- The Breakdown

- Posts

- 🟪 Friday eventful charts

Brought to you by:

“Events, dear boy, events.”

— Harold McMillan, on why things happen

Friday eventful charts

When the Overton window is so wide open that Gaza might become the 51st US state (or, God forbid, Canada), truly anything can happen.

We seemed to get a taste of that this week, which started with threats of unexpectedly high tariffs on Canada and Mexico and ended with only unexpectedly low tariffs on China.

(Will a 10% tariff save the US auto industry from the $610 truck pictured above?)

Markets took it all in stride, however, with equities up a little on the week, bond yields down a little and currencies not much changed.

I find that reassuring — especially as markets seemed to correctly predict that Trump wouldn’t follow through with the tariffs on Mexico and China.

But can we trust the market to price everything in for us?

If Friedrich Hayek is correct in that everything we need to know about markets is captured in prices, we can all relax: Prices of stocks, bonds and currencies are telling us that the president is out to make deals and not do anything too disruptive.

I dearly hope that’s right, and not just for the sake of my investment portfolio — I really don’t want to spend two hours every morning parsing the latest political news.

But when the headlines are as wacky as they were this week, it’s hard to resist.

Was there any method to the madness?

Treasury Secretary Bessent said Trump’s intention is simply to get interest rates, trade deficits and the fiscal deficit down, which no one could object to.

Others, however, think President Trump has a grander plan to radically reshape the global economy.

Either way, I doubt there’s much sense in trying to predict it because whatever the president’s current plans, they are sure to be disrupted by events.

Some of those events will be of his own making: Who knows what headlines we’ll wake up to tomorrow?

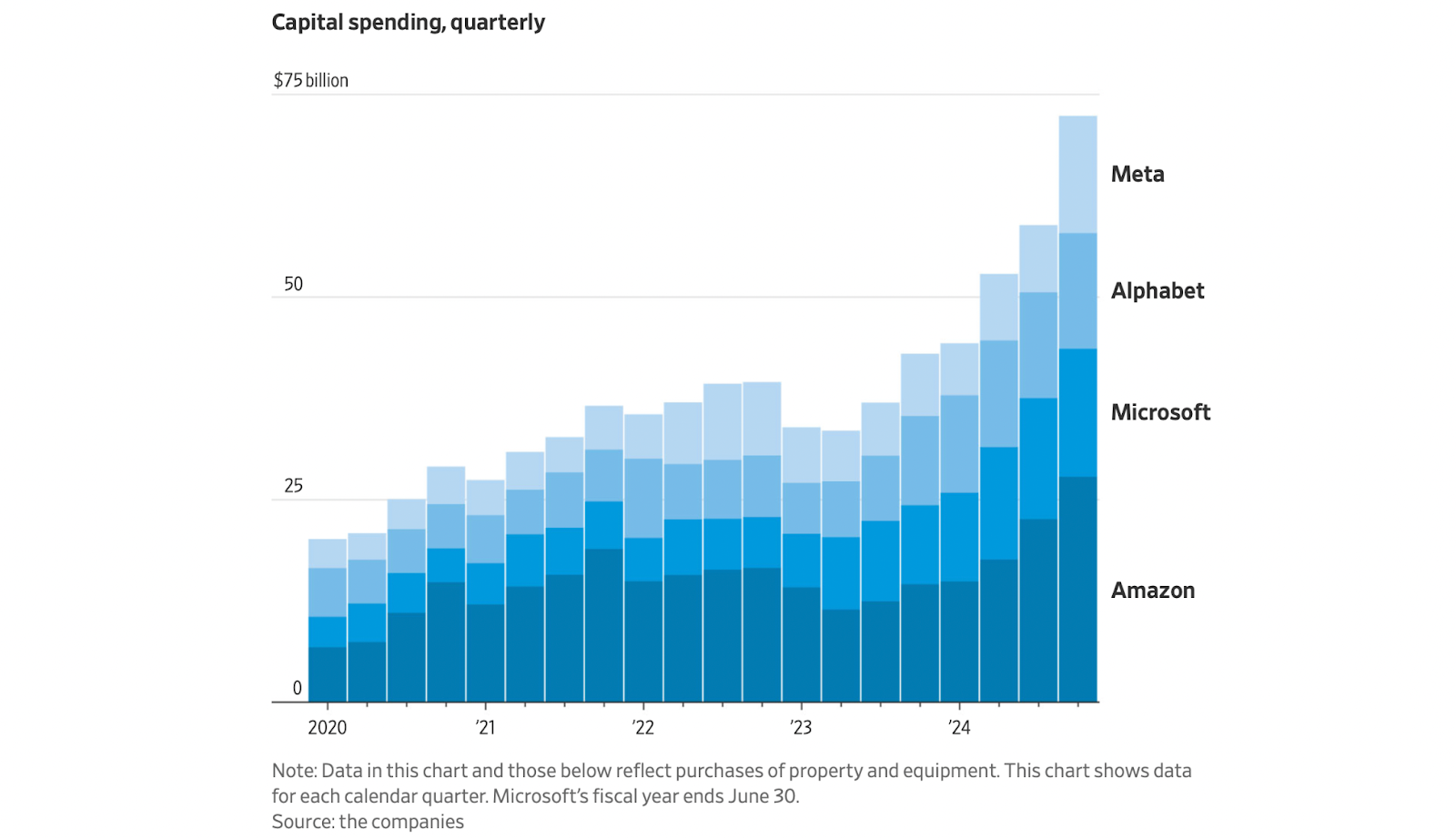

Others will not: The US tech sector is now expected to plow $3 trillion into AI infrastructure over the next few years, with who knows what consequences.

