- The Breakdown

- Posts

- 🟪 Friday Surprising Charts

🟪 Friday Surprising Charts

Is Buffett correct about surprises?

This issue is brought to you by:

“It is essential to remember that virtually all surprises are unpleasant.”

- Warren Buffett

Friday Surprising Charts

Is Buffett correct about surprises?

Markets seem to think so: It's why stocks go up on an escalator (slowly) and down on an elevator (quickly), why puts cost so much more than calls and why stocks tend to fall more after bad earnings reports than they go up after good ones.

That might be more market psychology than statistical fact, however, because good surprises happen too.

The global economy proved surprisingly resilient during the pandemic, for example. Inflation was surprisingly transitory thereafter. And the Fed has been surprisingly competent the entire time.

The effect of those welcome surprises was in evidence this week: Yesterday’s release of Q4 GDP showed the US economy continues to grow faster than expected, while this morning’s December PCE report showed inflation continues to fall faster than expected — a nice way to close the books on a surprisingly good 2023.

It’s not the only pleasant surprise from 2023.

After spending much of the year worried that ChatGPT was a first step toward our inevitable subjugation to robot overlords, it now seems far more likely that the robots will be perfectly content to make us our morning coffee, as Figure AI demonstrated this week.

Friendly robots are a great upside surprise and part of the reason why Microsoft became a $3 trillion company this week.

2024 has begun with another great one: China's non-response to Taiwan's election.

Semiconductor stocks shot higher this week as the odds of a conflict that would shut down Taiwan-based TSMC (and therefore the entire world economy) seemed significantly lower than they did last week.

That propelled US equities to new all-time highs led by Nvidia, up another 27% already this year.

Economist Ed Yardeni thinks there could be more upside surprises to come: “The S&P 500 may be starting a tech-led melt-up similar to what happened during the second half of the 1990s,” he wrote in a note this week.

“We are wondering whether a bout of irrational exuberance might push the multiple higher, inflating a speculative bubble in the stock market as occurred during the late 1990s.”

I hope he’s right, because markets were never more fun than they were in the late 1990s.

But even if he’s not, it’s a reminder that the tail risks in finance are not all to the downside — markets can surprise to the upside, too.

And because we’re always so focused on the downside, the upside might be easier to realize than you’d think — the biggest surprise of 2024 might simply be that there are no unpleasant surprises.

Is it time to look out above?

Let’s check the charts.

