would we use public blockchains at some point in the future? The idea of an open, always available, global infrastructure is interesting, of course. It’s somewhat use-case dependent though. We still think that there aren't strong, robust or scalable privacy solutions for tokens on public blockchains. We think there's some way to go from a scalability perspective. We need guarantees that a transaction is not going to be reverted, that it will actually settle. And finally, the question that we get asked consistently by our clients and by our regulator is: What happens if something goes wrong? Who do you call? How do you actually resolve an issue? If you have some multi-billion dollar transaction that is trying to settle and the network goes down or there is some failure, you need to get to a resolution pretty quickly. These are the types of things we think about.

That's not to say that the public blockchain ecosystem will never be usable for large scale traditional financial service use, but from our perspective we’re not there just yet.

Will I ever be able to use JPM Coin?

Just so we’re on the same page as to what JPM Coin is, it’s a blockchain-based bank account and today is exclusively available to institutional clients of JPMorgan. It's not a stablecoin, although one dollar in your JPM Coin account is one dollar. What we're enabling with JPM Coin is cross-border, wholesale payment flows and delivery-versus-payment settlement. So it's not something that's geared for retail right now.

What's the distinction between a blockchain-based bank account and a deposit token?

A deposit token is a monetary instrument that’s transferable from me to you, as opposed to a bank account that stays in situ and you move money in and out of it. So, that means that deposit tokens can be programmable in a much more blockchain-native way. If you think about Uniswap contracts, they are designed to actually hold tokens, they're not designed to interact with bank accounts or even deposit into a bank account — whether that account is on some blockchain or not.

When we think about this idea of deposit tokens, we think about a more blockchain-native construct for money that is transferable to KYC’d participants.

Would freely available tokenized bank deposits be better than stablecoins?

I don't think stablecoins are necessarily going away, there's clearly a use case for them. What makes deposit tokens interesting is that most of the world today operates on commercial bank money and deposit tokens are commercial bank money.

Our view is that deposit tokens will have a much better ability to do more of what commercial bank money does today, like credit creation, and will not create liquidity drags that stablecoins create due to the fact that stablecoins are fully reserved. As a result, we think that the size of the deposit token market, ultimately, will be significantly bigger than that of stablecoins’.

What kind of new financial products would tokenized assets enable?

Intraday-repo is one — establishing a repurchase agreement that can mature and settle intraday. That did not exist before we created it — it just practically couldn't be done.

Then there are interesting ideas like tokenizing cash flows. Any financial instrument is primarily just a set of future cash flows and now with this technology you could tokenize individual cash flows, individual coupons for a bond, for example, individual dividends, or whatever the case may be — those could become assets themselves that could be used either in the form of collateral or for payment, or pooling into some other investment vehicle. You can start to get much more fine-grained in terms of what a financial instrument actually is and how to think about not only the risk associated with it but the pricing of it. At scale that can look like almost an entirely different set of financial instruments to, or derivatives of, what we have today.

Are intra-day repos the most active tokenized real-world asset?

I would say from a traditional financial services perspective, yes. There's about $2 billion dollars of tokenized Treasurys and tokenized cash that are being exchanged in intraday-repo transactions on the Onyx Digital Assets (ODA) platform every day. That far exceeds any other tokenized real-world asset use case today. Repos are a very standard way of providing or accessing finance through the use of collateral, and now you can just do that in a better way.

What do customers use intraday repos for?

There are a variety of different reasons as to why people need funding during the day as opposed to only getting access to funds at some term duration. It can be to meet margin requirements in some cases, or to fund coupon payments. In other cases to meet FX settlement cycles. The idea of reducing your cost of borrowing by entering into a very short term intraday-repo as opposed to a traditional repo that's going to settle tomorrow or in two weeks’ time, for example, is very interesting.

Have you tried to calculate how much money customers have saved?

We did a case study with one client, the number they estimated was 56% cost savings versus their existing financing. So somewhere north of 50% is what we've seen.