All we know for sure is that the future will be determined by these political, AI and as-yet-unimagined events.

This week it felt like they’ll be coming at us faster than ever. With the Overton window flung wide open, the best we can hope to do is just try to keep up.

So let’s check the charts.

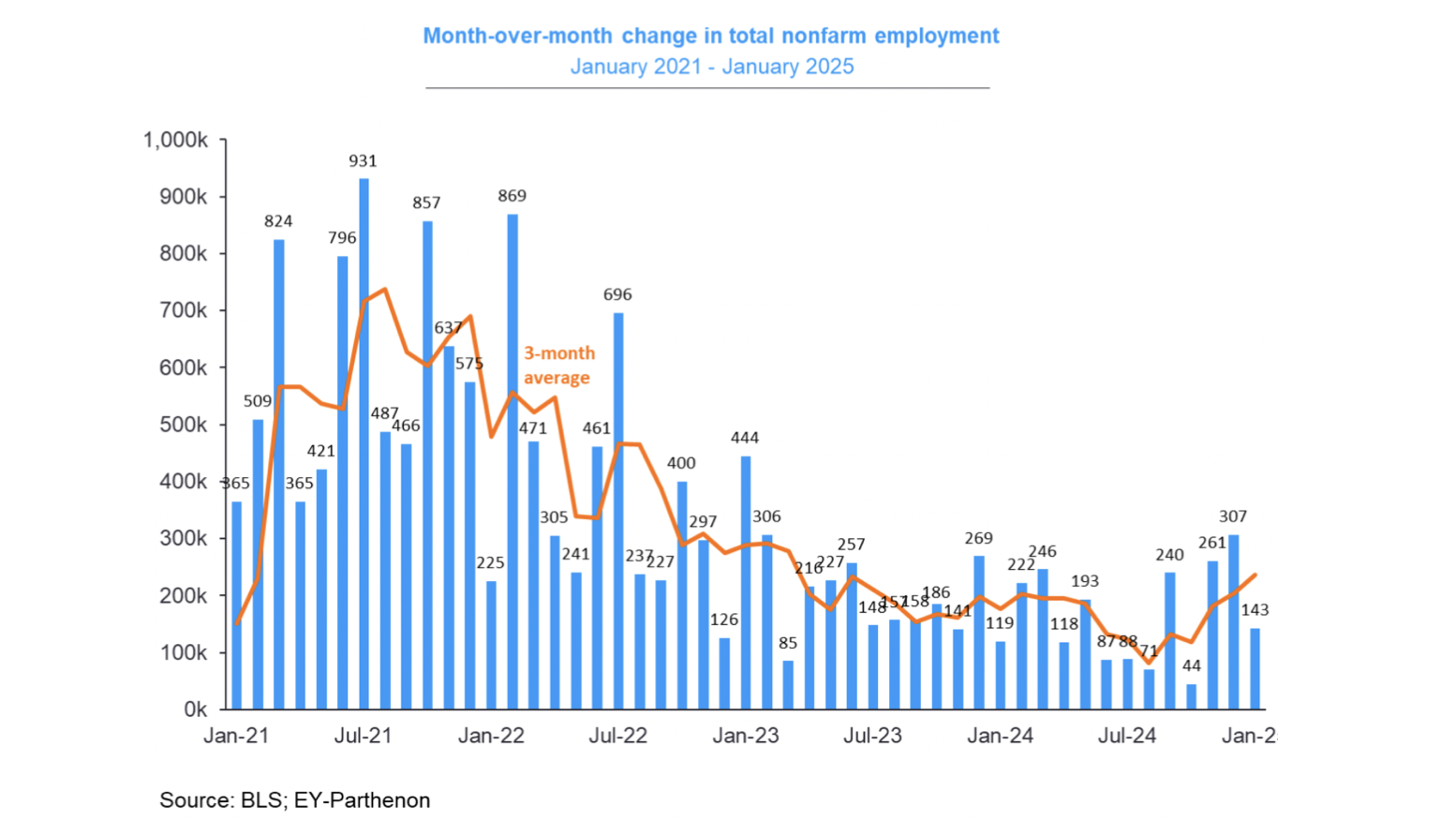

An uneventful jobs report:

January nonfarm payrolls were solid at +143k and a +50k revision to the previous month. The US economy remains near full employment, with labor force participation rising, jobs still growing and real wages still rising.

