- The Breakdown

- Posts

- 🟪 Friday profitable charts

🟪 Friday profitable charts

Dreamers and doers are building amazing stuff

Byron Gilliam

February 28, 2025

Brought to you by:

“The world needs more dreamers and doers, not just talkers.”

— Jensen Huang

Friday profitable charts

Warren Buffett appears to be concerned: Berkshire Hathaway ended 2024 holding $334 billion of cash, more than double its holdings at the end of 2023.

Even more telling, Berkshire bought just $9.2 billion of stock in 2024, while selling more than $143 billion.

Buffett hates paying capital gains taxes and his favorite holding period is “forever,” so he must think stocks have gotten very expensive to be selling like that.

Helpfully, the value investor and Buffett acolyte Chris Bloomstran is willing to put a number on just how expensive that might be.

In his 167-page annual letter, Bloomstran estimates the intrinsic value of the S&P 500 index at $3,500.

The S&P closed today at just under $6,000 — nearly 70% higher!

Bloomstran cites persistent budget deficits, elevated interest rates, poor growth prospects and peak profit margins for his assessment that the S&P 500 should be worth just $3,500 — 15x his estimate of the index’s operating earnings ($233).

If he’s even half right, investors are likely in for a long run of disappointing returns.

Research Affiliates, for example, predicts that large US growth stocks will return just 1.8% annually over the next decade (well below the rate of inflation).

Those negative real returns might be front-loaded, of course, because investing bubbles always pop far faster than they inflate.

But stocks can be expensive without being in a bubble — Howard Marks notes that bubbles are “more a state of mind than a quantitative calculation.”

If so, this week’s events suggest we’re not in one.

Nvidia reported another astounding set of quarterly numbers with revenue up 78% to $39 billion (in a single quarter!).

Those kinds of results also seem likely to continue: CEO Jensen Huang says demand for Nvidia’s newest generation of GPU is “amazing.”

And yet, the shares finished 9% lower on the week.

That puts NVDA on a modest 27x forward P/E multiple — hardly the “irrational exuberance” that Marks would say is indicative of a bubble.

Investors might even be irrationally gloomy, given what’s going on in Silicon Valley at the moment.

The writer and investor Azeem Azhar shared on a podcast this week that “it’s not unheard of” to find early-stage AI startups growing revenue at 7% per week.

This kind of growth, he says, is unprecedented, even by the standards of Silicon Valley.

“In a pre-gen AI world it used to take an exceptional team of six or seven about a year to get to a million dollars in annual recurring revenues (ARR). Today, [we’re] seeing teams of two founders get to the milestone in under three months.”

Like me, you’re probably not invested in any of those startups, but there’s good news for us retail investors, too.

AI startups, Azhar says, are growing revenue faster than the Big Tech companies (that we’re all invested in) are growing AI infrastructure.

Sam Altman seemed to confirm this yesterday in reporting that OpenAI has run out of GPUs.

And AWS suggested the same: “If we had more capacity than we already have…we could monetize it."

Most of that capacity is being used for business productivity things, which are maybe not so exciting.

But we’re now also getting robots working in factories, a little cat robot to blow on your coffee for you, fleets of self-driving cars, brain-balancing headsets to relieve depression, a two-way brain-computer interface and robots that provide emotional support.

So, investors may be right to worry that stocks are expensive, but there may be a reason they’re expensive — the dreamers and doers are building some amazing stuff.

Let’s check the charts.

