- The Breakdown

- Posts

- 🟪 The Fed’s real MVP: Prices

🟪 The Fed’s real MVP: Prices

Here’s how higher interest rates lead to lower prices

Byron Gilliam

September 18, 2024

Brought to you by:

“Prices are a signal wrapped up in an incentive.”

— Alex Tabarrok

The Fed’s real MVP: Prices

With inflation already rampant, the FOMC began raising the fed funds rate in March 2022 and it seems to have worked: Inflation (eventually) fell.

Now it’s cutting the fed funds rate because inflation has fallen enough — and if it falls too much, it will cut faster.

That might work too. Keeping rates just low enough might keep inflation just high enough (and no higher).

The problem, however, is that the Fed may have things exactly backwards.

The stickiest component of US inflation has been housing, where raising rates is most likely counterproductive.

Mark Zandi recently told The Atlantic that when it comes to housing, “the Fed’s main tool for lowering inflation is actually doing the opposite.”

It’s easy to see why: Raising the cost of money has raised the cost of building new housing — so much so that many would-be new homes don’t get built, as the Wall Street Journal reports.

By raising interest rates, therefore, the Fed may have prevented the supply response that would correct the underlying cause of rising prices.

If so, it may be because the Fed is treating prices as if they’re the problem when they’re actually a symptom of the problem — and the solution, too.

Prices serve two purposes, according to a report from the Fed itself: They send signals about “the relative scarcity of a good or service” and offer incentives for buyers and sellers to adjust accordingly (by buying less or offering more).

Using interest rates to fight inflation risks muddying that signaling power of prices and the short-circuiting of those incentives.

It’s not just about housing.

“The rise in interest rates by itself has essentially no power to lower inflation,” according to the grumpy (and very readable) economist John Cochrane.

In fact, raising rates is more likely to do the opposite: Higher interest rates, Cochrane explains, allow consumers to save more now, which in turn allows them to buy even more later.

The result is that “higher interest rates lead to higher inflation in the long run.”

I suspect that Chair Powell secretly agrees but is unable to say so because he’s forced to worry about the short term, too — the Fed is tasked with fighting inflation on a monthly basis and it’s given just one tool (monetary policy) to do it with.

So that’s what it tries to do by fiddling with interest rates at semi-monthly meetings, like today’s.

In a candid moment, I’m sure Powell would tell you that the real way to fight inflation is not with the monetary policy he controls but with fiscal policy: Rising prices are fundamentally a symptom of more money chasing the same amount of goods, so the real way to fight it would be to tighten fiscal policy with lower government spending.

That is a political non-starter nearly everywhere, of course, so Chair Powell and his central banker colleagues are forced to pretend that they can fight inflation by raising interest rates.