Will a JPM customer ever be able to post a tokenized asset held with JPM as collateral with another bank?

One of the products that we have on ODA is a collateral mobility solution that enables a non-JPMorgan collateral provider to post tokenized collateral to a non-JPMorgan collateral receiver. JPMorgan is not in the flow of that transaction at all — these parties can tokenize assets on our ODA platform and then post the collateral directly to each other in a matter of seconds.

Is tokenization a hard sell with clients?

The concept and the benefits are an easy discussion to have because they are quite obvious and quite meaningful. There are always additional considerations that blockchain happens to bring along with it because of everything that happens in the crypto ecosystem or just because people feel like they want to understand the underlying technology more. But ultimately, it's not the tokenization part that’s hard, it’s more, how do I get this into my regular-way systems and processes and not create another set of processes?

Is Project Guardian the future of finance? Is that your lynchpin thing?

Our lynchpin is really the platform we're creating, ODA, because that enables this ecosystem of assets and new products. Project Guardian is a very forward looking view of what you can enable if you had tokenized assets at scale. That specific concept would look like a material overhaul of the existing processes for the better and give people access to products that they don't have access to today.

I do think about Project Guardian as a North Star to shoot towards, but ultimately, it's going to be enabled by a lot of the foundational work we're doing today.

Does that include the Singapore stuff about tokenized deposits?

Well, there have been two iterations of Project Guardian — one in 2022 and one in 2023. In 2022, we tokenized deposits of Japanese yen and Singapore dollars and we showed how you could use DeFi pools with KYC credentials to enable FX swaps between these currencies on a public blockchain. The 2023 iteration of Project Guardian was quite different in flavor. It was much more focused on tokenizing fund assets. We showed how, from a wealth management perspective, tokenizing alternative investments, for example, could enable an entirely new way of getting access to “alts” and also simplify the way that portfolio managers manage their investment portfolios today. Tokenization of alternative assets is a big focus area for us.

Which one of those two do you think would be realized earlier?

Good question. I think the second one would be because it is a narrower use case and one that we can really talk about tangibly with our asset management and wealth management clients — although there is still more wood to chop. Whereas large financial institutions actually using DeFi protocols on public blockchains for FX trading of traditional currencies are probably further away right now.

What does digital identity unlock?

I think about the principles of digital identity being analogous to the principles of crypto in some sense. I think digital identity is really the foundation for a truly global, lawful, open, “permissionless” ledger because ultimately it doesn't really matter what new technologies we all come up with — when it comes to moving money globally, there will always be requirements for KYC, there will always be requirements for preventing money laundering and there will always be requirements for ensuring adherence to sanctions laws. Those things are just not going to change and they shouldn't change.

So, when I think about what digital identity is, it’s the thing that can unlock money movement in a lawful way, globally and programmatically, and hopefully in a privacy preserving way, where you don’t have to reveal everything about yourself and how or why you're transacting, but you can still prove that your transaction is not illicit or malicious, and you're a good actor. You can't do any of those things at scale if some system doesn’t know who you are at some level.

And so, I think that identity is foundational for this goal that many people in crypto want to get to.

How far away are we from that?

It’s one of the hardest ideas to implement. It's a hard thing to build a global system around new concepts [like] verifiable credentials. One of the challenges is that it's not an obviously monetizable domain, which means it doesn't have money flowing into it from VCs, which means it doesn't have everyone trying to create solutions around it.

People look at it like a utility, and commercialization of that is hard. Until people see what it can unlock in other commercial domains, I think it'll be a secondary area of focus. We’re working hard on bringing decentralized identity solutions to market that can enable new commercial opportunities.

Will regulators ever accept zk Proof KYC?

I don't know. I don't know what it's going to take even for corporations to be comfortable with zk proofs. Is it something that you just take as read? Are you expected to have some mathematical understanding of the proof?

I think that regulators will accept a trusted credential that has been issued by a trusted identity provider, but the zk proof aspect is an open question.