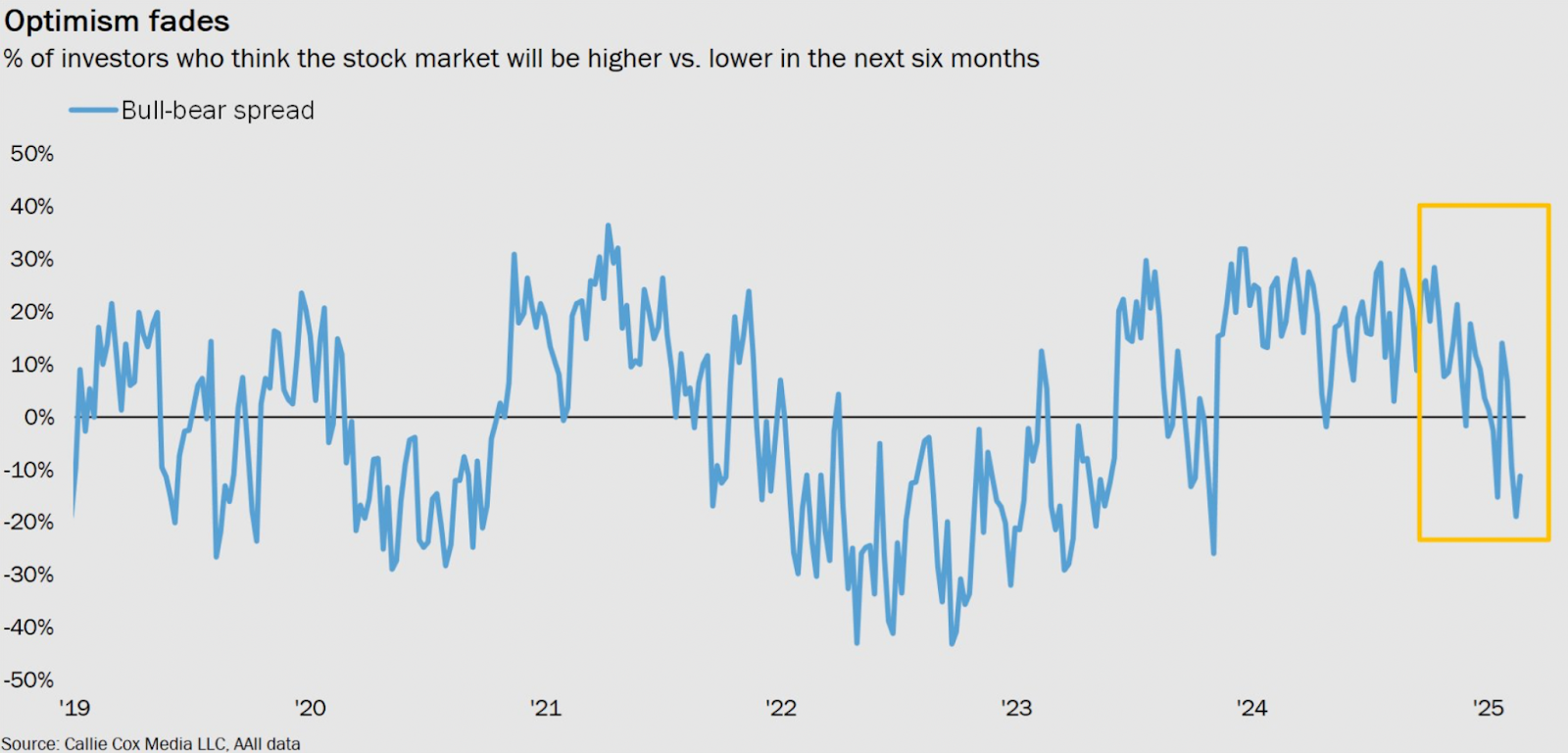

Irrational gloom?

Investor sentiment surveys are generally a trailing indicator of stock prices and therefore worthless. So it’s interesting to see the AAII survey turn bearish while the market is still so close to its all-time highs. Have investors for once figured out something ahead of the market? I’m not sure that’s even possible, but that’s kind of how it felt this week.

