- The Breakdown

- Posts

- 🟪 Friday Charts

🟪 Friday Charts

This was the third straight week of worrying about “AI capex ROI” and more importantly, the first week of genuinely worrying about recession.

Byron Gilliam

August 02, 2024

Brought to you by:

“If you can keep your head when all about you / Are losing theirs….”

Friday Charts

This was the third straight week of worrying about “AI capex ROI” and more importantly, the first week of genuinely worrying about recession.

The latter may be hard to credit after three straight years of hearing that the macro sky is falling, during which investing skies only got brighter.

But, like a broken clock, the macro chicken littles may finally be on to something.

This morning’s jobs data suggests the US economy might be rolling over and that the Fed might already be well behind the curve.

As of just last month, none of the 19 FOMC members forecast unemployment above 4.3% anytime before 2027.

This morning’s unemployment number? 4.3%.

There are 29 unemployment reports between now and 2027, so it’s unlikely we’ll get there without a higher one.

Already, that 4.3% number has changed the macro debate from when the Fed will cut rates to how fast.

At least two big investment banks are now predicting 50 basis point cuts at each of the September and November meetings and another 25 bps in December.

Even that may not be fast enough however, judging by the market’s reaction today.

The jobs data has scrambled the investing debate as well, with cyclicals and tech both sharply lower today and bonds breaking out to new year-to-date highs.

The market’s message? US rate cuts are coming, but they may be coming too late for cyclicals and too slowly for tech stocks.

They may also be coming at the same time as rate hikes in Japan, which poses a different sort of problem for markets.

The confluence of lower interest rates in the US and higher interest rates in Japan has crashed the dollar/yen exchange rate from 160 just a month ago to 146 today.

That is an inconvenience for foreign visitors to Japan, a problem for Japan’s exporters and a disaster for the legions of hedge funds that are suddenly losing money on the infamous “carry trade.”

Borrowing yen for near 0% and using it to buy US assets yielding 4%+ has been such an easy trade for years that there may be trillions of dollars tied up in it.

Much of that could now be unwound, pulling liquidity out of US markets with potentially unpredictable results.

On the other hand, macro doomsters have been ringing false alarms about the yen carry trade even longer than they have recession — much longer. For decades, really.

So this could be just another in a long series of false alarms, I don’t know — these things are by definition unpredictable.

As investors, all we can do is try to stay as calm as Türkiye’s Yusuf Dikeç.

But we have to know when to panic, too.

So let’s check the charts.

Is 4.3% a lot?

It doesn’t look like much, especially coming in the shadow of the pandemic spike, but history shows that unemployment tends to be a slippery slope (upwards).

Can we break the rules?

This morning’s unemployment report has triggered the “Sahm rule” recession indicator, suggesting that we are already in a recession (but just don’t know it yet). Claudia Sahm herself cautions that we shouldn’t take the Sahm rule as gospel, but it would have predicted each of the last nine recessions.

Bonds are back:

The iShares investment grade bond ETF (AGG) broke out to a new year-to-date high this morning and is rapidly catching up to small-cap equities, which were surprisingly in-vogue as recently as last week.

We can all finally move again:

With 30-year mortgage rates down 22 bps (0.22%) just today, sub 6% mortgages suddenly seem nigh. The golden handcuffs of having a low-rate mortgage may soon be coming off.

The chart of the moment:

One US dollar will only buy you 147 yen now, down from 160 just a month ago. But even if you’re not planning a trip to Japan (which you should be), watch this chart: For markets, yen up (like now) means risk-off, and yen down (like it usually is) means risk-on.

Trend change coming?

