- The Breakdown

- Posts

- 🟪 Friday Smoot-Hawley charts

🟪 Friday Smoot-Hawley charts

On forgetting hard-won lessons from the past

Byron Gilliam

March 07, 2025

Brought to you by:

“I beseech you, in the bowels of Christ, think it possible you may be mistaken.”

— Oliver Cromwell

Friday Smoot-Hawley charts

This was the week markets finally beseeched President Trump to think it possible he may be mistaken.

The S&P 500 fell 2% on Thursday despite the good news that some of the president’s threatened tariffs were being delayed — a distinct change of tone from as recently as a few weeks ago when markets were sure that tariffs were just a negotiating tactic.

When asked what he made of the market’s selloff this week, the president responded, “I think it's globalists that see how rich our country's gonna be and they don't like it.”

This seems unlikely to me, because in my experience, globalist investors are generally in the business of buying the stocks of countries they believe will be rich — and people who don’t like to see the US get rich generally don’t have any US stocks to sell.

Also, nearly every economist believes that tariffs are likely to make the country poor.

“The trouble with tariffs,” David Kelly wrote this week, “is that they raise prices, slow economic growth, cut profits, increase unemployment, worsen inequality, diminish productivity and increase global tensions.”

“Other than that,” he added, “they’re fine.”

Things are already not fine.

Strategists at Bank of America warn that the biggest risk from tariffs is a “self-fullfilling slowdown due to corporate uncertainty” — a risk that was probably realized this week.

On the same day that President Trump finally imposed tariffs on Canada and Mexico, his commerce secretary said he might roll them back “tomorrow”; automakers were then granted an exemption that’s good for one month; the White House said the president was “open” to other exemptions; on Thursday the president suspended most of the tariffs he imposed on Tuesday by exempting goods covered by USMCA (the trade deal he negotiated in his first term); on Friday, the president threatened 250% tariffs on Canadian lumber and dairy products.

If anyone was planning to build a factory anywhere in North America, there’s a good chance those plans are now on hold.

Responses from the latest ISM manufacturing report, collected before this week’s roller coaster, already paint a picture of customers afraid of placing orders and executives afraid to invest.

It’s only likely to get worse.

Secretary Lutnick told CNBC that much of the tariffs either imposed or threatened this week will be superseded by “reciprocal tariffs” to take effect on April 2.

If "reciprocal" sounds reassuringly non-threatening to you, think again: The Economist warns that “reciprocal tariffs would strike a fatal blow to the global trading system.”

Worryingly, Lutnick also said that these tariffs will “start high” before decreasing.

This doesn’t make much sense, seeing as the whole point of being “reciprocal” is to simply match the rates that other countries impose.

But it will be a nightmare of uncertainty either way: The Economist estimates that fully reciprocal tariffs would entail 2.3 million individual levies.

Imagine the lines of trucks that will form at the Canadian border as US customs officers try to figure out who should pay which of the 2.3 million possible tariff rates.

(Current USMCA rules are already so complicated that importers often choose to pay tariffs instead of spending the time and money to figure out if they’re exempt.)

Or, even worse, imagine a line of almost no trucks.

After Smoot and Hawley raised tariffs by just seven percentage points (from 40% to 47%), trade between Canada and the US collapsed by more than 75%.

75%!

We seem to have forgotten that hard-won lesson (or, like the students at Ferris Bueller’s high school, never really learned it in the first place).

Maybe that’s unsurprising because progress in finance is cyclical, as Jim Grant says, not cumulative — which means we’re condemned to forever relearning many painful financial lessons.

Still, I never thought the devastating effects of punitive tariffs would be one of the mistakes we’d insist on remaking.

Until this week, the markets didn’t seem to think so either.

Let’s check the charts.