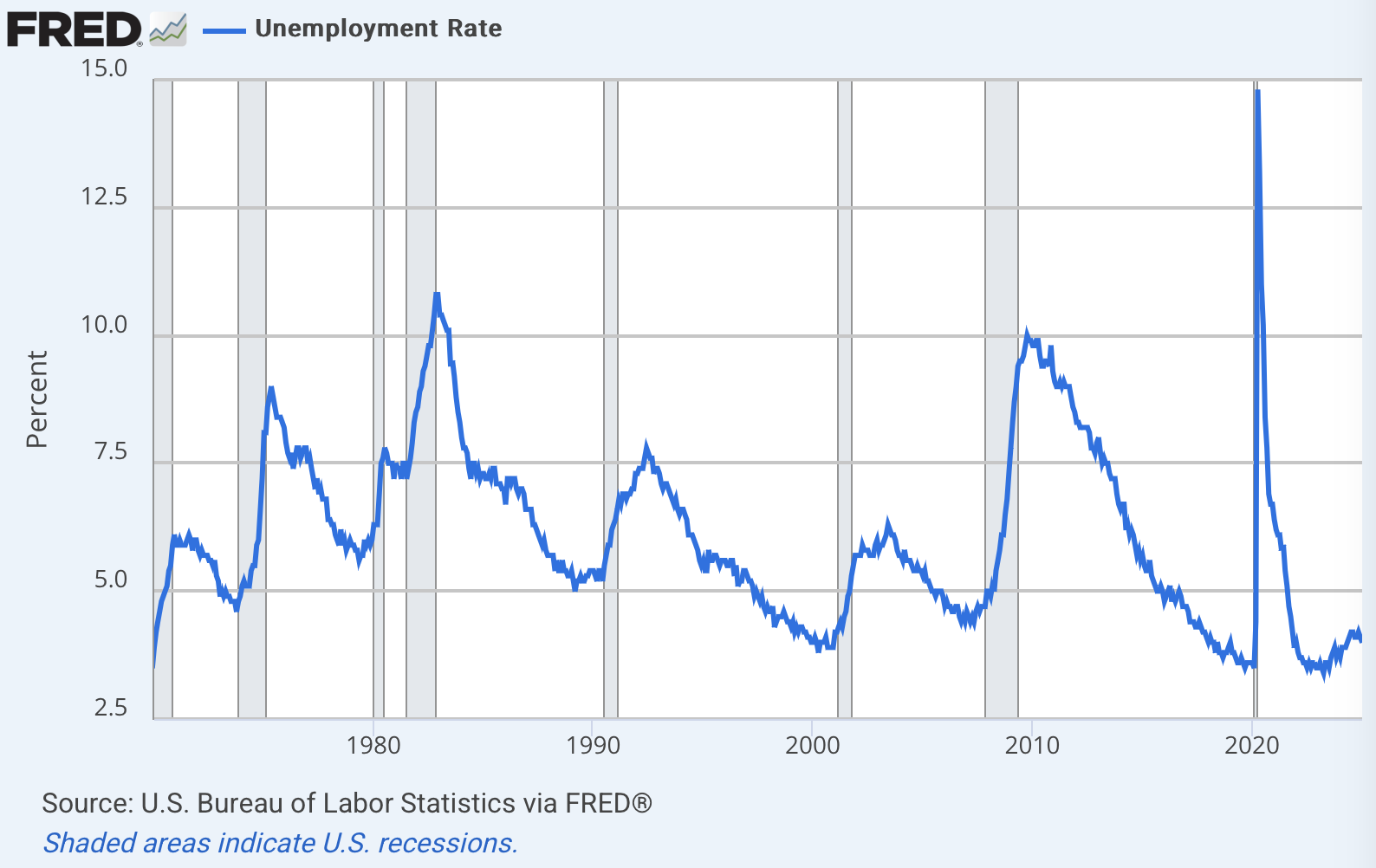

Are the good old days now?

Eddy Elfenbein notes that “except for January 1970, the unemployment rate is lower today than it was in every single month of the 1970s, 80s and 90s.”

