- The Breakdown

- Posts

- 🟪 Friday Lunar Charts

🟪 Friday Lunar Charts

It was yet another week of all-time highs in US equities this week, in part because Chair Powell encouraged us to continue ignoring him.

This issue is brought to you by:

“Keep your eyes on the stars, but your feet on the ground.”

- Theodore Roosevelt

Friday Lunar Charts

It was yet another week of all-time highs in US equities, in part because Chair Powell encouraged us to continue ignoring him.

In his testimony to Congress on Wednesday, he told us the economy is good, inflation is going in the right direction, and suggested that the next move in Fed Funds will be down despite some recent rumblings to the contrary.

There’s nothing to see here, in other words.

Monetary policy is unusually restrictive as Fed Funds remain “far from neutral,” but the market has long since stopped worrying about that.

As long as it’s not getting more restrictive, as Powell reassured us it would not, we can continue to focus on the fun stuff — mostly AI.

There was a lot of AI this week!

Broadcom had a big earnings beat on better-than-expected AI demand, eBay said it’s piling into GPUs, a Fed survey said AI automation is saving US businesses money and Microsoft said the AI copilot for writing code is proving so useful that their customers’ main concern is deciding what to do with their newfound free time.

There are, however, some signs that the AI story is getting a little long in the tooth.

Broadcom traded lower after its great results, for example. Alphabet is now down on the year as AI seems to be generating more costs than revenues for them. Tesla is down 30% on the year as Musk has failed to convince us that his car company is actually an AI company.

The Magnificent 7 has been reduced to the Magnificent 2: NVDA +84% and META +46% YTD.

But this is all short-term, tactical stuff and we should probably be thinking much bigger — maybe even as big as China and Russia, who announced plans this week to build a nuclear power plant on the moon.

The plant, to be completed by 2035, will be built and maintained by “jumping” robots, which I assume will also be artificially intelligent. (Why jumping, I don’t know. Maybe they’ll be putting up a basketball hoop for them?)

I think it’s worth noting here that 2035 is only 11 years away (yes, I did that math in my head).

Stocks may look expensive as they keep making new highs in 2024, but where do you think they’ll be when intelligent robots are building power plants in outer space?

I’m guessing a lot higher.

But the first job is to survive that long, so let’s keep our feet on the ground with some charts.

Reaccelerating?