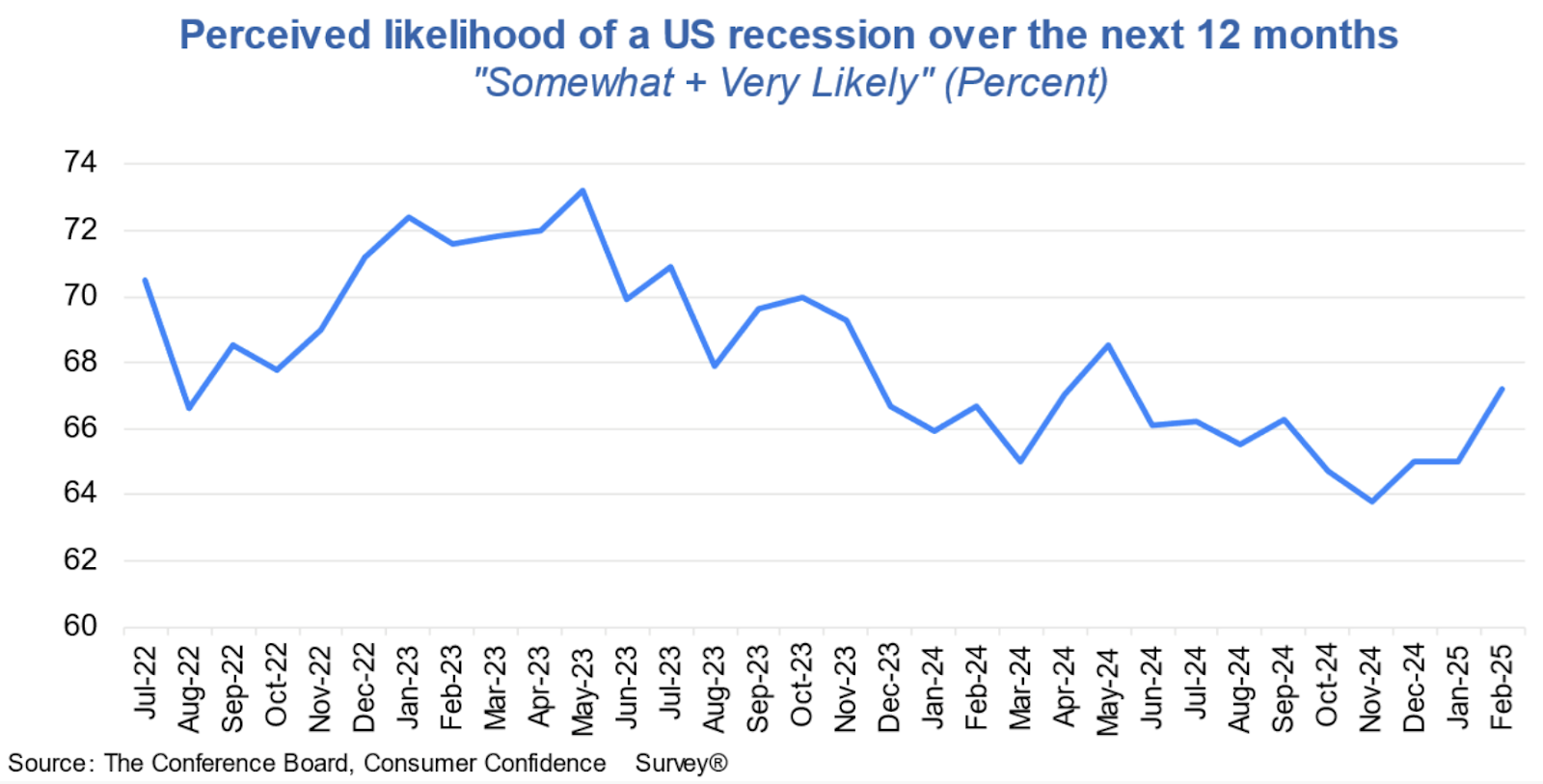

Consumers are gloomy too:

The Conference Board’s survey of consumer confidence fell 6.7 percentage points in February, the largest drop since 2021. Consumers’ expectations of recession (above) bottomed around the election and have been trending up ever since.