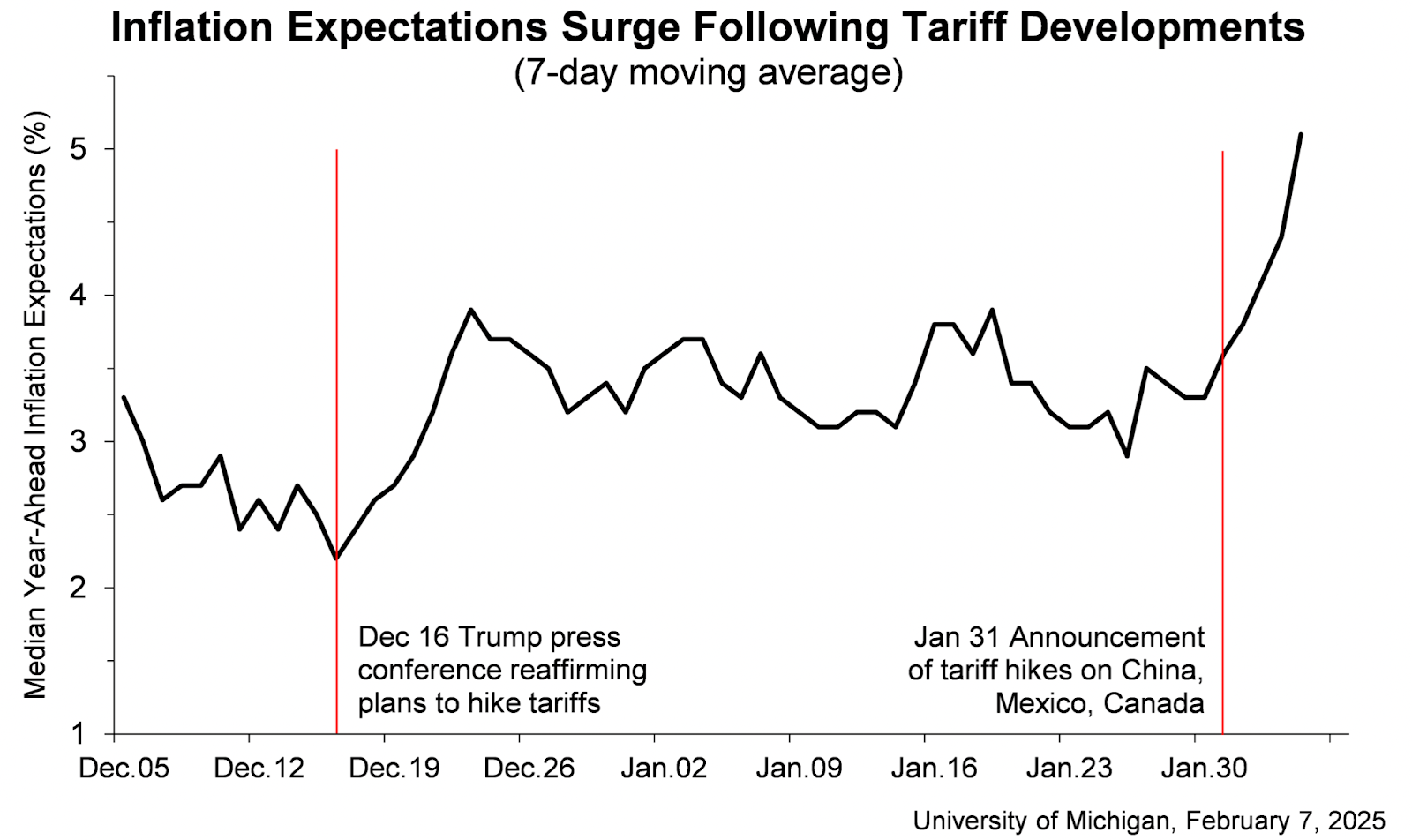

Are tariffs good or bad for inflation?

This morning’s University of Michigan consumer survey showed 1-year inflation expectations jumped a full percentage point, to 4.3% in January. 5-year inflation expectations rose to 3.3%, the highest level since 2008. These expectations are comically partisan, however, with Democrats suddenly expecting inflation to be much higher and Republicans suddenly expecting it to be much lower.