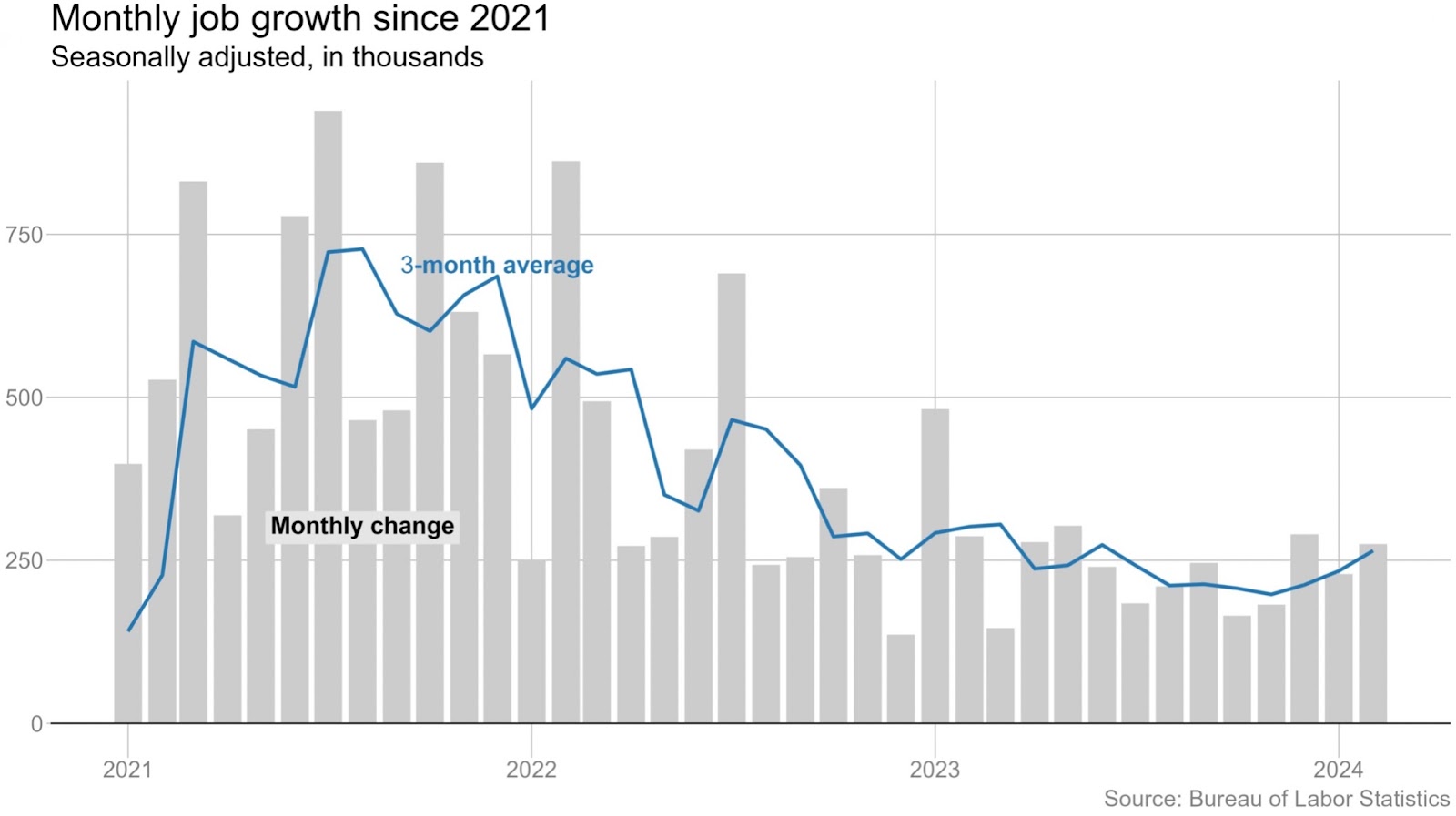

This morning’s jobs data was a little choose-your-own-adventure — whatever your bias was about the economy, it was likely confirmed. February payrolls were up 275k vs 200k expected, but revisions subtracted 167k from January’s data. Average hourly earnings were up a modest 0.1% month-on-month, but a solid 4.3% year-on-year. This confirms my bias that the economy is not-too-hot-not-too-cold and just right for risk assets.

Still very good:

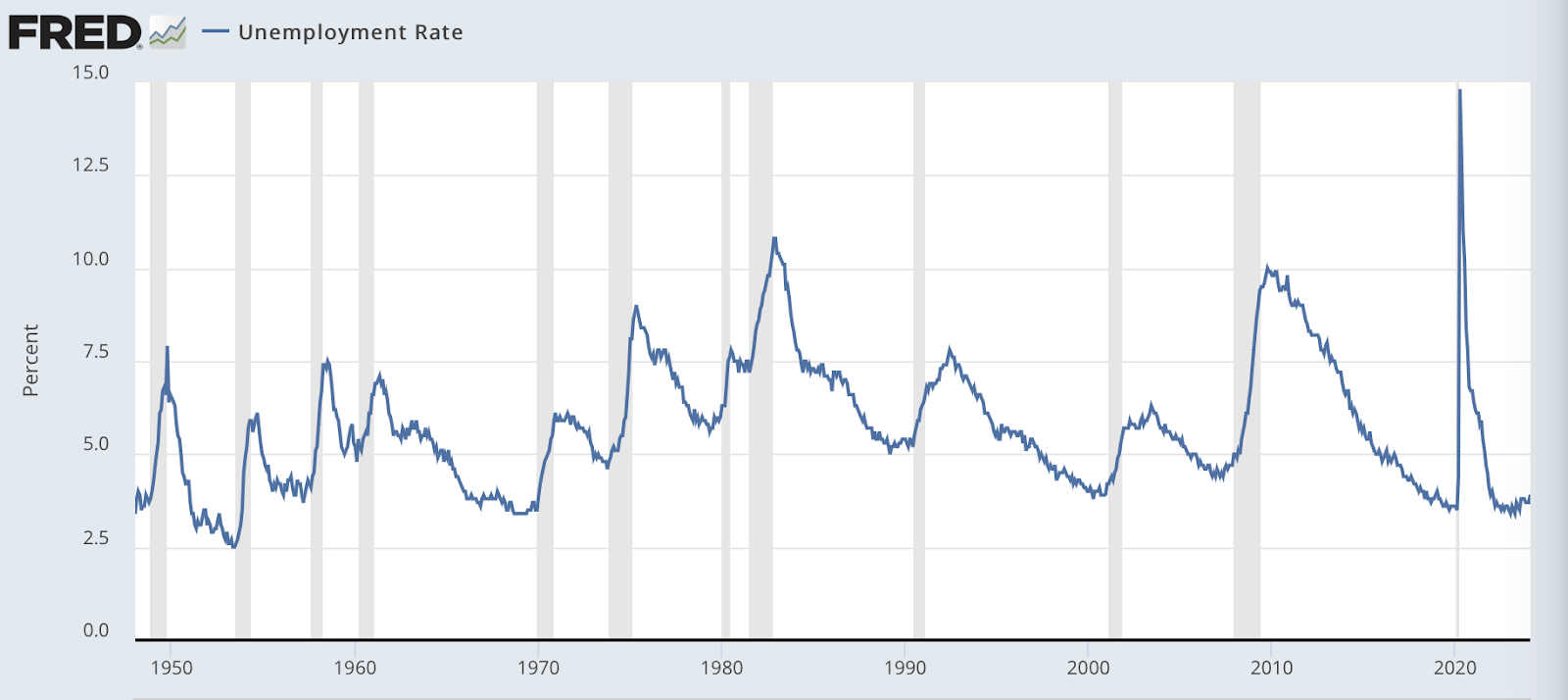

The US unemployment rate ticked up to 3.9% in February, which some will see as the start of a trend change higher. But February was the 25th consecutive month below 4%, which still seems like something to celebrate.