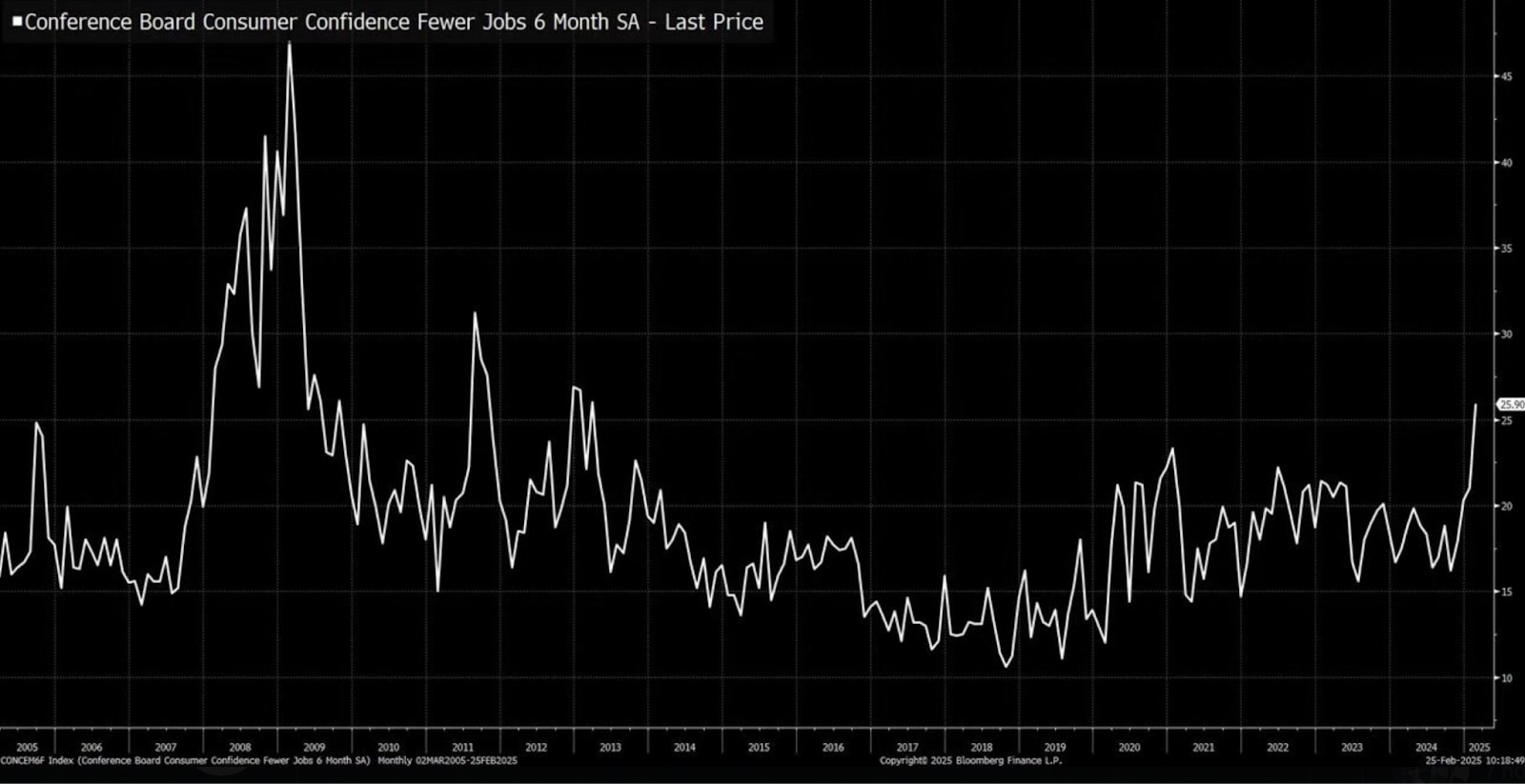

A gloomy outlook on jobs:

The same survey found that expectations of jobs being harder to find six months from now jumped to its highest level in over a decade. (A decade that included a global pandemic!)

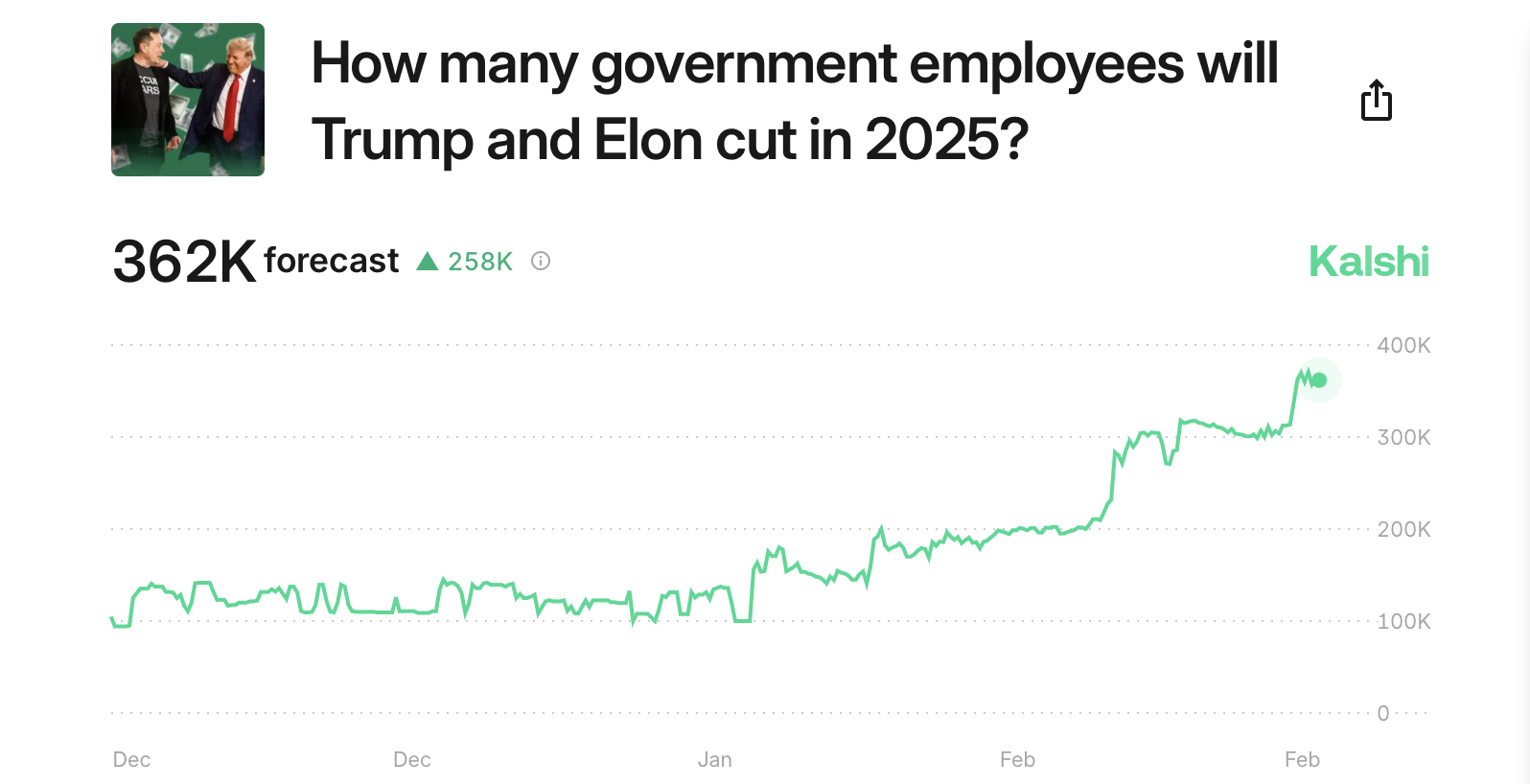

Government jobs:

Betting markets suggest people expect 362,000 US government employees to lose their jobs.