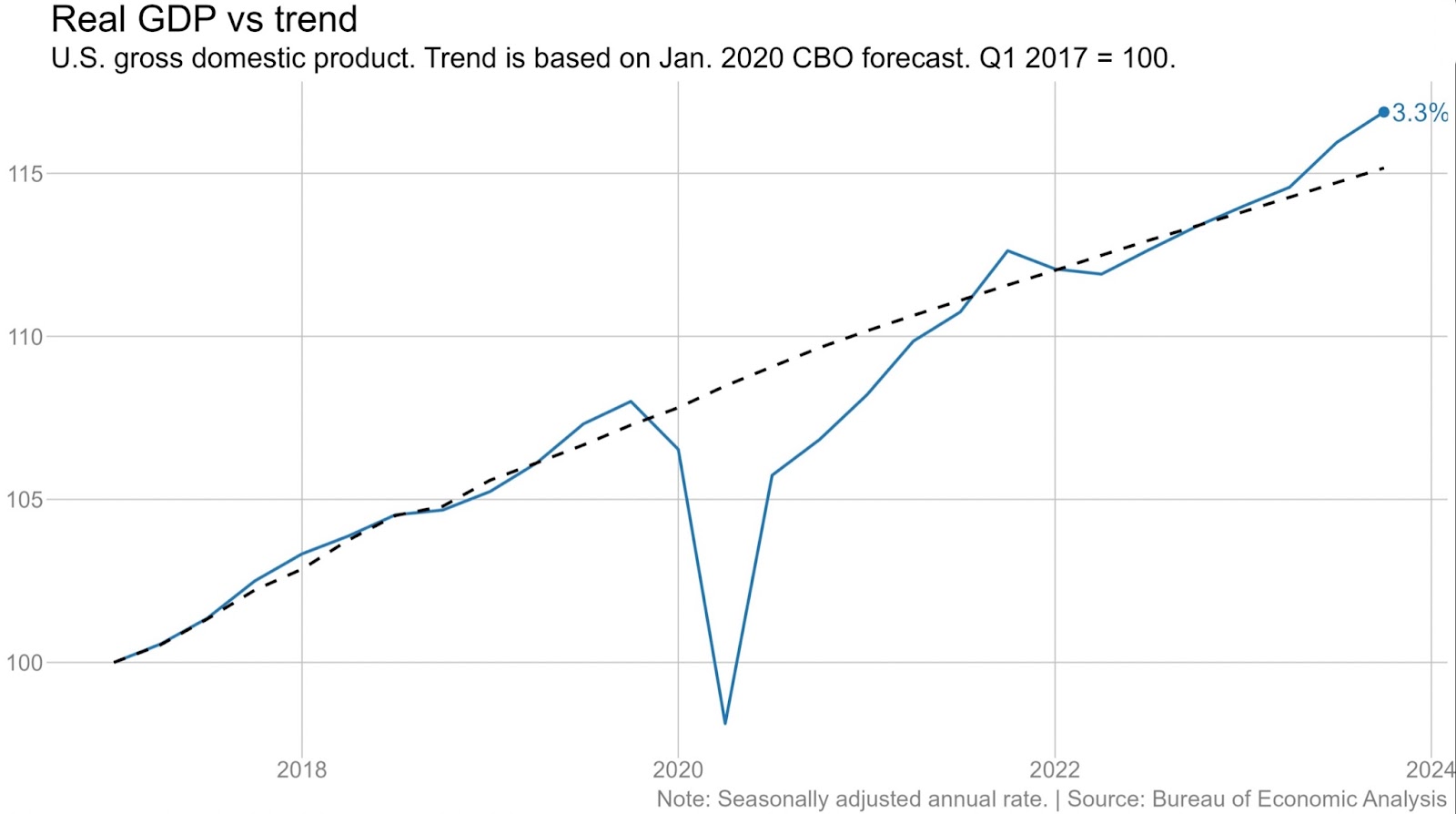

2023 was surprisingly good:

The US economy grew 3.3% in Q4 — accelerating just when people had expected it to be sputtering. Ben Casselman of the New York Times notes that US GDP is now above where the CBO expected it to be before the pandemic (and that’s adjusted for inflation, too, per the above chart).

Try again next year:

The US economy grew 2.5% for the full year — far better than the near 0% growth Wall Street economists had expected at the start of the year

