- The Breakdown

- Posts

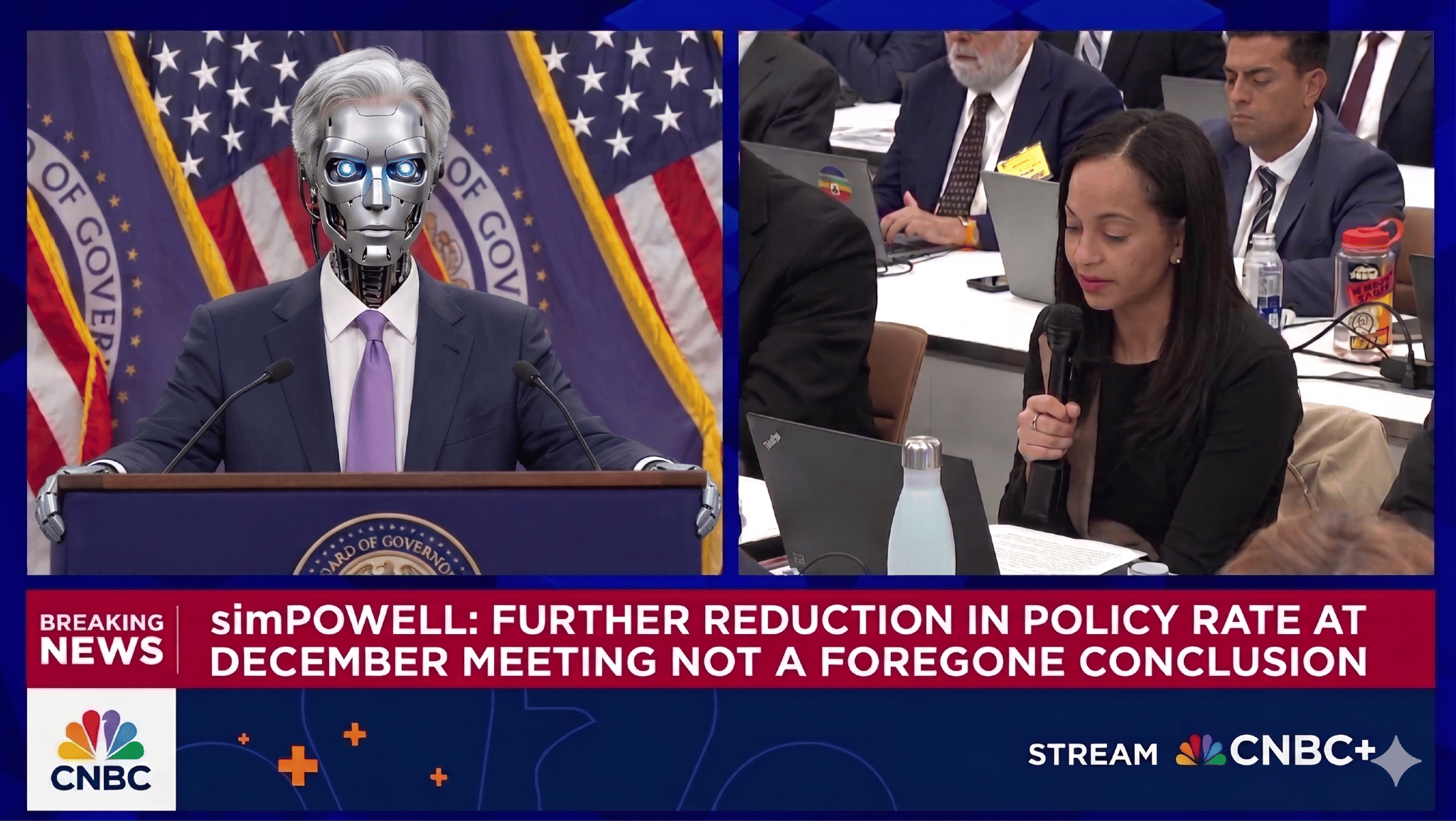

- 🟪 SimFOMC

SimFOMC

If LLMs are prediction machines, our replaceability will be a function of our predictability.

An LLM that can reliably anticipate what you’ll write, say, and do in any given situation will be fully capable of doing your job.

By that measure, economists Sophia Kazinnik and Tara Sinclair have developed an AI that’s ready to replace the Fed: it predicts how members of the FOMC will vote on rate decisions with uncanny accuracy.

The economists use the model as a kind of flight simulator for monetary policy — a way to test how all manner of what-if scenarios would affect FOMC policy.

They do this by recreating the FOMC at the individual level: each real-life banker is represented by a simulated agent — simPowell, simWaller, simMiran.

Each simulated agent is powered by its own LLM, trained on their banker’s background, academic papers, speeches, CNBC appearances, and more.

(Future iterations might even include their hobbies, Sinclair told David Beckworth.)

The simulated bankers “reason in natural language” and “engage in committee debate,” just like the real ones.

To predict a rate decision, the model puts them through every aspect of the rate-setting process, both formal and informal.

A “water-cooler option,” for example, accounts for the spontaneous chats bankers might have before going into a meeting. “We’ve set it up so that it follows exactly the way that the minutes say that an FOMC meeting is structured,” Sinclair explains.

Monetary policy is shaped as much by personalities as it is by data, so the water-cooler chats are important — they help the model capture the qualitative effects of “deliberation, persuasion, and strategic interaction” on bankers’ decision-making.

This has many advantages.

In addition to making the model more accurate, it lets researchers explore counterfactuals. Greenspan always spoke first at FOMC meetings, for example, and Bernanke last. Would policy have been different if the order was reversed? The model could tell you.

What if meetings were more frequent? Or less? Or never at all! Macroeconomists can use the model to do the kind of experimental research previously reserved for their colleagues studying microeconomics.

Sinclair thinks the real FOMC should use the model, too: “This framework allows policymakers to rehearse decisions, explore vulnerabilities, and evaluate reforms before they are tested in crisis,” her paper concludes.

But I have a better idea: let the model do all that!

This would have even more advantages.

Instead of simulating just the current FOMC, we could create simVolcker, simGreenspan, and simBernanke, too: interest rates would be entrusted to an all-star team of history’s greatest central bankers.

The dark art of monetary policy would become fully transparent: every water-cooler chat could be documented online, as it happens.

The FOMC could always be in session: instead of setting policy once every two months, it could debate every new data release and adjust policy on the fly.

Finally, presidents could appoint simulated bankers to the synthetic FOMC knowing exactly what they’d get: simVolcker if they worried about inflation, simGreenspan if they worried about growth.

Now, in the age of AI, all this can be done with computers.

Milton Friedman would say it’s past time we do it.

He was in favor of replacing the Fed with a computer since at least the 1990s — a time when computers couldn’t predict the next word of a single sentence, let alone the votes of 12 bankers.

Perhaps for that reason, Friedman would not have asked his monetary computer to do too much: “only print out a specified number of paper dollars — same number — month after month, week after week, year after year.”

With today’s computers, though?

Safe to say, simFriedman could do far better than that.