- The Breakdown

- Posts

- 🟪 Friday Charts

Friday charts: The revolution is listed

The start of the information-technology revolution can be identified with unusual precision: November 15, 1971, when Intel introduced the 4004 microprocessor in an Electronic News ad. “A micro-programmable computer on a chip!”

It was the world’s first single-chip microprocessor — an entire CPU (central processing unit) built into an integrated circuit on a sliver of silicon. No circuit boards. No soldering.

The 4004 first appeared in unassuming products like calculators and pinball machines. So it took a while for investors to recognize its significance.

Here, too, we can be surprisingly precise. In a study of how investors reacted to the advent of information technology, economists Bart Hobijn and Boyan Jovanovic conclude, “The IT revolution was anticipated by early 1973.”

Here’s how they know: the stock market went down.

The same technology credited for a multi-decade boom in the US stock market is also the primary reason why it fell in the ‘70s and stagnated in the first half of the ‘80s.

As Hobijn and Jovanovic tell it, investors recognized that many incumbent companies — the ones available to them on the stock market — risked obsolescence in this new era of information technology.

There would be winners, of course, but these were not yet obvious. What was obvious was that few of them were publicly listed (if formed, even).

As a result, the total value of US equities fell from 78% of GDP in 1972 to just 37% in 1974.

Valuations remained depressed until a new generation of companies — the first winners of the IT revolution — grew large enough to IPO.

This process took exactly 12 years.

We know that, Hobijn and Jovanovic say, because that’s when the relative value of stocks started going back up: the market capitalization of US equities went from 40% of GDP in 1985 to 130% in 1999.

Today — at the start of a new revolution in information technology — it’s 215%.

That may seem like a precarious height given how uncertain things seem. But, this time, there are plenty of winners to invest in: cloud providers, utilities, data center builders, and the entire semiconductor industry, for example.

Even a company as old-school as Caterpillar is a winner, thanks to its natural gas generators — which it's been making for decades — being used in data centers. The shares are up 170% over the past year.

Legacy winners like these are breaking the pattern of the IT revolution by more than offsetting declines in AI losers (software companies, mostly).

Also different this time: we won’t have to wait 12 years to invest in the new winners. The IPOs of Anthropic, OpenAI, and SpaceX should soon add at least $3 trillion to the value of listed US equities.

So, for all of the things investors have to worry about, a lack of options is not one.

But is there any upside to the stock market from a starting point of 200% of GDP?

Let’s check the charts.

The last time:

Per Hobijn and Jovanovic, this chart is mostly attributable to the advent of information technology. First because of the old firms it threatened to make obsolete and then because of all the new firms it enabled.

This time:

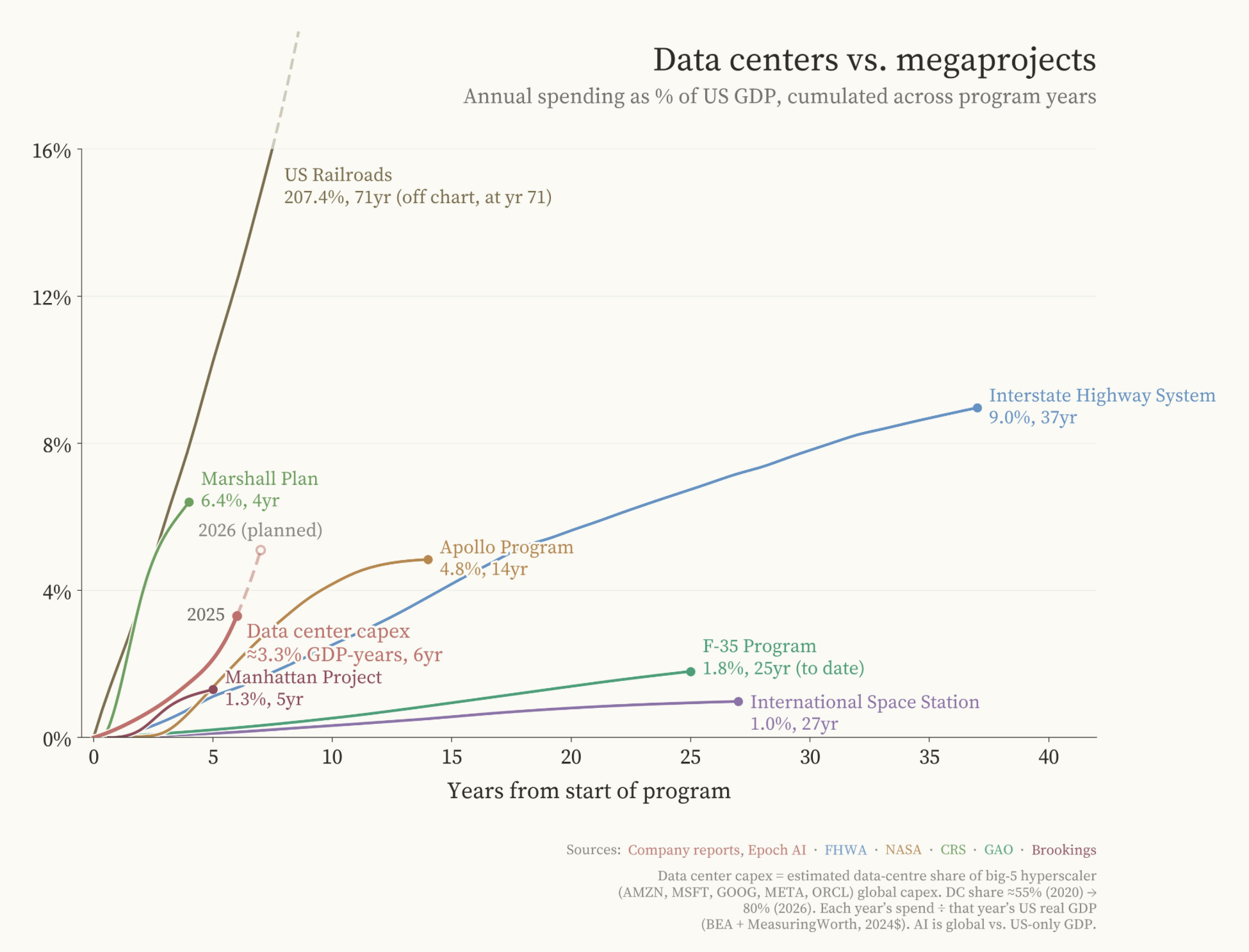

AI researcher Fin Moorhouse puts the current buildout in data centers in perspective by charting it against previous US megaprojects, like the highway system and US railroads.

Adjusted for GDP:

The data is less dramatic when measured as a share of GDP — which might mean we’re just getting started?

Very dramatic:

The Nasdaq was up 9.8% in the ten days to Tuesday — a 100th percentile event, per Warren Pies.