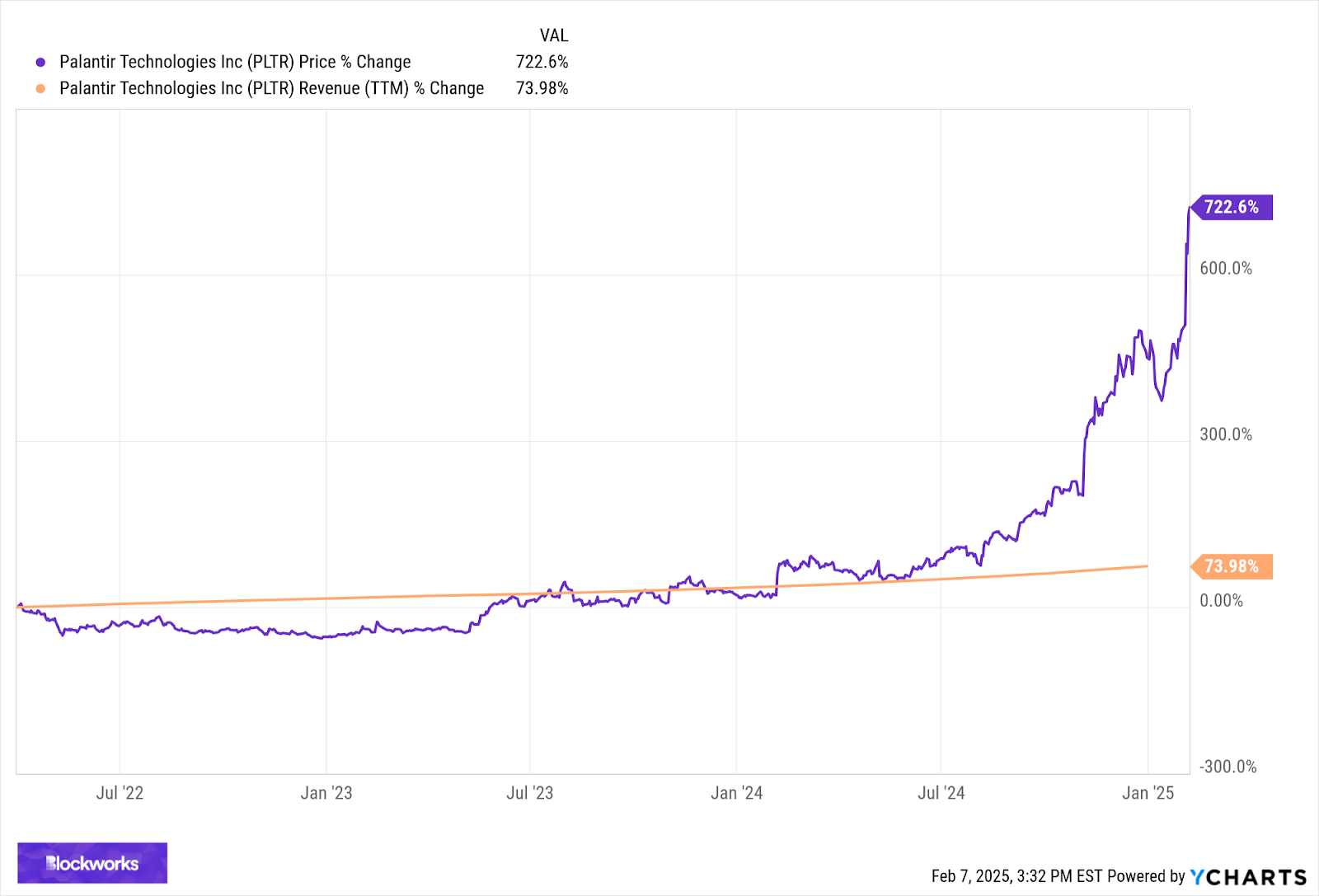

It’s good to be in the president’s orbit:

Shares of the Trump-aligned defense contractor, Palantir, rose about 40% this week after guiding 2025 revenue to about $3.7 billion — which is just 1/70th of Palantir’s market capitalization. A price-to-sales ratio of 70 is one measure of the value the market assigns to being in the president’s good graces.

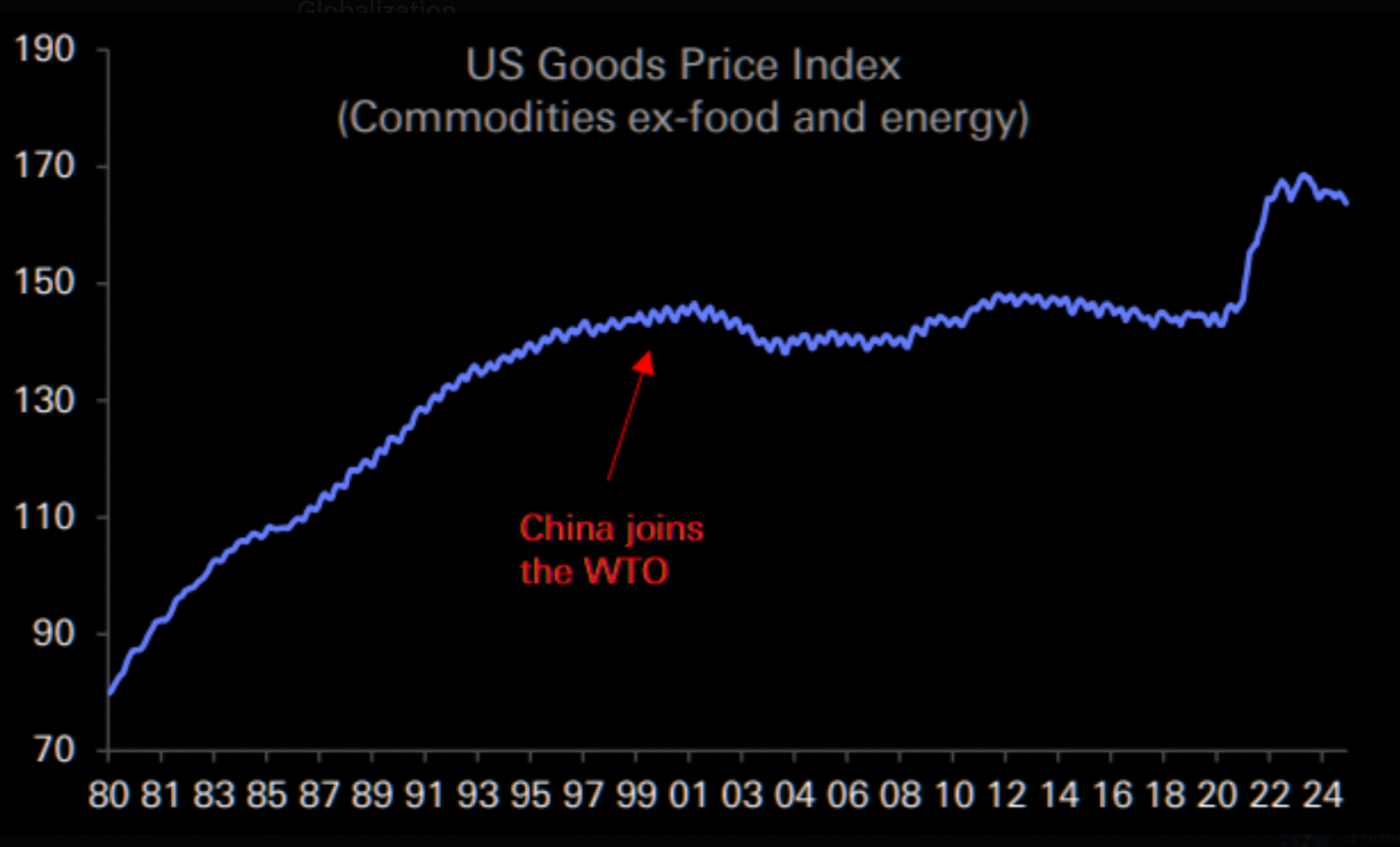

Is it good to be in China’s good graces?