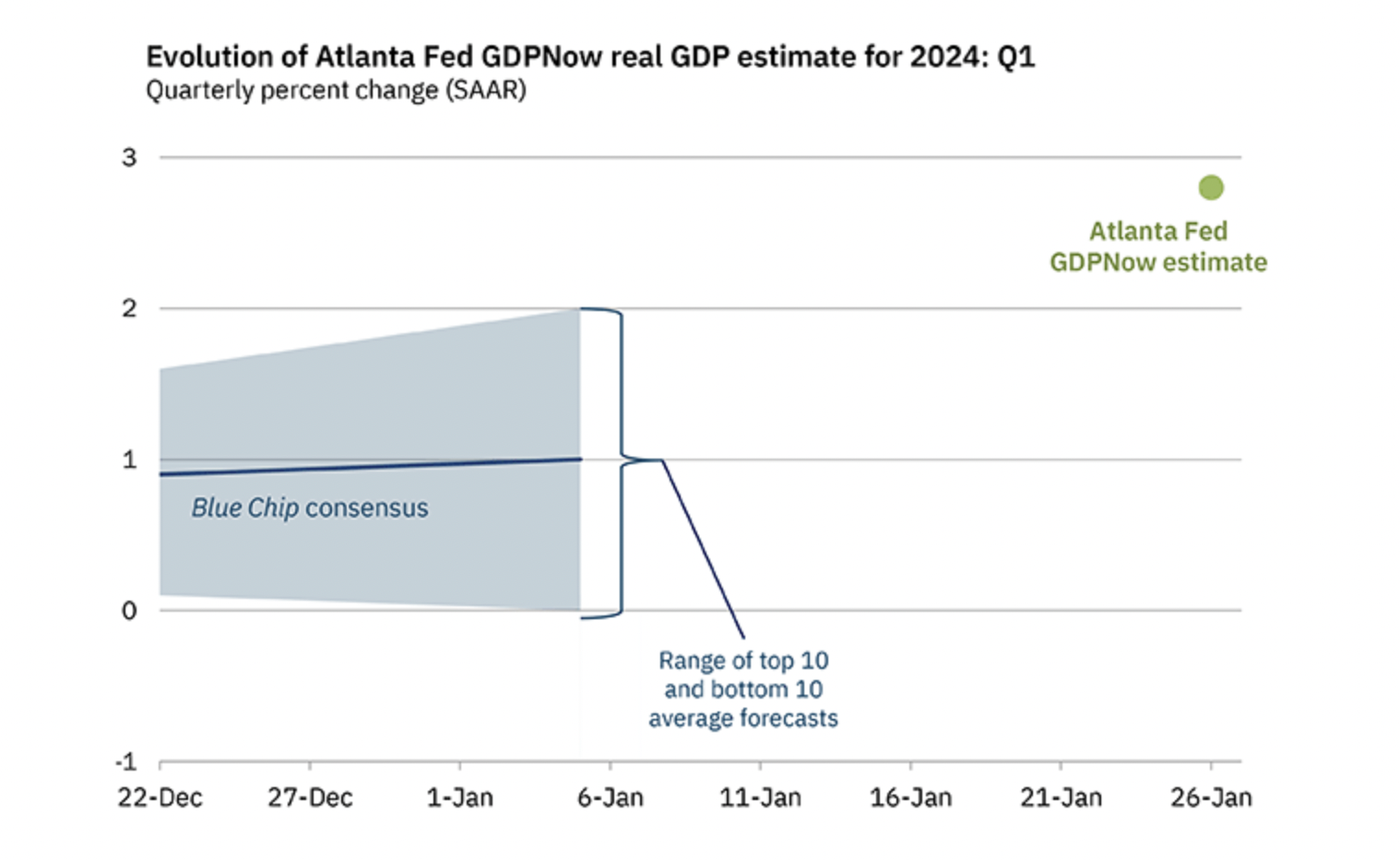

More of the same?

Economists may still be too pessimistic. The blue line at 1% is Wall Street’s consensus for Q1 GDP. The green dot at 3% is the GDPNow estimate. GDPNow has been winning.