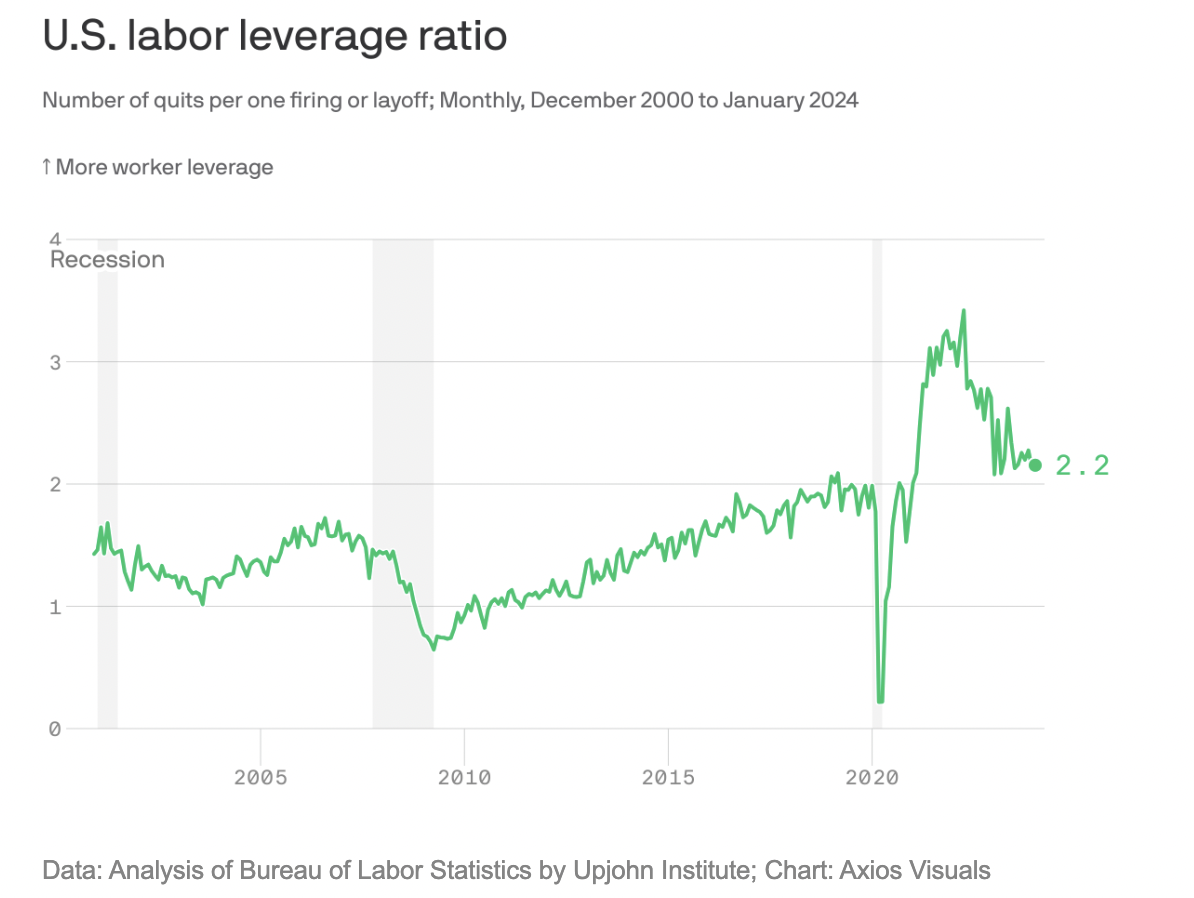

Take this job and…

Fewer people told their employer to shove it in February, but the ratio of quits to layoffs continues to favor employees. That seems like a happy medium to me, but this may just be a bad time to transact, in jobs or otherwise, as Conor Sen notes.