MEGA > MAGA?

Despite Trump’s tariffs and the situation in Ukraine, the Stoxx Europe 600 hit a record high this week. It’s now up 9% on the year, vs. the S&P 500 at just unchanged. Could Trump accidentally make Europe great again? If his hostility inspires a defense spending boom (invested at least partially in drones), he might.

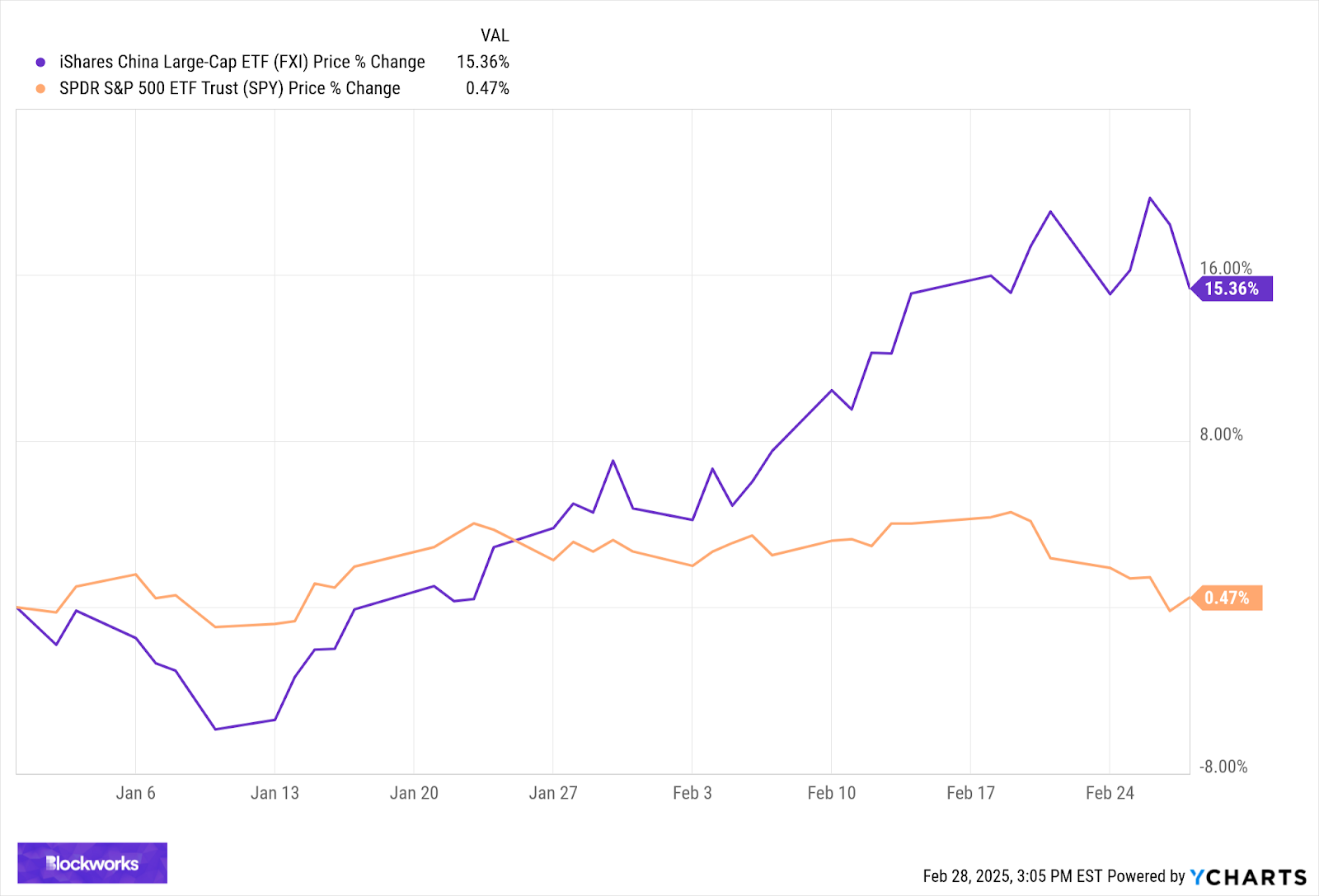

Making China great again?

Despite Trump adding an additional 10% tariff on imports from China this week, the iShares China large-cap ETF is up 15% year to date. (The broader Shanghai Composite Index is just unchanged, however.)

