- The Breakdown

- Posts

- 🟪 Predicting probabilities

🟪 Predicting probabilities

Are dollar prices in prediction markets the same as percentage probabilities?

Byron Gilliam

October 22, 2024

Brought to you by:

“It is difficult to predict, especially the future.”

— Danish proverb

Predicting probabilities

Are the dollar prices in prediction markets the same as percentage probabilities?

Polymarket says they are: “Prices (odds) on Polymarket represent the current probability of an event occurring,” according to its documentation.

Media coverage of the US election also treats them as such and this has been spreading despair among Democrats as the price of a Kamala Harris “Yes” contract has fallen from 52 cents as recently as a month ago to just 33.9 cents now.

The Polymarket website presents these dollar prices as percentages:

Should we therefore take the top chart at face value and assume Kamala’s chances of winning the presidency have sunk to just 33.9%?

Not everyone thinks so: “Many prognosticators have interpreted this as [a] drop in Harris’ odds of winning the presidential election. This is false, and also very stupid,” according to the anonymous author of the Quantian Newsletter.

Kamala voters rejoice!

Prices in prediction markets should not be either presented or understood as probabilities, Quantian writes, mostly because the binary payout structure of prediction markets creates a “convexity” that amplifies the impact of high-conviction — or highly motivated — bettors (particularly for longer-shot bets such as Trump winning the popular vote).

The details get a little technical, but Democrats should take heart from the TLDR that the sinking price of the Kamala Harris “Yes” contract may be as much about how easy it is to move prices on central-limit order books like the one at Polymarket as it is about Kamala’s recent polling.

Democrats might not want to rejoice too much though, because calling it “very stupid” to interpret prices as probabilities may be overstating the case against prediction markets — academic studies have long found prediction markets to be, well, predictive.

A 2006 paper co-authored by economists Justin Wolfers and Eric Zitzewitz, for example, determined that “prediction market prices appear to be quite accurate predictors of probabilities.”

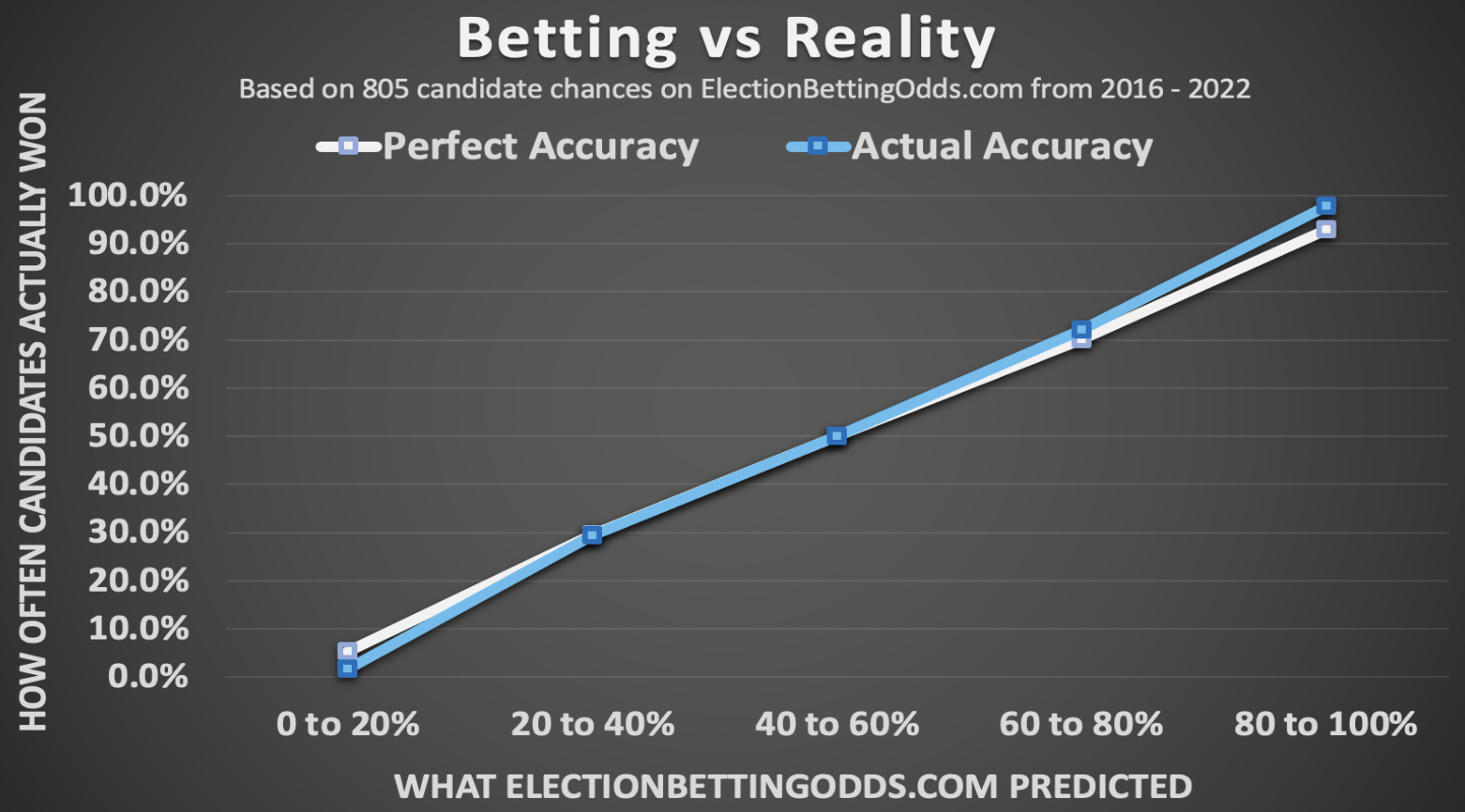

Similarly, a post-mortem of 807 political races followed by ElectionBettingOdds.com found that prediction market prices on those elections closely matched the after-the-fact probabilities implied by their outcomes.