Uncertain estimates:

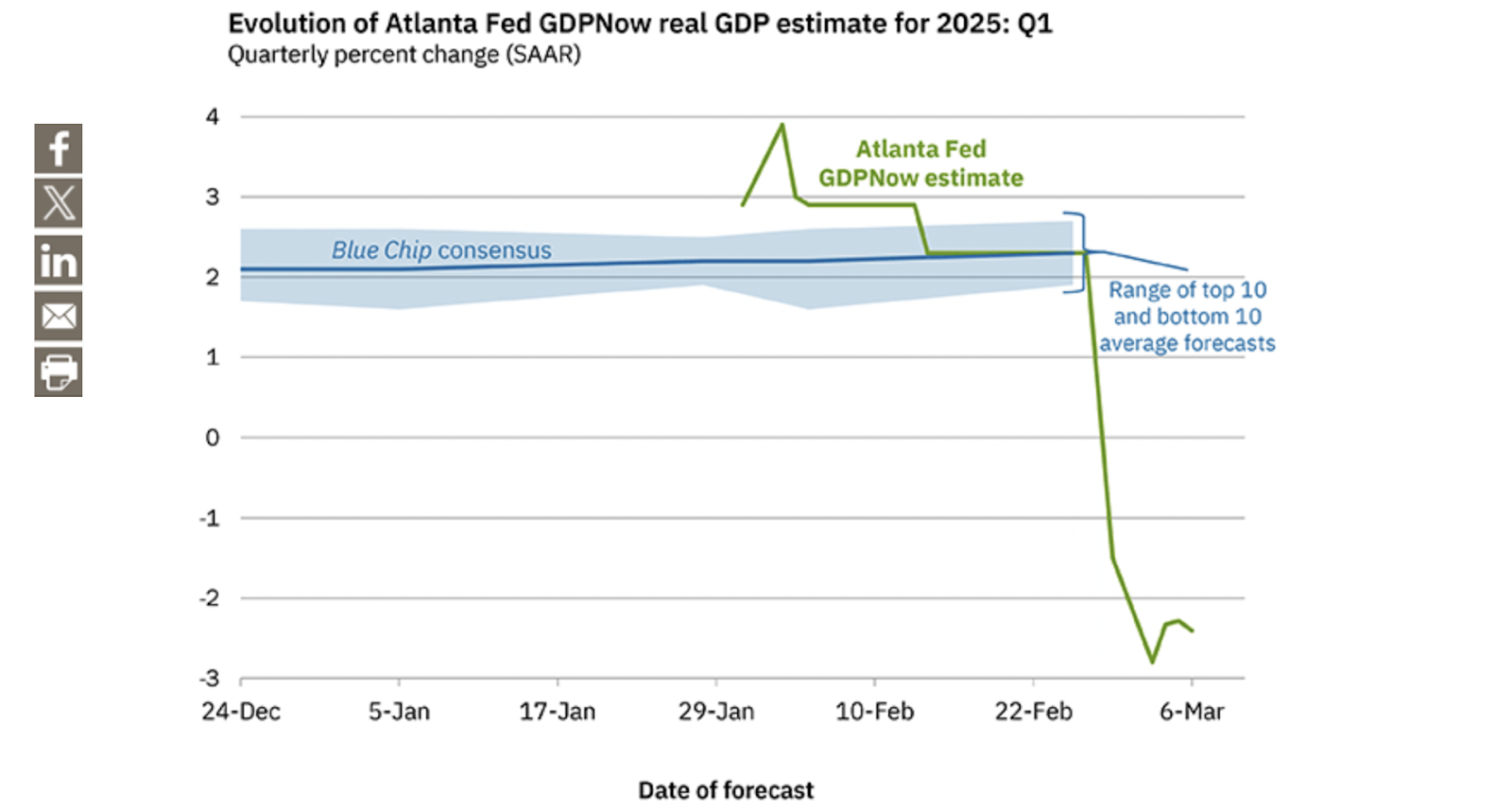

The Atlanta Fed’s GDPNow estimate for Q1 GDP growth has fallen to -2.4%. The final number is unlikely to be that bad, but maybe bad enough for the president to think he might be mistaken?