US home sellers are gloomy:

Pending US home sales fell to their lowest level on record (since 2001).

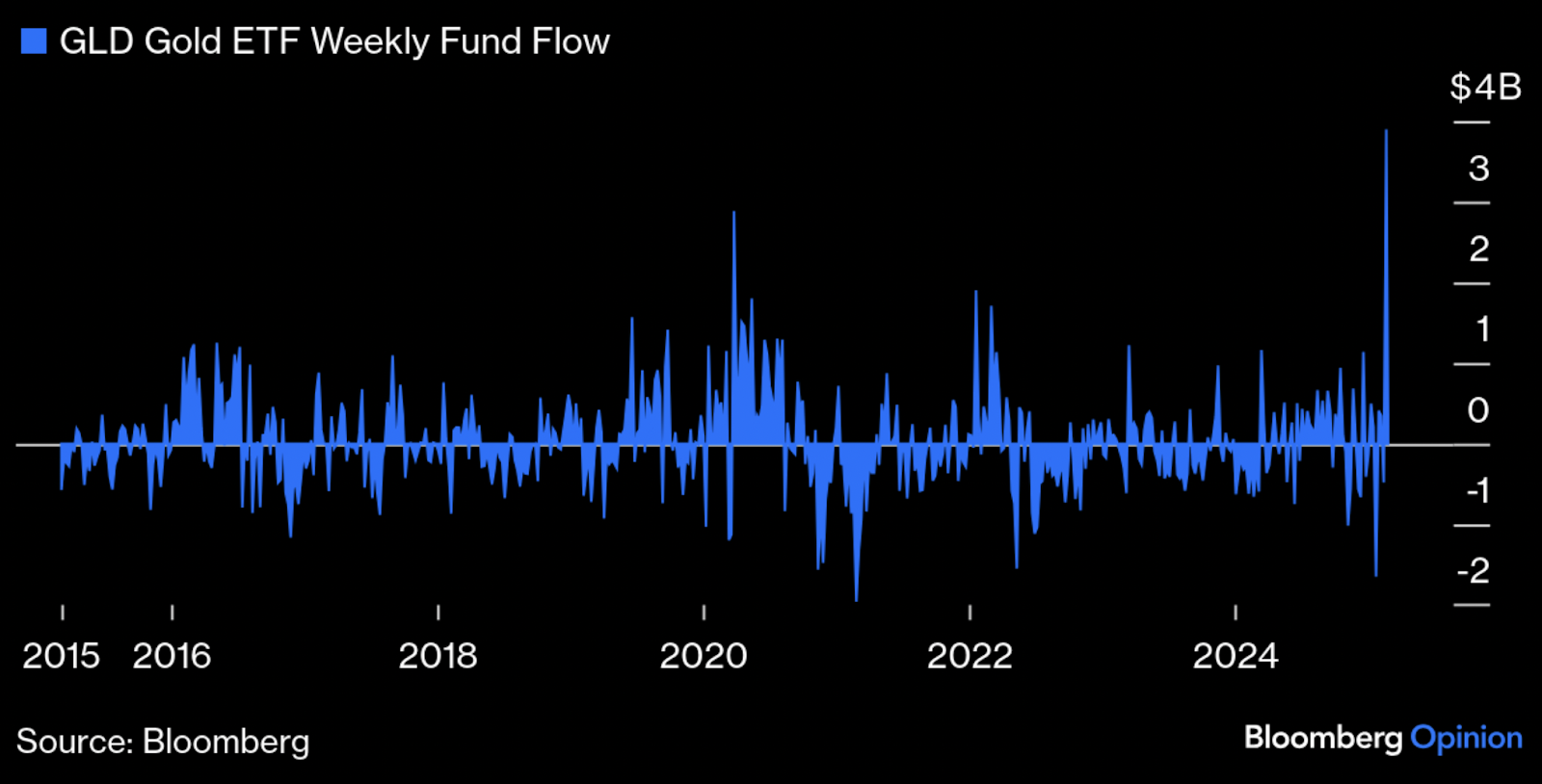

Seeking safety:

US investors poured a record $4 billion into the largest gold ETF, GLD. (ETFs for digital gold, however, saw billions of outflows.)