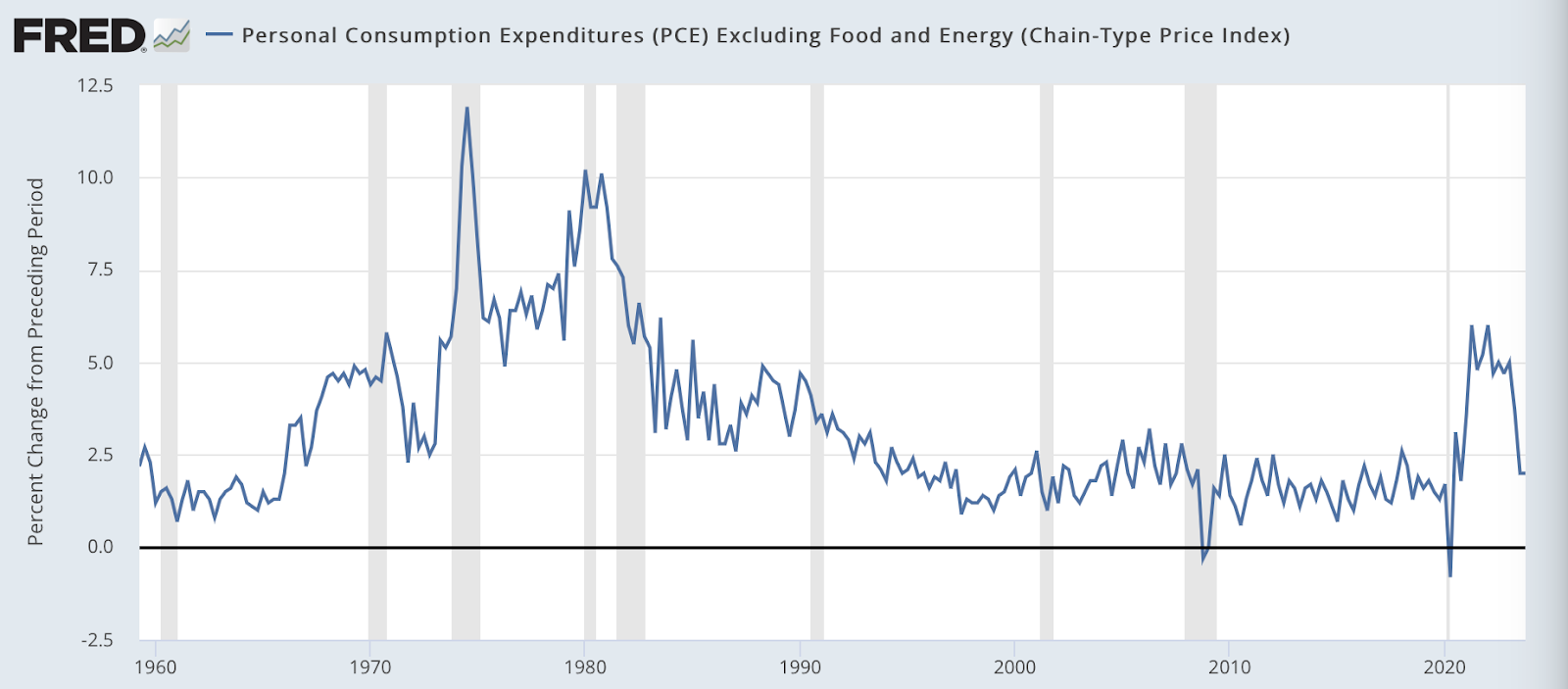

The other big surprise:

2023 ended with two consecutive quarters of core PCE inflation running at an annualized rate of 2.0%. That’s exactly the Fed’s target, which no one thought we could hit without inducing recession. We hit it, and recession is nowhere in sight.

Surprised?