@1MainCapital notes that the price of US goods were effectively unchanged in the 20 years following China’s admission to the World Trade Organization.

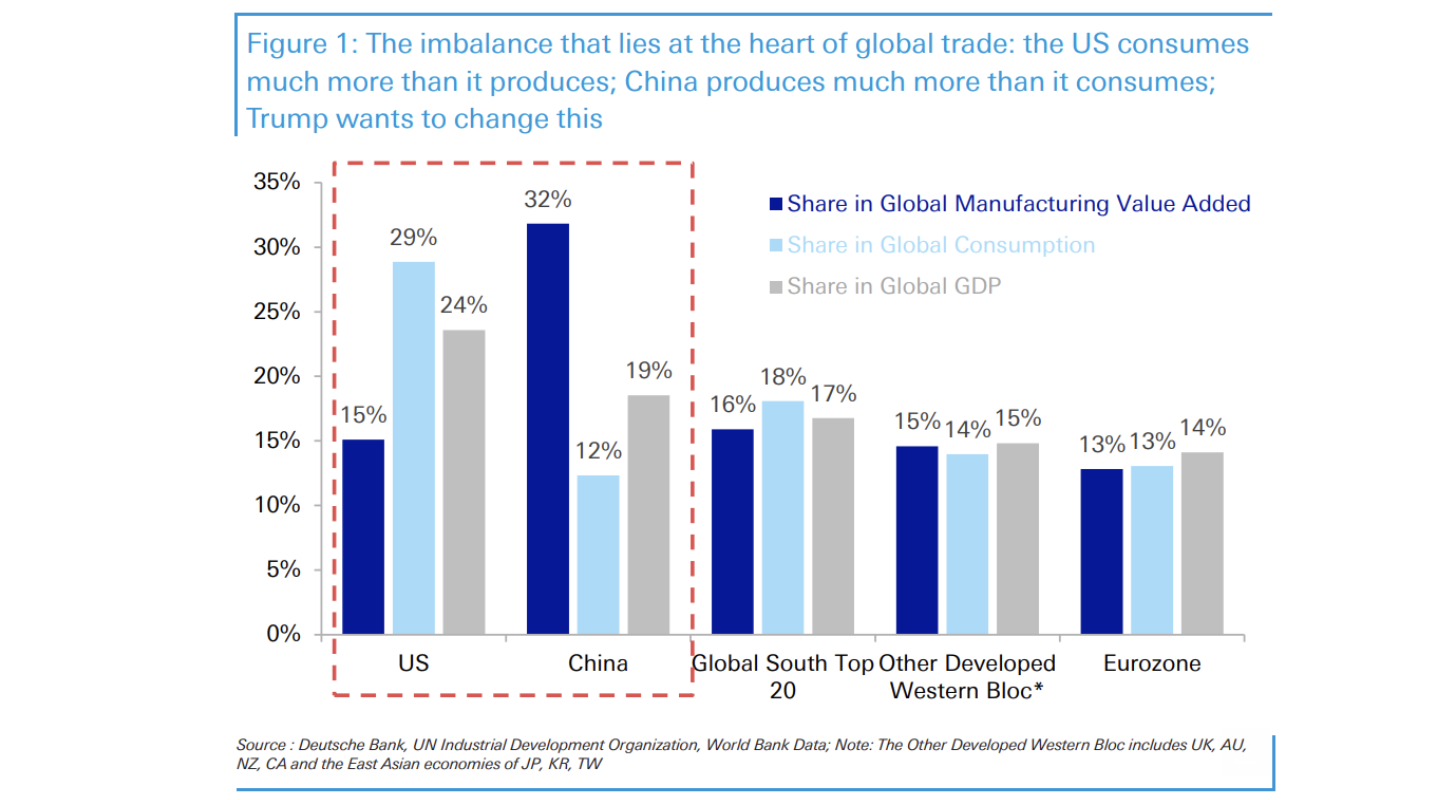

The president’s least favorite chart:

Per Deutsche Bank, the US accounts for 29% of global consumption but only 15% of global manufacturing output. In China, it’s the reverse: just 12% of global consumption but 32% of global manufacturing output. The president’s plan to change that with tariffs could prove costly: John Authers opined this week that “the greatest objection to this plan is that it’s stupid” and a WSJ op-ed called it “the dumbest trade war in history.”

Can we sell them some AI?

Amazon’s CEO indicated this week that the company would spend roughly $100 billion on AI infrastructure this year. Among other things, this represents a giant bet on Jevons paradox: “Companies will spend a lot less per unit of infrastructure, and that is very, very useful for their businesses,” Andy Jassy told investors this week. “But then they get excited about what else they could build . . . they usually end up spending a lot more in total.”