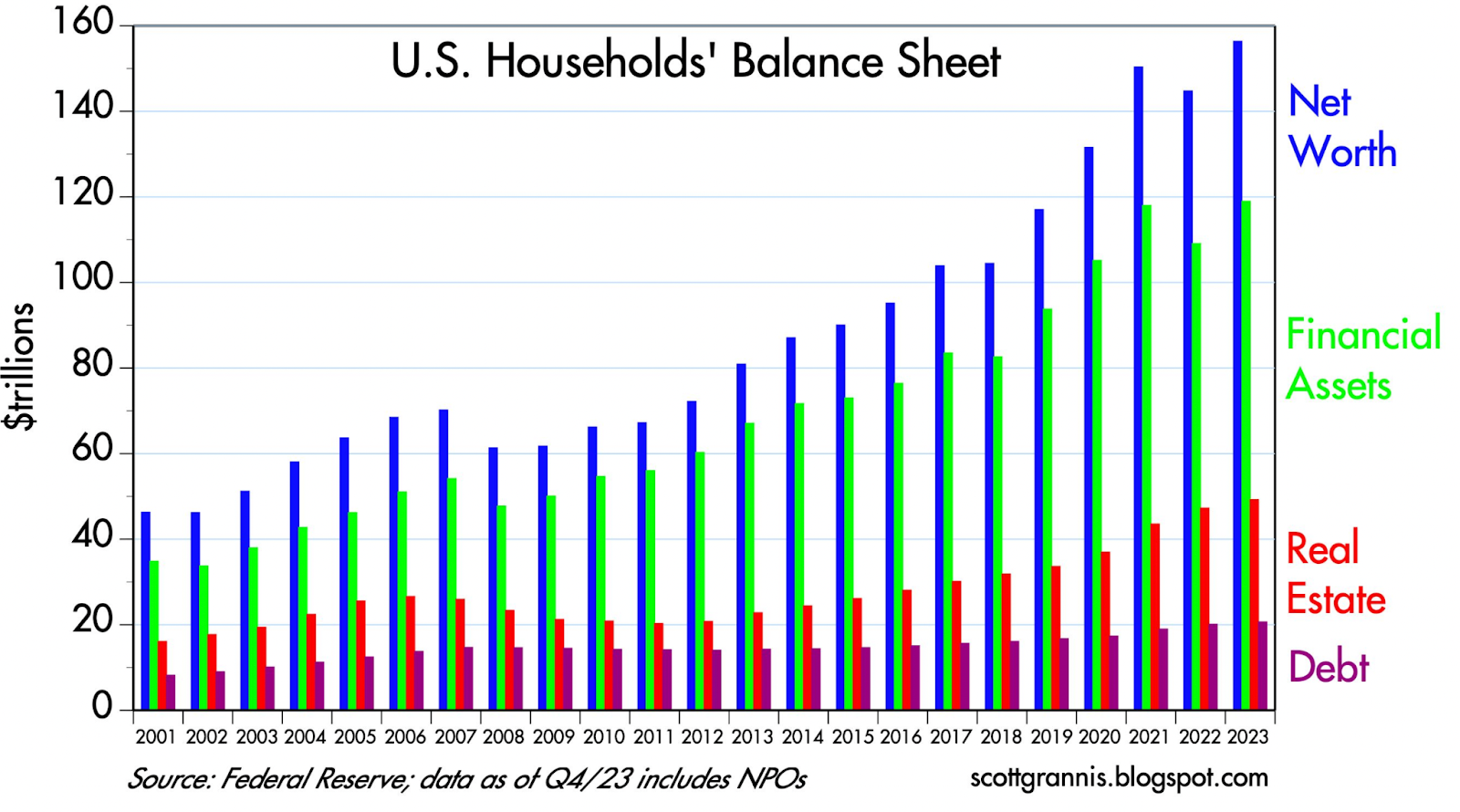

Wealth is making new highs:

Fed data out this week shows that the US private sector’s net worth (assets - liabilities) ended 2023 at a record $156 trillion. That is not adjusted for inflation, but neither are asset prices — something to keep in mind when risk assets are also making new highs.