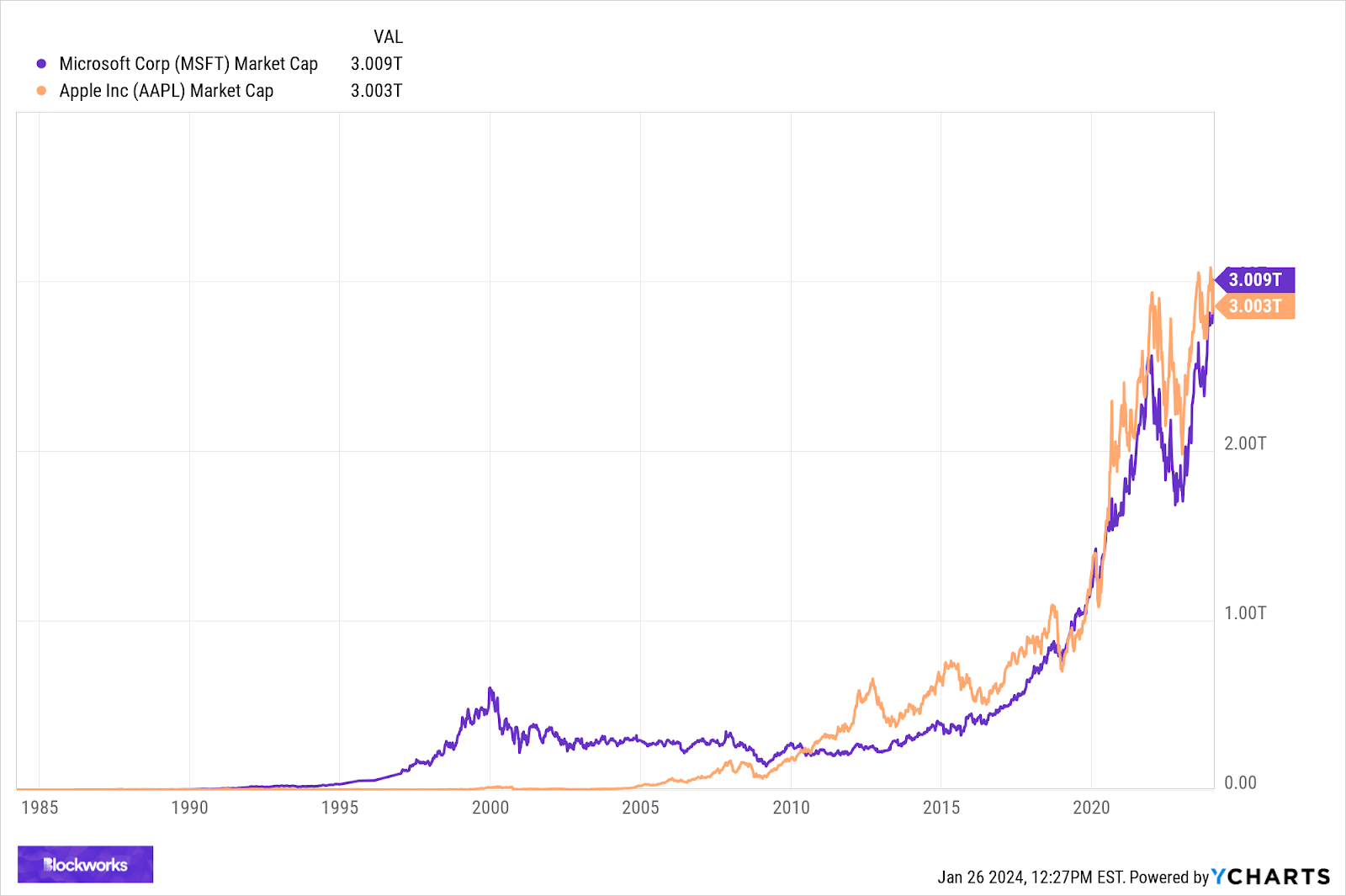

AI mania has propelled Microsoft into the exclusive club of companies worth $3 trillion. Only other member: Apple.