This is especially true in election bets near the middle of the probability spectrum, where Quantian’s “convexity” (aka “favorite-longshot bias”) is less of an issue.

These are averages, of course, and there is good reason to believe the election on Nov. 5 will not be average: The Polymarket odds are almost certainly being manipulated in Trump’s favor by a single, highly motivated bettor, as detailed in the Wall Street Journal last week.

It’s possible that the highly motivated bettor at the top of Polymarket’s betting ranks, Fredi9999, is in it to make money, but this seems unlikely — their trading patterns seem designed to have the maximum possible impact on price, which is of course the opposite of what anyone motivated by money would be trying to do.

Fredi9999’s motivation is, therefore, presumably to distort the prediction market in Trump’s favor — to what degree they’ve succeeded is open to interpretation, but the 5-8% impact estimated here seems like a good guess.

There is nothing new in this.

In 2008, an “institutional investor” was found to have placed hundreds of thousands of dollars of bets on the prediction market intrade to give people the impression that John McCain was doing better than he really was — and in 2012 someone lost at least $4 million attempting to do the same for Mitt Romney.

In the latter case, “this trader's activity was simply a form of support to the campaign,” according to the economist Rajiv Sethi.

The same appears to be happening in 2024, except bigger (thanks to Polymarket) and more transparently (thanks to crypto).

The betting is so big and so transparent this time that even the most staunch believers in prediction markets would likely concede that Polymarket odds should not be accepted exactly as probabilities.

This should not come as a surprise: Even Wolfers and Zitzewitz, for example, were conspicuously circumspect in their defense of prediction markets, writing that they provide “useful estimates of average beliefs about the probability an event occurs.”

That careful wording seems particularly apt in the case of election markets because betting on an election is fundamentally different from betting on, say, a sporting event.

If betting markets imply that the Yankees have a 60% chance of beating the Dodgers on Friday, it’s a good indication that if the two teams played 100 games in a row, the Yankees would probably win about 60 of them and the Dodgers about 40.

But if the US election was run 100 times over, it’s probably not the case that Trump would win 60 times and Harris 40.

Instead, there is most likely one true outcome and the probability of that outcome is simply a reflection of our inability to discern it.

In other words, prediction markets aren’t predicting the election outcome so much as they are predicting how accurate the polls are in predicting it.

More precisely, prediction market prices reflect the “average beliefs” created by those polls.

“Prediction market prices aggregate beliefs very well,” according to Wolfers and Zitzewitz, but they can also be undermined when betting is “motivated by an unusual degree of risk-acceptance.”

Fredi9999 is accepting a lot of risk!

Polymarket prices aren’t exactly probabilities, then, even if history shows that they are a near-substitute.

So, how despairing/elated should you be about the big move in prediction markets?

It’s impossible to say, but probably 5-8% percentage points less than Polymarket would have you believe.

Brought to you by:

MANTRA is a purpose-built RWA layer-1 blockchain capable of adherence and enforcement of real world regulatory requirements. As a permissionless chain, MANTRA empowers developers and institutions to seamlessly participate in the evolving RWA tokenization space by offering advanced tech modules, compliance mechanisms, and cross-chain interoperability.

Key Features:

Built using Cosmos SDK, IBC compatible, with CosmWasm supported

Secured via a sovereign PoS validator set

Scalable up to 10k TPS

Built-in Modules, SDKs and APIs to create, trade and manage regulatory compliant RWAs

Improved User Experience to onboard non-native users and institutions to Web3

Delta: Breaking Tradeoffs in Blockchain Architectures

Delta’s Ole Spjeldnæs and Myles O’Neil join the episode to discuss the vision behind Delta’s design, state model and zk settlement. Tune in for an outlook of Delta’s leaderless consensus functions and token value accrual.

Listen to Bell Curve on Spotify, Apple Podcasts or YouTube.

A lot of the Stripe / Bridge talk seems to be missing the point - this isn't just about Stripe's crypto abilities. This is about broadening Stripe's entire business - from one that ultimately depends on the merchant - to one that can be its own global payment network.

On-chain… x.com/i/web/status/1…

— Rob Hadick >|< (@HadickM)

5:07 PM • Oct 21, 2024

Tokens are protocol equity.

They should entitle you to direct the protocol's trajectory.

They should entitle you to permit/restrict how builders build with the protocol.

They should enable permissionless consumption and value-capture.

Anyone can buy tokens.

— arvind (@p0Gnosis)

4:59 PM • Oct 21, 2024

Seeking Alpha in Liquid Markets

Featuring:

@bgilliam1982

@joemccann

@TusharJain_x.com/i/web/status/1…— Permissionless (@Permissionless)

7:10 PM • Oct 22, 2024