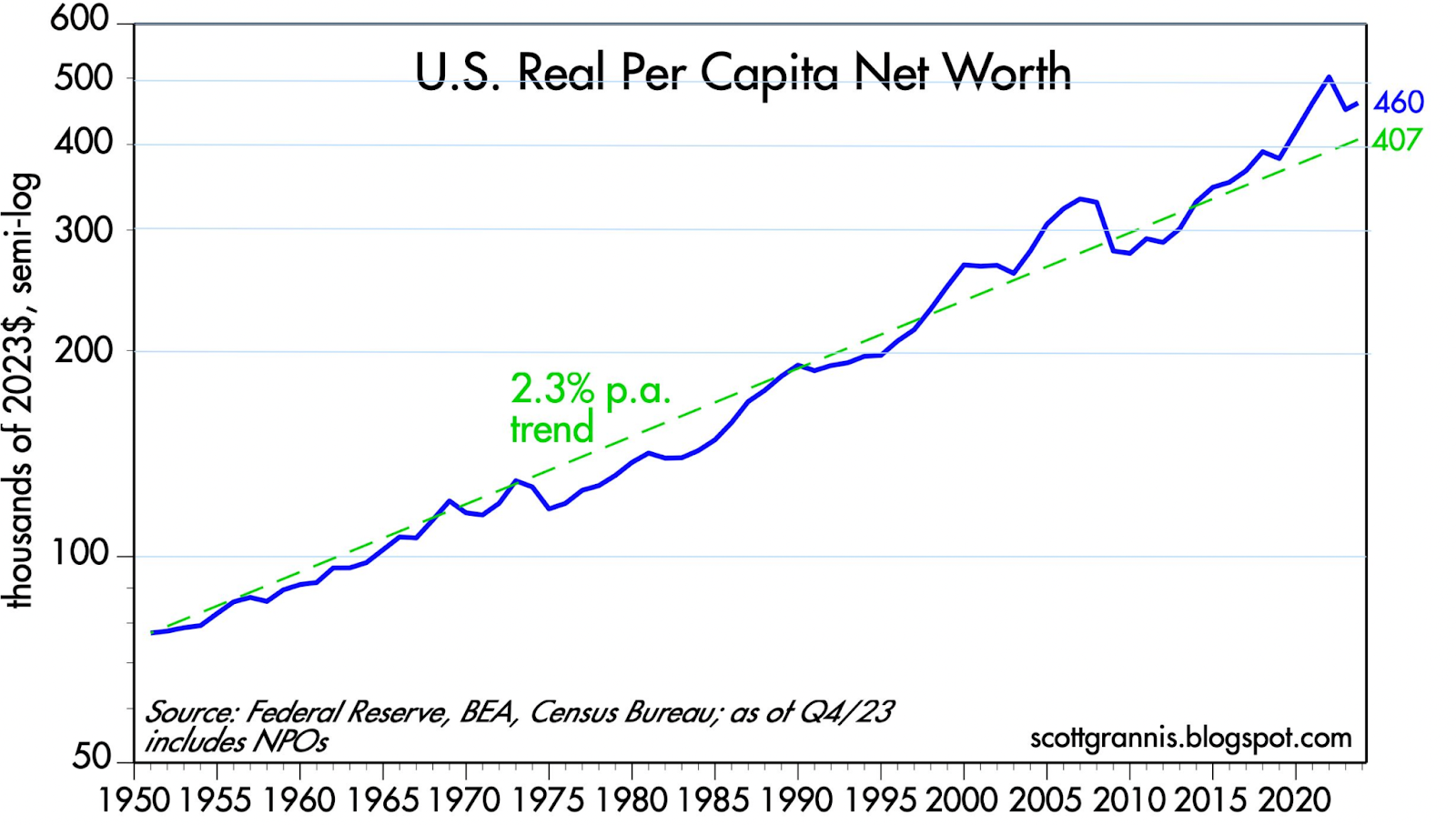

We’re doing pretty good even after inflation:

Scott Grannis adjusts the Fed’s data on net worth for both inflation and population growth and finds that we are off the highs of 2021, but still above trend. Things are good.