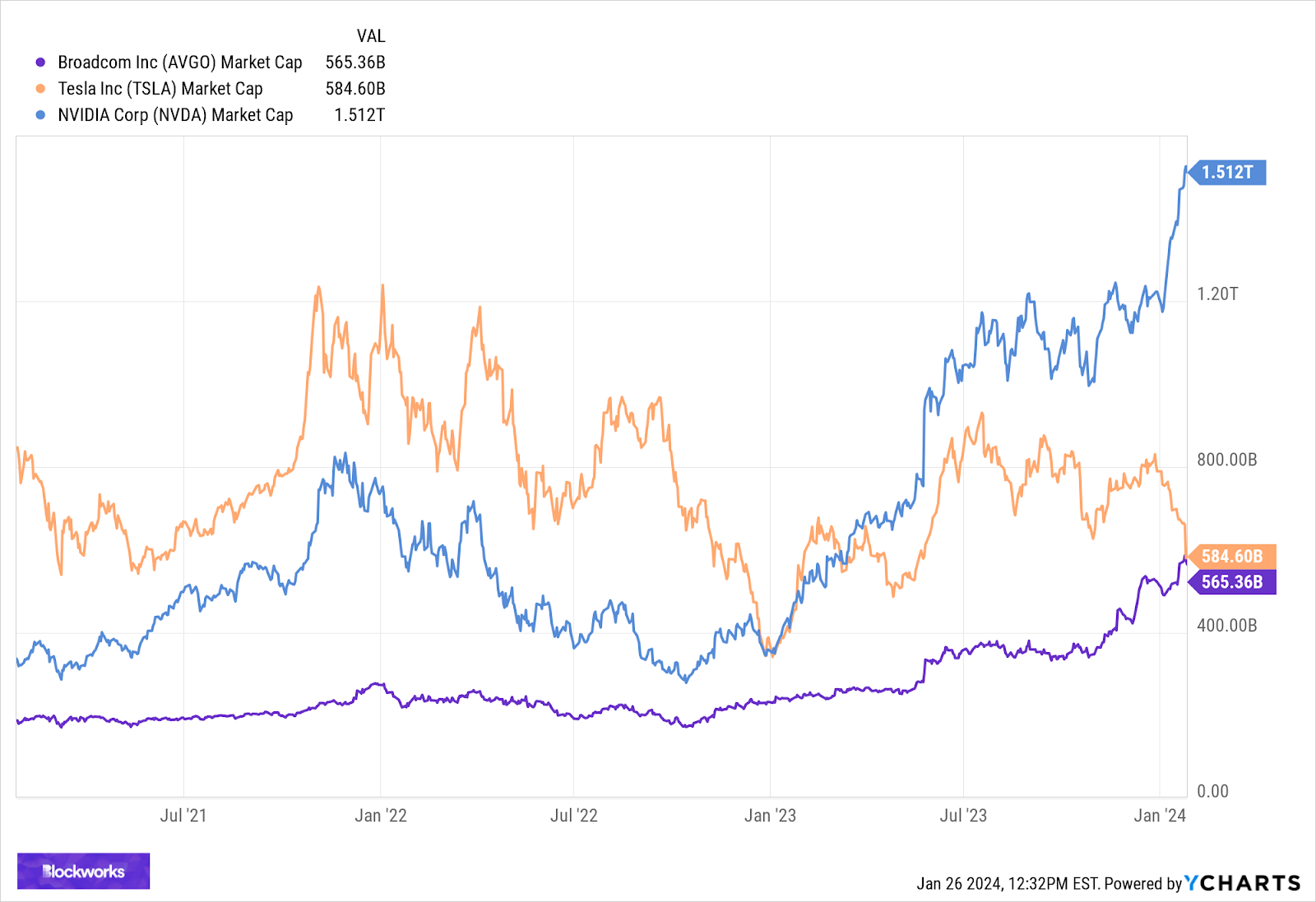

Semi surprised:

Nvidia, which nearly everyone thought was far too expensive last year, is already up a further 27% this year. Another semis giant, Broadcom, overtook Tesla by market cap this week — so the Magnificent 7 will have to either swap out TSLA for BRCM, or rebrand itself as the Magnificent 8.