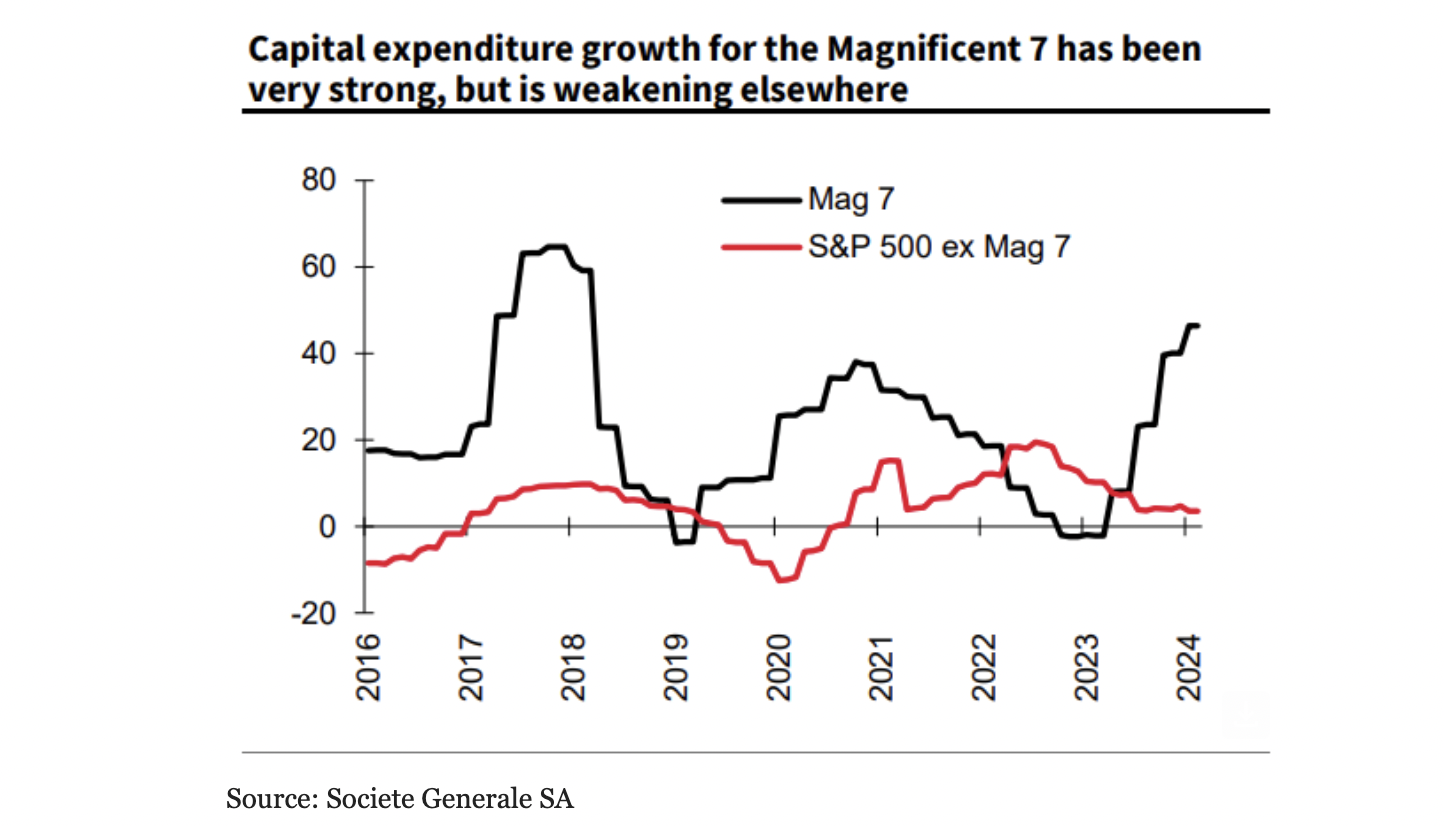

We’re goin’ all in on AI:

Soc Gen’s Andrew Lapthorne notes that while the Magnificent 7 increased capex by 40% last year, capex at the rest of the S&P 500 increased by just 3.5%.

Over-optimistic?

Inflows into outperforming US equities have accelerated since the election.