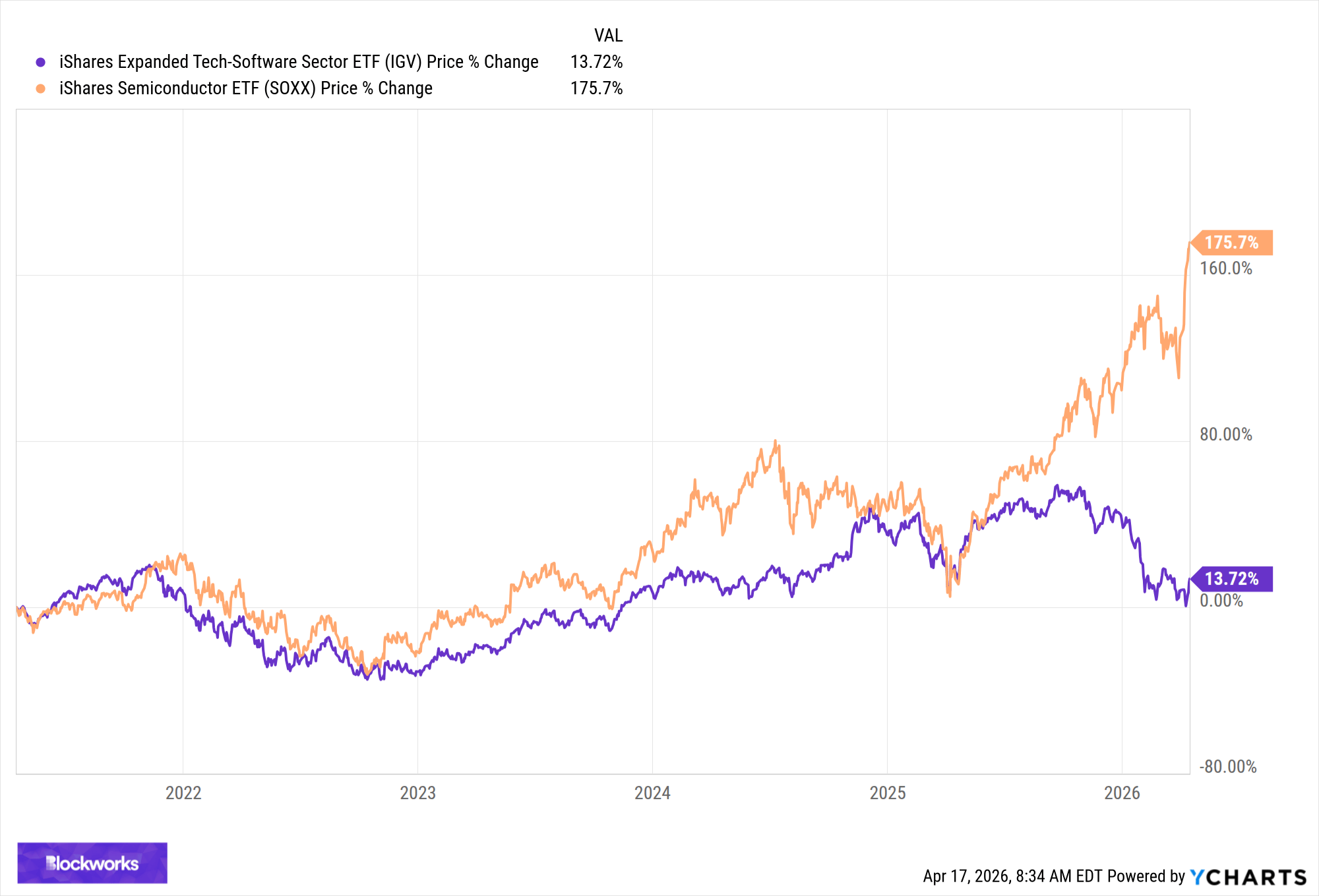

Winners and losers:

Year-to-date, semiconductor stocks have outperformed software stocks by twenty percentage points (and 163 percentage points over the past five years).

Unprecedented:

The dispersion of returns within the US technology sector has never been higher — which is what happens when the winners and losers from a new information revolution are both immediately available to trade.

Future IPOs:

Investors are betting big on the next generation of winners, as well. The dollar-value of venture capital investments hit an all-time high of $300 billion in the first quarter of 2026, up nearly 3x from the quarter before.

Near-future IPO:

The market value of Anthropic, as measured by perpetual futures on Ventuals, passed $1 trillion for the first time today.

Planting AI seeds:

Valuations of the very newest companies have skyrocketed. The red line above shows that the largest seed-stage startups were valued at $175 million in the first quarter of the year, up from $65 million less than a year ago.

The next big thing:

Morgan Stanley has data on the performance of Mythos. Charted against the performance of previous models, Mythos is above trend, but perhaps not as dramatically as Anthropic makes it out to be. Similarly, hallucinations (charted on the right) have declined, but not too dramatically.

Information revolution survival rate:

Morgan Stanley notes that, of every 100 publicly listed companies from 1976 (excluding financials), only 18 have survived in their original form.

It might happen faster this time.

Have a great weekend, revolutionary readers.

Introducing Blockworks Investor Relations, an IR platform built for onchain businesses.

The latest Blockworks offering brings together analytics, a branded investor relations site, and integrated advisory support into a single platform. The result is a more efficient way to share your story, build trust with investors, and engage a global audience from day one.

Check out our cofounder Michael Ippolito's keynote at DAS NYC launching the new IR platform.