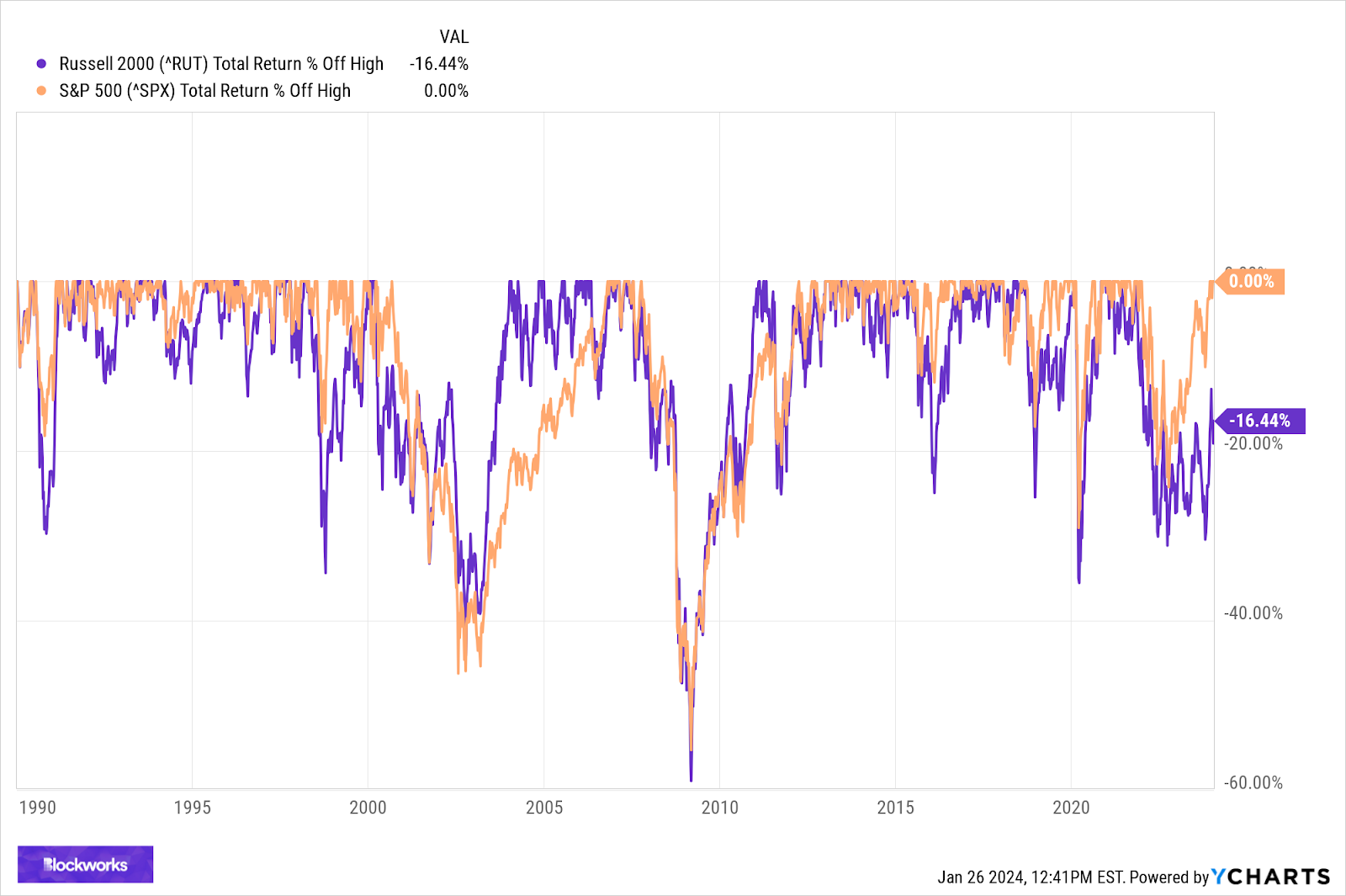

The not-so-magnificent 2000:

The S&P 500 (orange) is at an all-time high, but the Russell 2000 remains not far removed from bear-market territory. The only other time small caps lagged this far behind as large caps made new highs was 1998.

Surprisingly solid (for some):