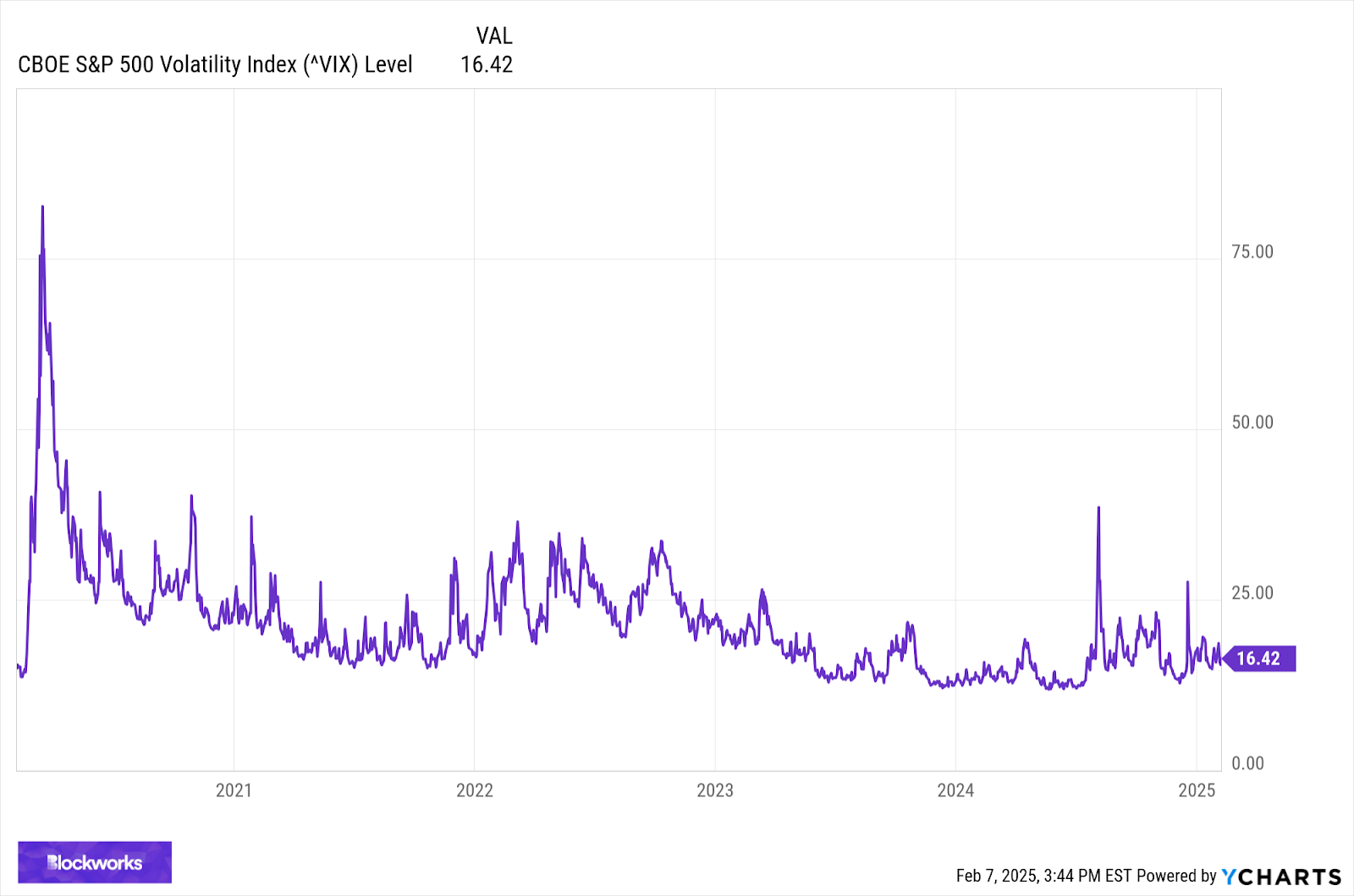

Under-concerned?

With the VIX at just 16, the market does not seem worried about the prospect of a trade war — or anything else, for that matter.

Let’s hope events don’t prove the market wrong.

Have a great weekend, eventful readers.

Brought to you by:

Tax time is here, but we've got good news! No more spreadsheets, no more headaches.

Easily integrate with every one of your crypto trading sources or wallets to track transactions, and generate accurate tax reports — all in minutes. Whether you're a casual trader or a pro, ZenLedger helps you stay compliant while minimizing tax liabilities. Our support team is here 7 days a week to help you get things done quickly and accurately.

Spend more time making money and less time worrying about what you owe.

Ethereum Interop, L2 Pain Points and Celestia’s Inflation

Tune in for insights on rollup design, token value accrual and private vs. public companies. Get Jill and Uma’s thoughts on reducing Celestia’s inflation and the Ethereum tariff debate.

Listen to Expansion on Spotify, Apple Podcasts or YouTube.

Brought to you by:

Hashrate Hackers, powered by Blockware, one of North America's leading Bitcoin Mining companies, announces the launch of a groundbreaking initiative aimed at blending the vibrant Ordinals community with the robust world of Bitcoin mining.

The vision: harness the network of an Ordinals community to install a $10m+ mining operation behind it and allow its Holders to compete for BTC rewards monthly.

Hashrate Hackers is where a store of culture creates a store of value. It turns collectors into contributors, and holders into participants of mining rewards.

The mission to redistribute wealth is realized through themed “Hacks” that allow holders to build their rigs and participate in races against the clock and leaderboards for BTC.

Mint Details:

February 11, 2025

Price:

0.015 BTC per Ordinal

Follow our Twitter and join our Telegram group for the upcoming details.

Passive funds now have $16T in assets, which is 52.6% of the whole (fund) enchilada after picking up 2% share last year. Passive equity is 63% share but passive bonds its 37%. (passive = index-based funds incl smart-beta). Whole fund enchilada owns 26% of stock mkt via @JSeyff

— Eric Balchunas (@EricBalchunas)

8:45 PM • Feb 7, 2025

How should we measure DA market share?

It's been cool to see Celestia climb in DA market share, but the critics have a point that market share of total data posted is a pretty weak metric

DA *fee* market share is probably more useful, but it doesn't tell you much either at this… x.com/i/web/status/1…

— Nick White 🦣 (@nickwh8te)

4:45 PM • Feb 7, 2025