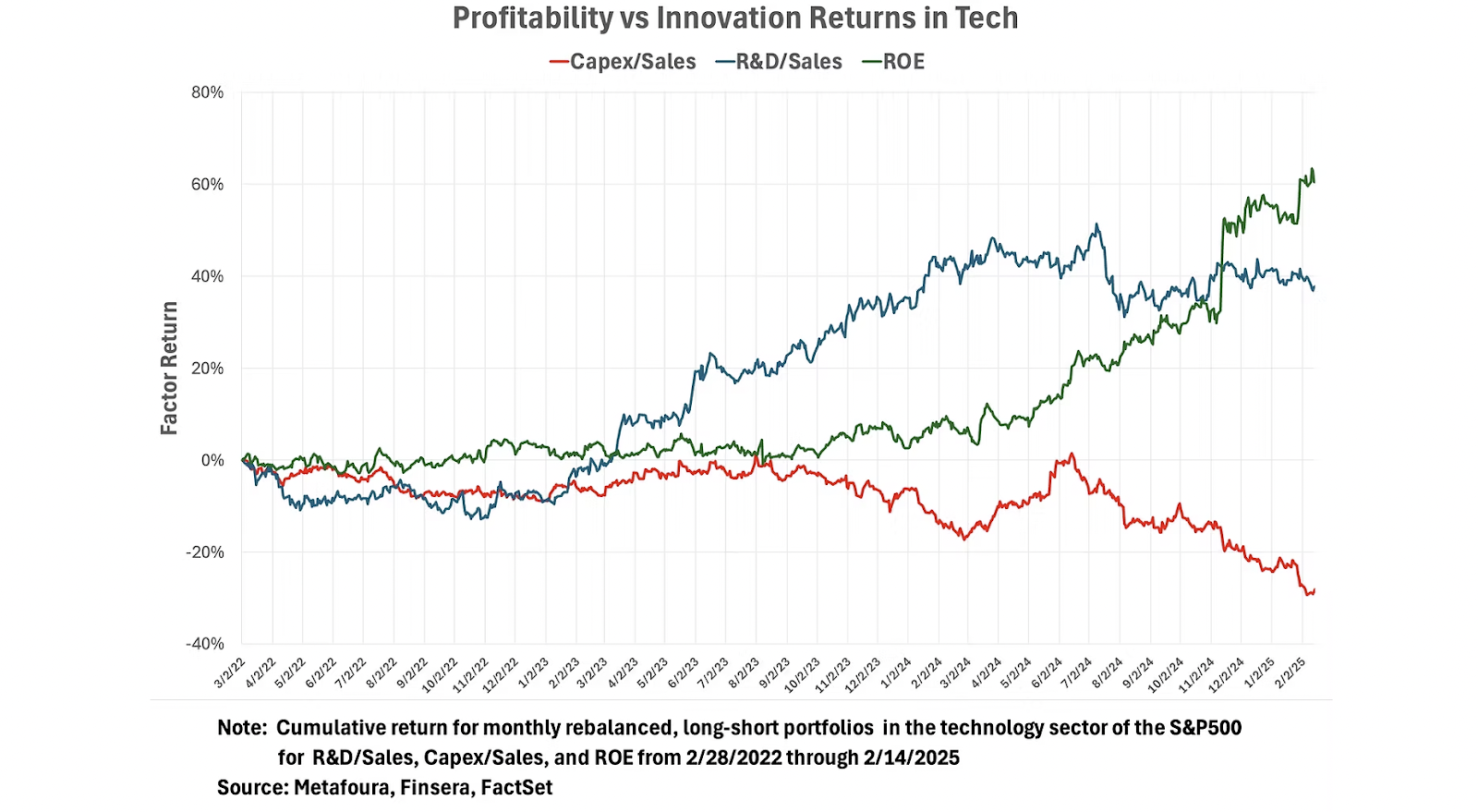

Even tech investors are seeking safety:

This chart from Joseph Mezrich shows that investors have been punishing high-spending companies (the red line) and rewarding highly profitable ones (the green line).