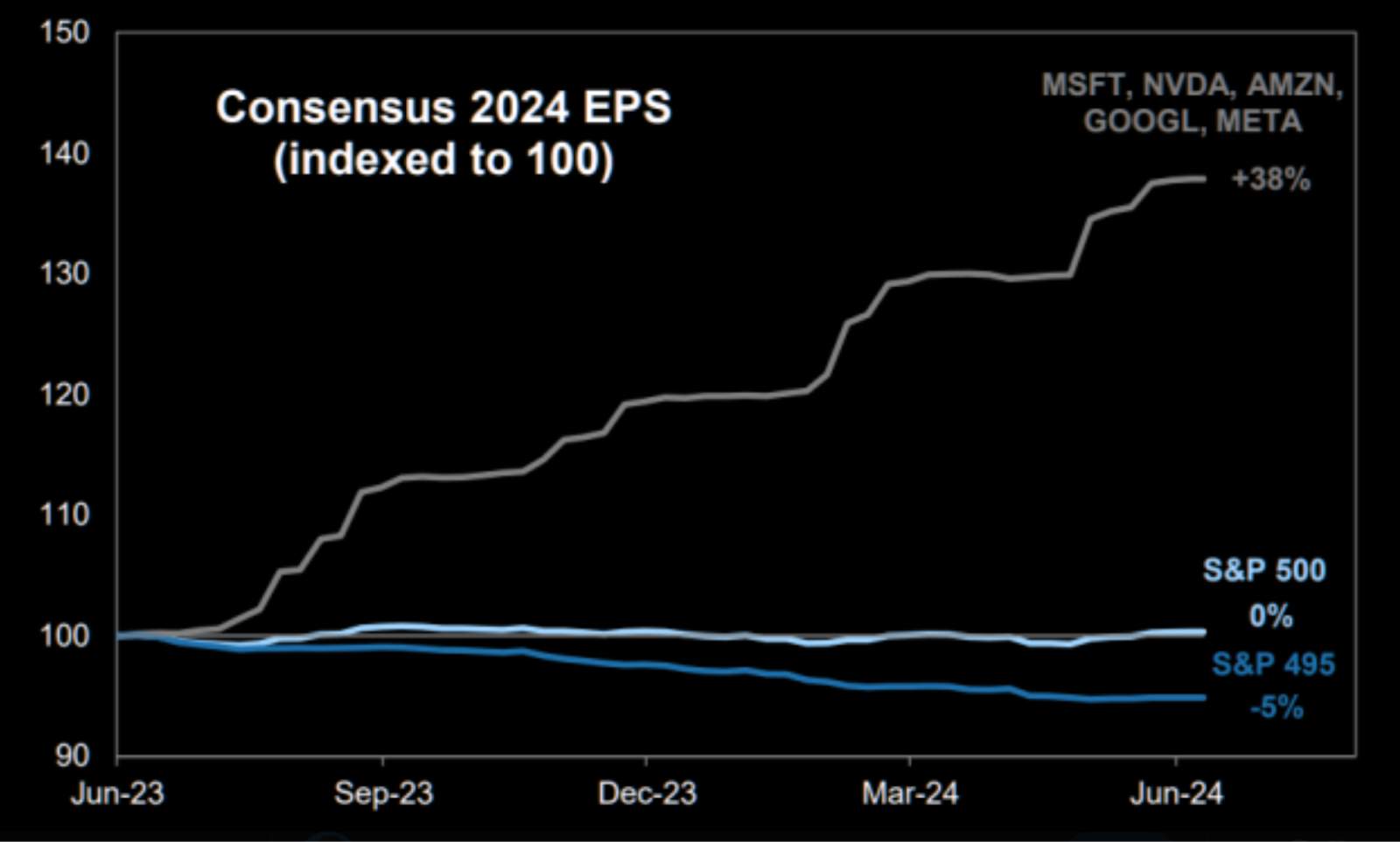

The reason the S&P 500 is still up 12% year to date is not because there’s been a bubble in AI stocks — it’s because AI stocks have been making more money than expected. That could change in a recession.

The “AI capex ROI” fears in a picture:

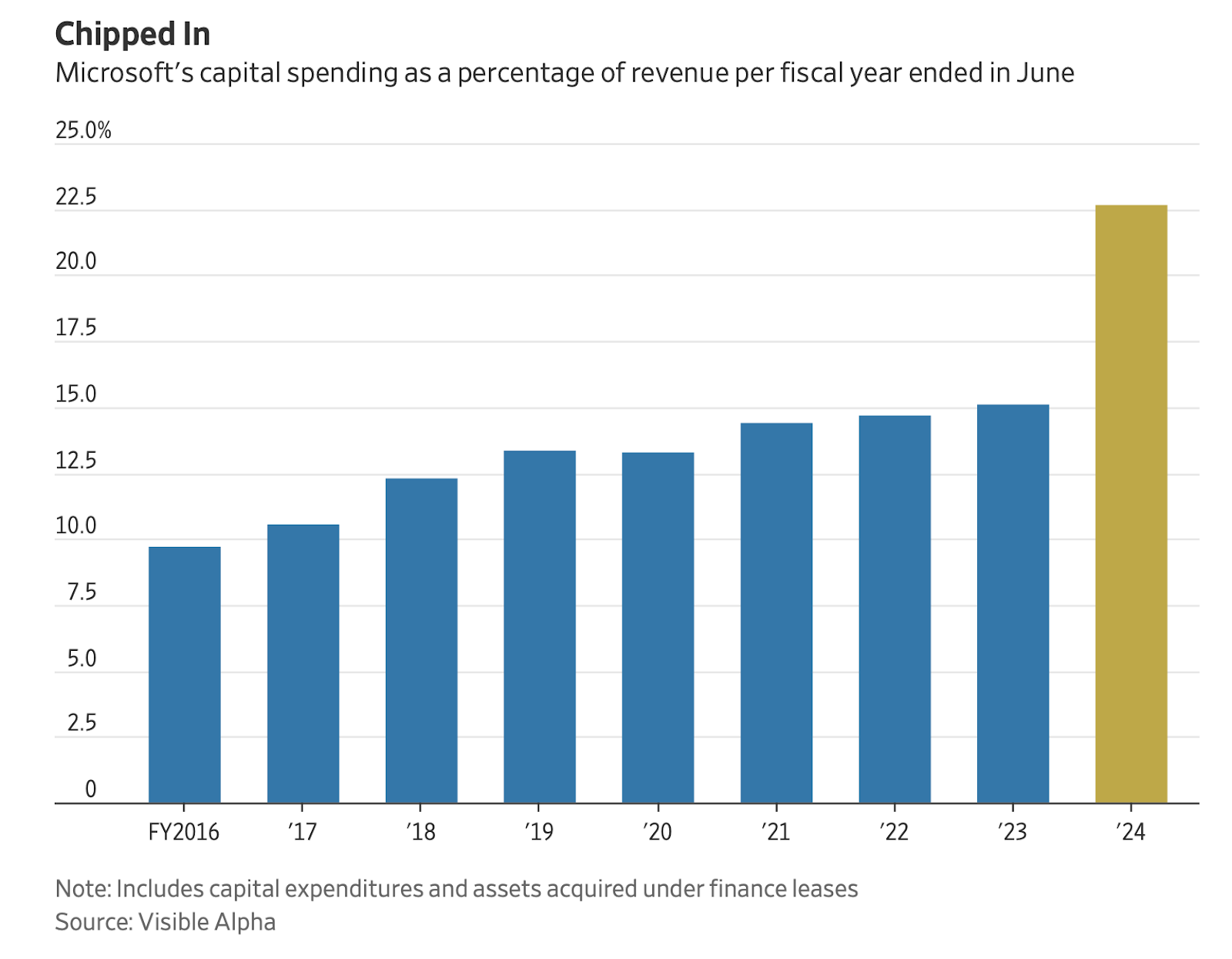

Microsoft’s capital spending as a percentage of revenues has taken a step change higher and is still rising. CEO Satya Nadella said on Tuesday’s call that Microsoft has the “demand signal” to justify the spend. Whether he’s proven right will be as big — or bigger — for the stock market than whether Chair Powell gets interest rates right.

We might Nadella to order some factories:

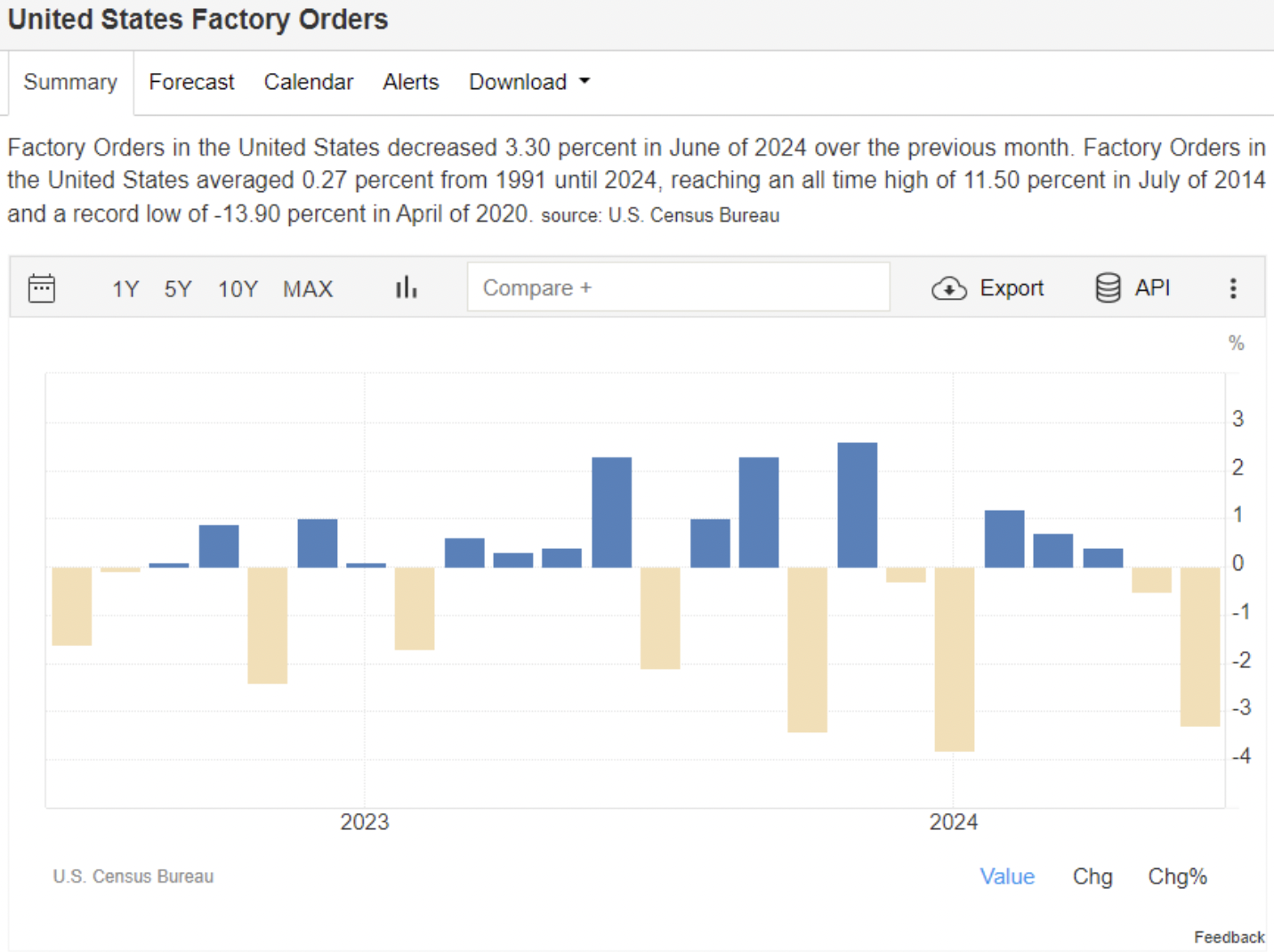

US factory orders fell 3.3% in June — one of a number of data points out this week that suggest this morning’s jobs report might be the start of a trend and not just a false alarm.

The case for a false alarm:

The BLS said Hurricane Beryl had "no discernible effect" on unemployment in July, but I seem to discern one in the above chart — nearly half a million people said they were employed but not at work due to bad weather (unusual for July).

False or otherwise, the market’s alarm bells are ringing and it feels like people are about to lose their heads.

Should we heed Rudyard Kipling and stay as cool as silver medalist Yusuf Dikeç?

In markets, that is always the right thing to do — except when it’s not.

Have a great weekend, sharpshooters.

Brought to you by:

RadQuest is out now and provides a Web3 onboarding experience anyone can confidently use.

MiCAR will give foreign stablecoins a clear advantage in Europe [Opinion] — Read

US stocks, cryptocurrencies tumble on disappointing jobs report — Read

Testing is a bottleneck to progress on next Ethereum upgrade — Read

UQUID integrates USDT on TRON for seamless public transport payments in Argentina [Sponsored] — Read

Radix’s gamified onboarding platform RadQuest simplifies Web3 for anyone [Sponsored] — Read

Bringing ZK Proofs to Developers Everywhere

Succinct Labs CEO and co-founder Uma Roy dives into Succinct’s Prover Network & SP1, why zkVMs are needed and the importance of being open source. Tune in for insights about the market for zkVMs as well as Succinct’s go-to-market strategy and its future visions.

Brought to you by:

re.al is the permissionless L2 for tokenized RWAs built on Arbitrum Orbit, bringing off-chain yields onchain. re.al is the first L2 to return chain and protocol fees back to users in reETH, ensuring they benefit from the growth of the ecosystem. We’ve just launched a fully-transparent rewards program returning 10% of $RWA supply to early users. Get started, trading, borrowing, and leveraging a diverse selection of RWAs. Not investment advice or product solicitation and not aimed at US persons.

ETF volume is elevated but not crazy high at all. I'd expect to see $SPY at $30b by now if sht was really hitting fan. Also $VXX is way down at 19th spot (normally it is in top 10 when sky falling). Points to a short-lived selloff but who knows!

— Eric Balchunas (@EricBalchunas)

4:12 PM • Aug 2, 2024

chart of the day

Bitcoin is a TRUMPWIN market

Trump’s odds on Polymarket perfectly tracked the price of Bitcoin for 12 weeks, the shaded area in the middle

— David Canellis (@dcanellis)

1:46 PM • Aug 2, 2024

market now pricing in a >70% probability of TWO cuts in September 👀 vs ~10% a week ago - one of the fastest narrative shifts I've seen

the danger is, if the Fed only cuts 25bp (1x), it'll look out of touch - if it cuts 50bp (2x), it'll look like it's panicking

— Noelle Acheson (@NoelleInMadrid)

4:38 PM • Aug 2, 2024