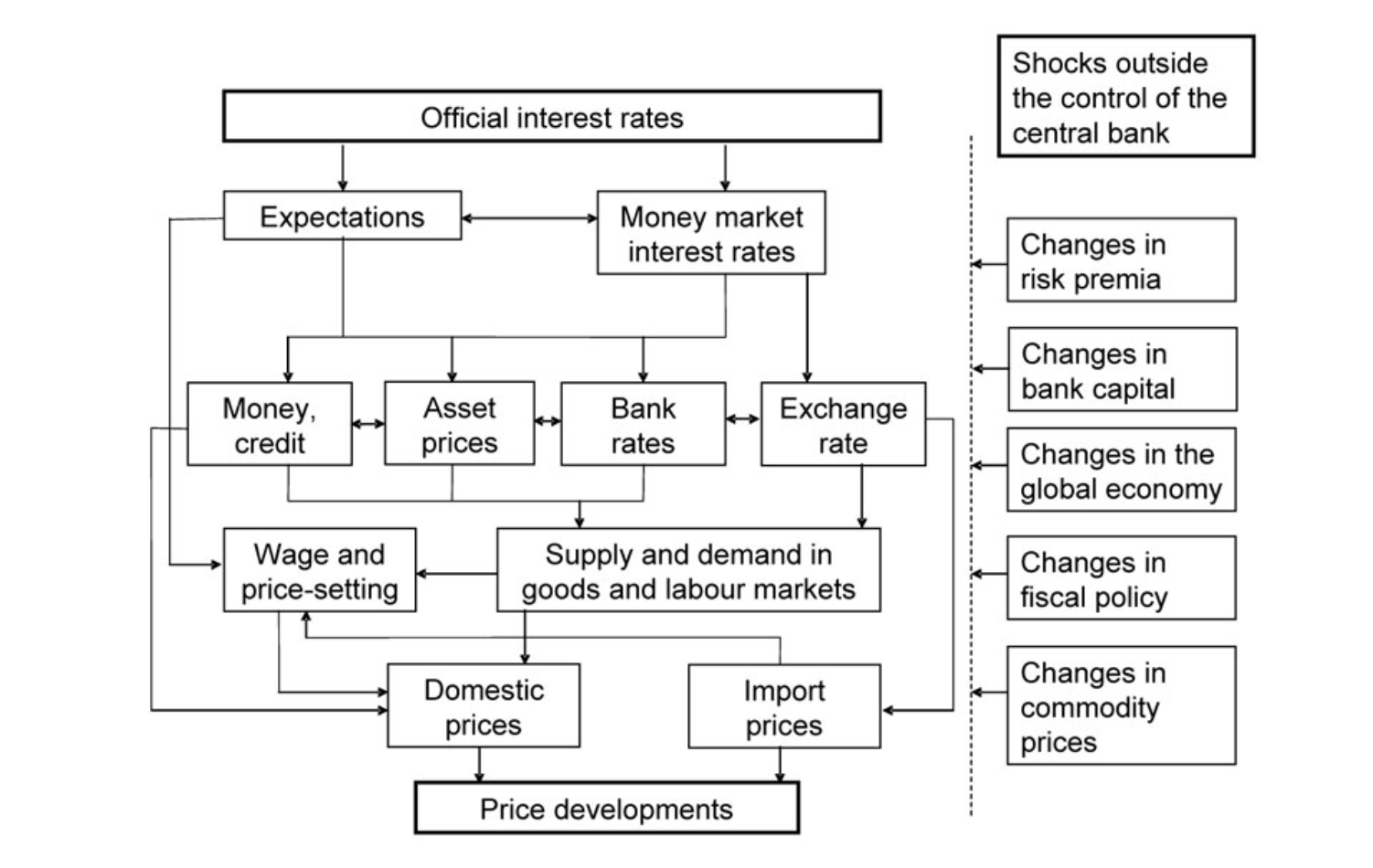

Here’s how higher interest rates lead to lower prices, according to his colleagues at the ECB:

Got that?

Now imagine thinking that changing interest rates by 50 basis points will get all of those arrows moving in the right direction to just the right degree so that it achieves just the right effect on inflation.

Yeah, probably not.

What the graphic gets right, however, is its stark illustration that the economy is a complex, adaptive system.

What the market probably gets wrong is the idea that the FOMC can micromanage that system by fiddling with interest rates.

Worse still, they might well be fiddling them in the wrong direction!

Higher interest rates may have impeded the system from adapting to the signals and incentives provided by higher prices.

Credit where due

In his press conference this afternoon, Chair Powell insisted that “we’re not declaring mission accomplished” — but I think he’s entitled to because today was a big day for the FOMC.

They took a lot of heat for not raising rates soon enough and then not raising them fast enough. Yet, eighteen months later, they seem to have gotten it about right: Inflation is down with no harm done to the economy.

Still, they may well have gotten it right for the wrong reasons.

It may be that prices accomplished the mission for them.

Brought to you by:

Avantgarde Finance dives into the DEX aggregator landscape in their latest report. Key takeaways include:

1inch has seen market share decline on metrics such as volume

ParaSwap and CoW look relatively undervalued on market cap to fundamental ratios

Token utility varies significantly, such as with PSP offering notable staking benefits yielding up to 31%

New features set to differentiate protocols further and may serve as catalysts to narrow existing valuation gaps

Download our report today to find out more!

Can Drift Rival Binance?

Bell Curve host Michael Ippolito joins BWR analysts to discuss the PerpDEX sector, prediction market success after the US election and the different ways to monetize social networks. Tune in to find out which parts of crypto suck and how to get silly onchain.

Your all-time favorite newsletter author will be IRL at Permissionless chatting with the top liquid token fund managers on how they seek and find alpha in the digital asset space. Don’t miss it!

enjoyed talking crypto with @jdorman81 on @arca's That's Our 2 Satoshis ... thanks for letting me invite myself on!

youtu.be/aotlyHPEso0?si…— Byron Gilliam 🟪 e/acc (@bgilliam1982)

2:01 PM • Sep 18, 2024

(FT) - India has overtaken China’s weighting in one of the world’s biggest stock market benchmarks, as share sales and rising liquidity in Indian companies make the country more open to investors.

@FT@knowledge_vital

ft.com/content/72864f…— Carl Quintanilla (@carlquintanilla)

1:58 PM • Sep 18, 2024

We looked deeply at the evolving Bitcoin ecosystem and concluded that it is technically complex, politically path-dependent, and generally still under construction.

— Dmitriy Berenzon (@dberenzon)

1:52 PM • Sep 18, 2024