Would JPM ever launch an L2 like BASE?

Our current focus is building out and scaling ODA. ODA is a multi-asset EVM platform that supports a variety of use cases and asset classes, has native on-chain cash to enable atomic settlement and delivery-versus-payment, and has a wide variety of clients and client types who can deploy assets and solutions onto it. Of course ODA is not permissionless, but could it become an L2 over time? Potentially, under the right conditions.

What might tokenization mean for alternative assets?

We're doing a lot of work in this space right now. We recently co-authored a paper with Bain wherein we projected that tokenizing alternative assets could unlock a $400 billion additional revenue opportunity for the alts industry. We think that tokenizing alternative assets can really simplify the way that these funds are managed operationally, the way investors get access to them, the way that money moves from investors to fund managers.

If you can simplify these backend processes and if you can standardize the way that private assets are processed, you can potentially create a truly shared record between investors, wealth managers and fund administrators. A lot of the complexity around managing alternatives could be streamlined. And if you can streamline that, you can potentially start to do more interesting things — you may be able to lower the investment sizes or create new liquidity solutions.

Would that enable me to buy a tokenized share in a VC or private equity fund?

What we’re not going to be trying to change is the regulatory requirements for accessing alternative assets. You would still have to be a qualified purchaser or accredited investor, for example. But you potentially could lower the investment minimums such that investors are able to build a much more diversified portfolio of assets.

Will I ever self-custody my equities portfolio?

We do believe that the world is going to move toward tokenized assets.

Does that mean that all assets are going to be tokenized? I think that's an open question, but at Onyx we certainly are doing a lot of work, every day, to increase the number of assets that are available on blockchains.

This issue is brought to you by:

With thousands of Solana validators, how do you know you're staking to the right one? Enter Marinade: the ultimate solution to stake SOL.

Marinade monitors all Solana validators and automatically stakes with hundreds of top performers, constantly rebalancing for peak performance along the way.

Stake with Marinade Native for no smart contract risk, or go liquid with mSOL to use in DeFi. It’s Max Decentralization for Solana and Max Performance for you.

Top Stories

Bitcoin returns to $61k after closing in on new all-time high — Read

Gemini settles with NY regulators, will return $1B to Earn customers via Genesis bankruptcy — Read

Coinbase says it’s investigating zero-balance issue amid $64k price pump — Read

What can blockchain do for AI? Not what you’ve heard. — Read

The role of RWAs in the evolution of stablecoins: Report — Read

We're Watching

In today's episode Mike and Hart are joined by Bryan Pellegrino, co-founder of LayerZero, to debate the end state of the multi-chain future.

Thank you to our sponsor:

Arbitrum is the leading Ethereum Layer 2 scaling solution, home to over 600+ applications.

Arbitrum allows you to interact with Ethereum the way it was meant to be - with lower fees and faster transactions. Whether you're exploring the leading DeFi ecosystem, the strong infrastructure options, a flourishing NFT and creator ecosystem, and a rapidly growing gaming hub, the Arbiturm ecosystem has a solution for you.

Daily Insights

The new record for #Bitcoin ETF trading volume is officially $7.69 billion. Previous record was $4.66 billion from launch day.

— James Seyffart (@JSeyff)

9:51 PM • Feb 28, 2024

AI is to Nvidia as the ETF is to Bitcoin. BTC is experiencing a step function change. The ETF’s have not yet been onboarded at the wire houses or major wealth platforms. It’s still the first inning.

— Anthony Scaramucci (@Scaramucci)

10:42 AM • Feb 28, 2024

Why We Aren't (S)Topping

(for my first ever long X post, I'm releasing a note I sent early this this morning to Galaxy counterparties and clients)

The sun hasn’t yet risen in NYC, but I know it will. From Galaxy HQ north of Battery Park, the Hudson River looks like a sea of… twitter.com/i/web/status/1…

— Alex Thorn (@intangiblecoins)

3:43 PM • Feb 28, 2024