Quantifying the uncertainty:

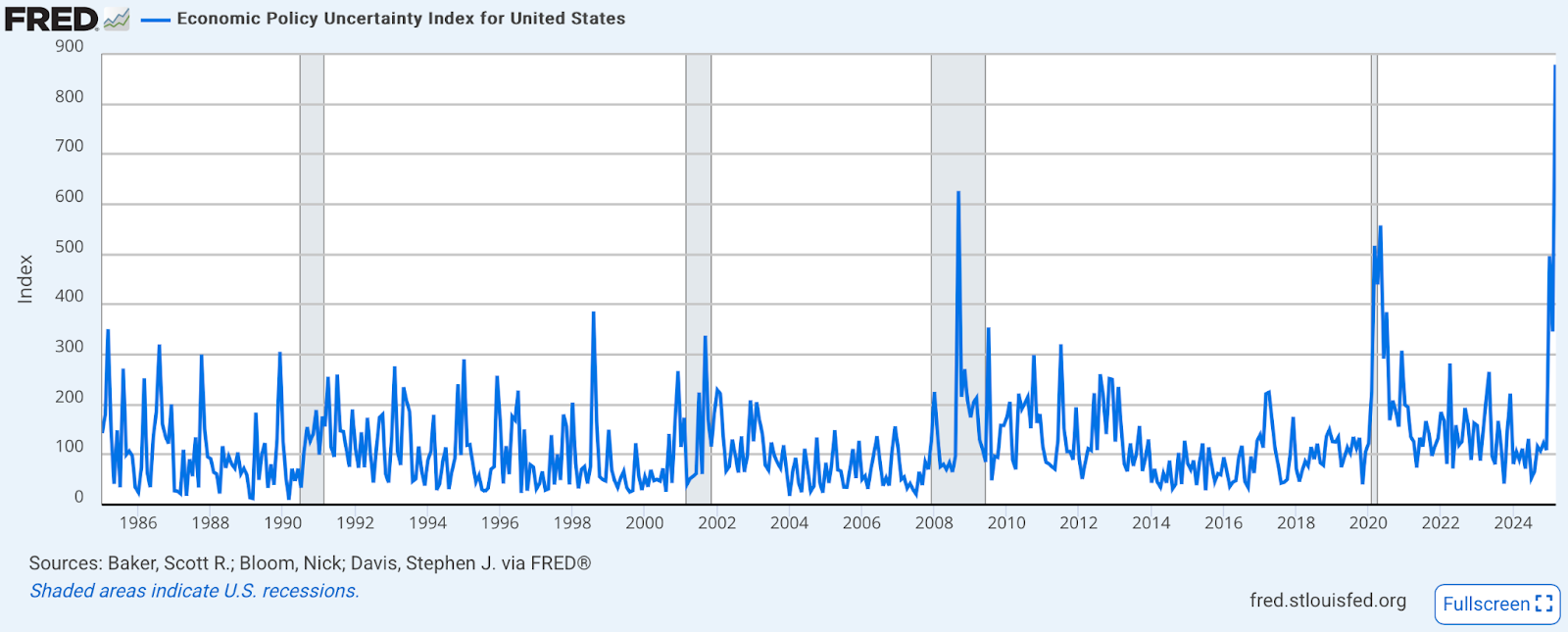

The NBER’s index of economic policy uncertainty is at an all-time high. The data only goes back to 1985, though, so we’ll never know just how uncertain Smoot and Hawley made people feel.

Quantifying uncertainty 2:

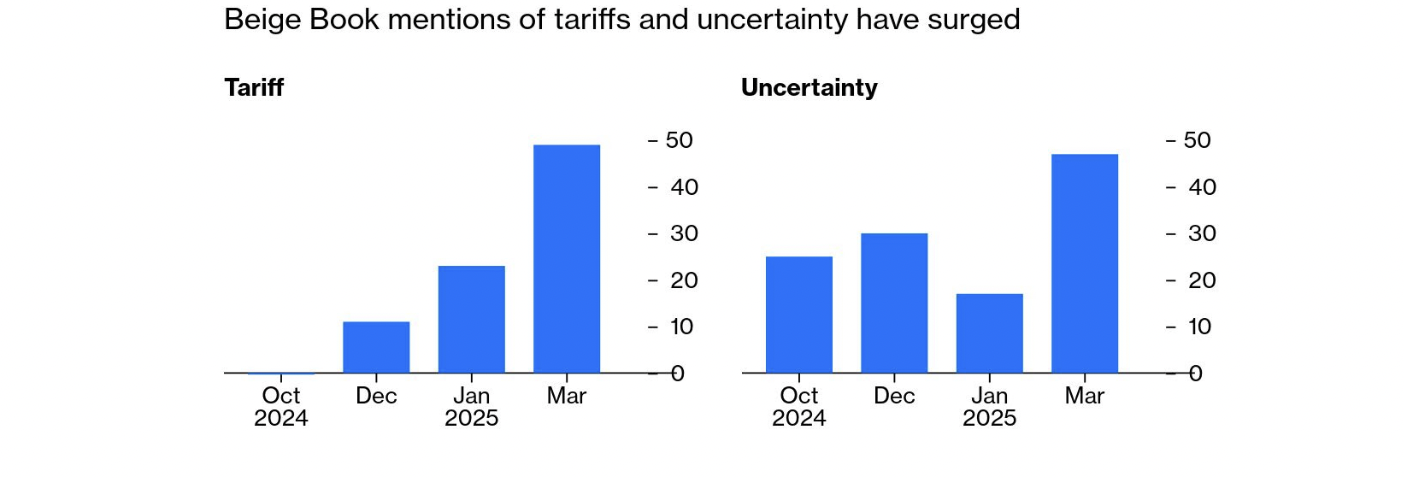

Word count data from the Fed’s beige book survey suggests that respondents are finally starting to take the threat of tariffs seriously. Jon Authers takes this as “evidence that tariffs are causing worry, and may already be changing executives’ behavior.”

Tariff prepping:

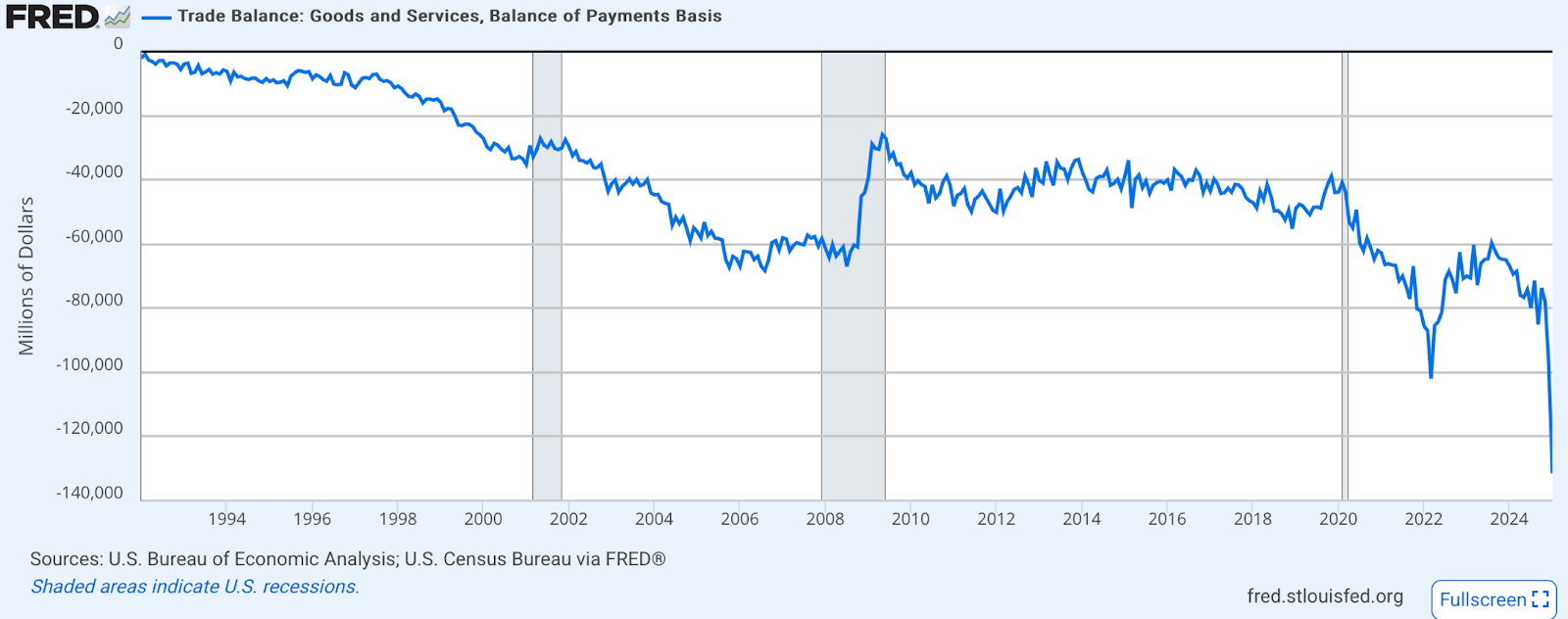

The US trade deficit is ballooning as US importers stock up on goods faster than a doomsday cult stocks its bunker.

Tariffs mean higher prices:

Goldman Sachs estimates that tariffs will add as much as 1.5 percentage points to US prices in 2025. More specifically, Sanford Bernstein estimates that tariffs will raise the average cost of a US car by $2,700.

Tariffs mean lower growth:

Goldman Sachs estimates that tariffs could reduce US GDP growth by as much as 1.4 percentage points.

Pre-tariff inflation:

Thanks mostly to falling oil prices, the Truflation measure of US inflation is down to just 1.38%.

Not that bad?

Despite all the uncertainty, the Bloomberg consensus of economists still only sees about a 25% chance of recession. But I’m guessing it’ll be higher after economists recover from this week’s roller coaster of news.

Dollar down:

Tariffs should generally make the US dollar stronger (because it reduces demand for imports), but the dollar has been getting weaker. This might be good news (maybe tariffs ultimately won’t be that high) or bad news (maybe other countries will set tariffs even higher).

The odds of good news:

Polymarket betting implies there’s a 60% chance that President Trump will remove tariffs on Mexican imports before May (and a 50% chance he’ll remove Canadian tariffs).

If so, it’ll probably be because crashing markets convinced the president that he might be mistaken.

Have a great weekend, free trading readers.

Brought to you by:

Good reasons NOT to stake your SOL: Wanting full custody of your crypto (& sole access to your wallet). Not having enough time in the day to figure out which validator has the best rewards rates (or enough bandwidth to constantly chase higher APYs).

All the more reason to try Marinade Native.

Non-custodial Solana staking, directly from your wallet, automatically adjusted to earn the most competitive staking rewards rates. No smart contracts, no liquid staking tokens, and no extra work.

The US Is Risking Stagflation

Upcoming DAS speaker Mohamed El-Erian discusses the February jobs report, tariffs and imports frontrunning and the growing risk of stagflation. Get his thoughts on the outlook for Japan, China, Bitcoin, digital assets and more.

Listen to Forward Guidance on Spotify, Apple Podcasts or YouTube.

Investors, policymakers, and industry leaders — make the calls that shape the future of digital assets. 3 weeks out, the room is filling up.

Mohamed El-Erian (Allianz) on how institutional capital is navigating uncertainty.

Nathan McCauley (Anchorage Digital) on the state of crypto banking and custody.

Jessica Peck (US Department of Justice) on where enforcement is headed next.

Rep. Tom Emmer (R-MN) on the regulatory fights that will define the industry.

📅 March 18-20 | NYC

We break down the highlights from our interview with Mohamed El-Erian in today’s Forward Guidance newsletter.

@elerianm@fejau_inc— Forward Guidance (@ForwardGuidance)

9:15 PM • Mar 7, 2025

50,000 people on our livestream right now, wild

— Yano 🟪 (@JasonYanowitz)

9:04 PM • Mar 7, 2025