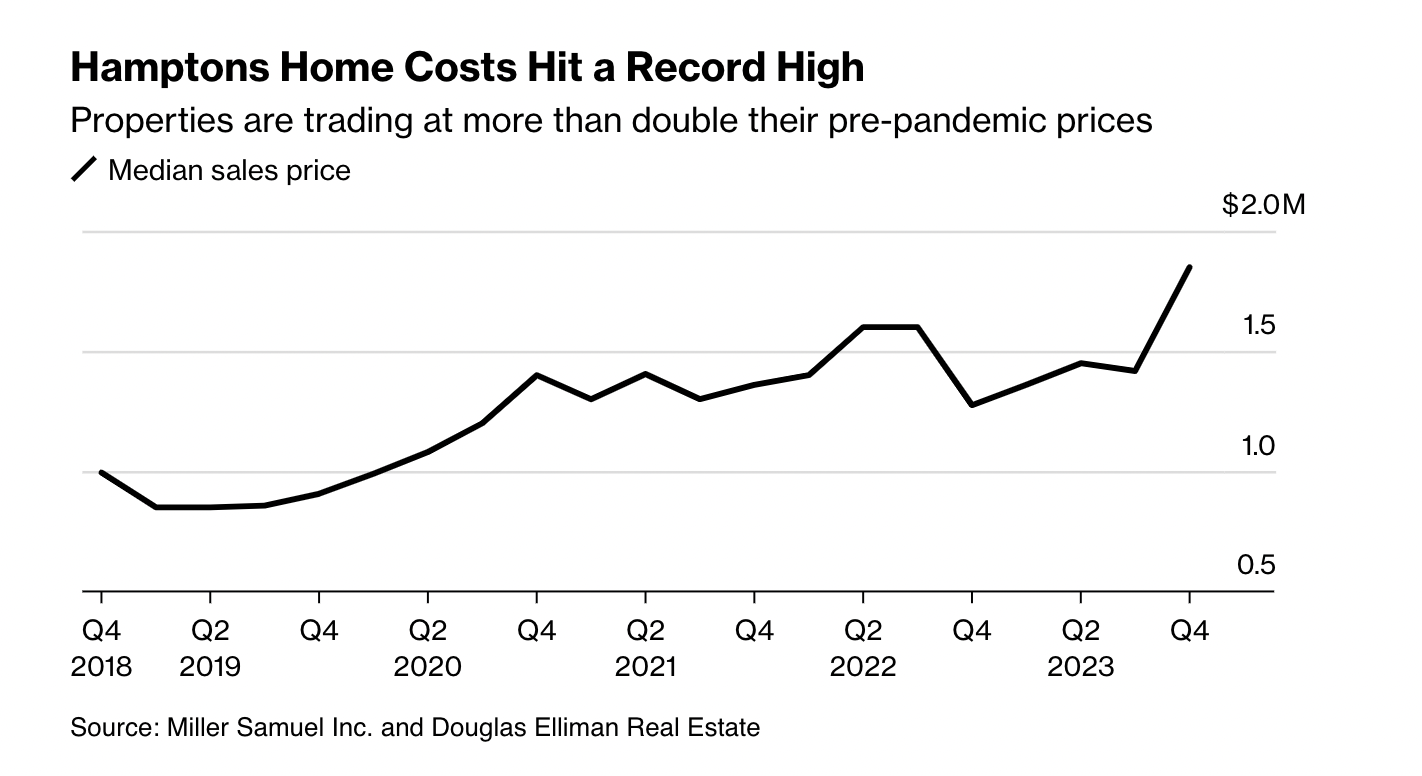

The much-feared housing bust may have come and gone already: New home sales were reported up 8% YoY this morning. Prices remain surprisingly buoyant, mostly because there’s still a shortage of existing houses (sales -4% YoY) — especially in places like the Hamptons, where an average home will now set you back $1.85 million. Yikes.

UP: GDP, stocks, housing.

DOWN: Inflation, Taiwan risk, AI risk.

What else could go right in 2024?

We’ll just have to let ourselves be pleasantly surprised.

Have a great weekend, right-tailed readers.

This issue is brought to you by:

Arbitrum is the leading Ethereum layer-2 scaling solution, home to over 600+ applications.

Arbitrum allows you to interact with Ethereum the way it was meant to be — with lower fees and faster transactions. Whether you're exploring the leading DeFi ecosystem, the strong infrastructure options, a flourishing NFT and creator ecosystem or a rapidly growing gaming hub, the Arbitrum ecosystem has a solution for you.

Top Stories

Bitcoin halving expected to hit on 4/20 — Read

Roughly ‘60% chance’ of spot ETH ETF approval in May: Seyffart — Read

Bitcoin ETFs see net outflows for 4 straight days — Read

TRON 2023: Key developments and collaborative milestones [Sponsored] — Read

Mercado Bitcoin starts 2024 with listing of TRON network’s native token: TRX [Sponsored] — Read

We're Watching

In this week's roundup Mike and Myles dive deep into the dichotomy emerging between Ethereum the protocol and Ethereum the Asset. As Ethereum pushes activity to rollups and prioritizes exporting ETH's value, tough questions arise around stake rates, liquid staking derivatives, and monetary policy.

We’re Hosting

Bitcoin’s Next Frontier: Institutional Demand in the World of Options and Futures Trading

This webinar will explore the evolving landscape of Bitcoin with a focus on institutional demand and products from traditional finance. Discussion will include an analysis of market dynamics, the intricacies of options pricing, the significance of a spot ETF for Bitcoin and its implications on the broader cryptocurrency market.

Daily Insights

Here's what the premiums and discounts have looked like for the #Bitcoin ETFs intraday through 10 days. Compression all around.

— James Seyffart (@JSeyff)

4:39 PM • Jan 26, 2024

The market is expecting the first rate cut in May

— Benjamin Cowen (@intocryptoverse)

8:58 PM • Jan 26, 2024

The ECB is about to make its second policy mistake in a row.

Slow to respond to inflation, slow to respond to disinflation.

The European economy doesn’t work with 3-4% rates.

The longer they wait, the more they’ll be forced to cut later.

— Alf (@MacroAlf)

8:13 AM • Jan 26, 2024