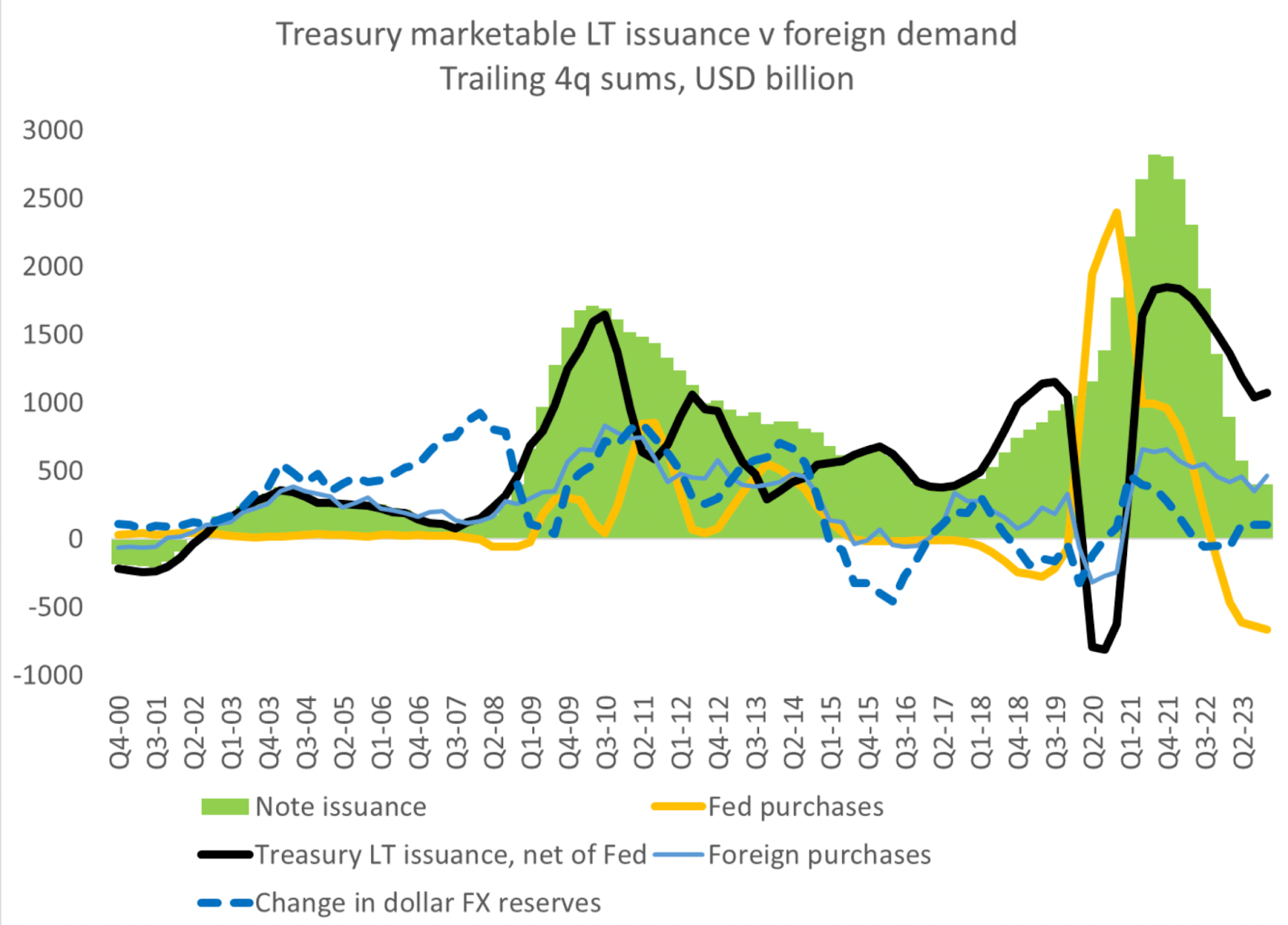

It’s not just Americans that are flush with cash:

This surprising chart from @Brad_Setser shows that foreign demand for long-term US Treasurys ($450 billion in Q4) now exceeds net issuance of those Treasurys ($400 billion in Q4). I would not have guessed that.

If there’s enough money around to buy US debt as fast as the US government is printing it, there’s probably at least enough money around for another few weeks of all-time highs.

Have a great weekend, wealthy readers.

This issue is brought to you by:

Vertex is a leading DEX on Arbitrum offering spot, perpetuals & money markets with unified cross-margin.

Trade with lightning-fast speeds and super-low fees across 30+ markets.

Unleash your trading with Vertex Edge – multiple chains, one layer of synchronous order book liquidity.

Top Stories

Wyoming passes law to give DAOs a nonprofit legal framework — Read

Bitcoin price briefly tops $70K to reach new all-time high — Read

Worldcoin wants to pursue legal action against Spain over data block — Read

Ethereum hits $4K for first time since December 2021 — Read

TRON DAO at ETH Denver and host of TRON Builder Tour Denver stop [Sponsored] — Read

We're Watching

In this week's roundup the Bell Curve crew is joined by Sergey Nazarov, co-founder of Chainlink, joins us to discuss the evolution of Chainlink from a focus on price feeds to a platform for data, compute, and cross-chain services.

Thank you to our sponsor:

Delivering trust, reliability and deep institutional liquidity, LMAX Digital today serves the largest financial institutions, globally.

It also contributes real-time market data to the industry’s leading reference rate indices and provides real-time volume data feeds to major institutional analytics providers.

LMAX Digital is regulated by the Gibraltar Financial Services Commission (GFSC) as a DLT provider for execution and custody services.

Daily Insights

Solana Season Continues on the back of the Memecoin Frenzy and Potential Airdrops

1) DEX Volume

On 5 March, the daily trading volume of Solana has reached a new ATH with $3.4B Volume. $534M volume (15%) is driven by Memecoin2) MEV Tip

A new ATH for @jito_labs Validator Tip on… twitter.com/i/web/status/1…— Tom Wan (@tomwanhh)

12:09 PM • Mar 8, 2024

Let’s look at some historical examples to see how correlated approval ratings have been to stock market performance (and by implication the prospect for a regime either continuing or changing). 🧵

— Jurrien Timmer (@TimmerFidelity)

5:02 PM • Mar 8, 2024

What's going on with the US job market?

Thread.

1/

— Alf (@MacroAlf)

4:33 PM • Mar 8, 2024