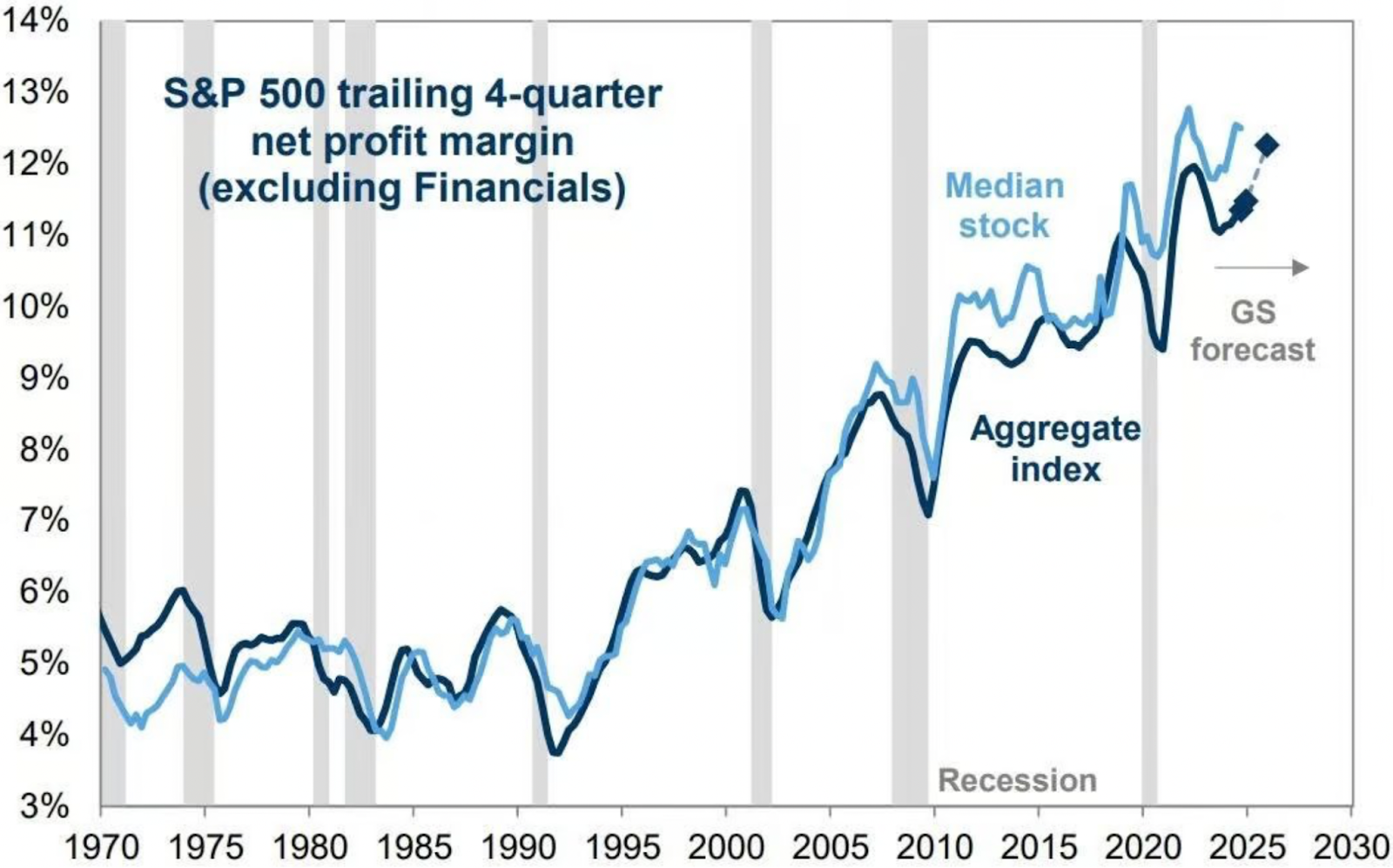

Contra-Bloomstran:

Analysts at Goldman Sachs expect that profit margins for US companies will continue to expand.

It’s presumably no coincidence that those profit margins have been trending up ever since the dotcom bubble.

If we can look back 30 years and say the same about the AI bubble, we may wonder what everyone was so worried about.

Have a great weekend, profitable readers.

Morpho is the first and only DeFi protocol integrated by Coinbase. As the go-to infrastructure for onchain loans, Morpho’s immutable code sets the gold standard for decentralization, giving builders full ownership and control.

Leverage Morpho’s flexibility to create lending and borrowing solutions tailored precisely to your users’ needs.

ETHDenver Vibe Check: The End of the Beginning?

Live from ETHDenver, this episode tackles subdued conference vibes and broader industry sentiment. Tune in for insights behind the rise and fall of memecoins and the shift from idealism to pragmatism in crypto startups.

Listen to Expansion on Spotify, Apple Podcasts or YouTube.

With capital rotating, regulation evolving, and liquidity shifting, the smartest players are already adjusting.

Paul Brody (EY) on where enterprises are deploying blockchain beyond the headlines.

Ambre Soubiran (Kaiko) on the market trends that funds are acting on before retail catches up.

Jake Chervinsky (Variant) on the legal shifts that could create—or kill—new opportunities.

Rob Hadick (Dragonfly) on the allocation strategies driving institutional plays this year.

Some will watch. Others will act. Which side are you on?

📅 March 18-20 | NYC

Sitting here listening to @SenLummis at the @APompliano Bitcoin Investor Week. What an incredible leader on Bitcoin.

What occurs to me is that the political shift we’ve seen recently in Washington is just a down payment on where we are going.

Remember when Fidelity launched its… x.com/i/web/status/1…

— Matt Hougan (@Matt_Hougan)

5:05 PM • Feb 28, 2025

First official episode is live! ⚡️

We discuss:

- Whether Jack Dorsey is Satoshi

- The threat vectors for Bitcoiners

- Attack stories and how to protect yourself

- Rapid-fire Q&A at the end!Timestamps:

00:00 Introduction

01:01 Is Jack Dorsey Satoshi Nakamoto?

05:50 Debunking… x.com/i/web/status/1…— Supply Shock (@SupplyShockBW)

3:40 PM • Feb 28, 2025