- The Breakdown

- Posts

- 🟪 Friday charts

Friday charts: The debt only rises

I’m old enough to remember when the Fed worried the US government wasn’t borrowing enough money.

In 1998, the US collected $70 billion more in taxes than it paid out in expenses, creating its first budget surplus in nearly 30 years.

By 2001, the US Treasury was so flush with cash it chose to retire government debt by buying Treasury bonds from the market (not with printed money like when the Fed does it, but with taxpayer money).

As welcomed as that was, it threatened to become too much of a good thing.

Fed Chair Alan Greenspan warned at the time that “the elimination of Treasury debt does remove something of economic value,” and that it could have “some potential adverse consequences.”

Greenspan even considered the possibility of the government borrowing money it didn’t need: “One might argue that it would be best to continue to borrow at least limited amounts from time to time in order to keep the [Treasury] market operating, so that it will be available when it is needed again.”

(If only he knew how very needed it would be.)

Some of this was luck — tax receipts surprised to the upside for a few years, thanks to favorable demographics and a booming stock market.

Strangely, though, much of the credit goes to politicians — on both sides of the aisle: George Bush signed the Budget Enforcement Act in 1990 and Bill Clinton pushed through a deficit-reduction package in 1993.

Even more telling: Ross Perot, campaigning almost exclusively on the issue of deficit reduction, won 19% of the popular vote in the 1992 presidential election.

How times have changed.

Now, it’s hard to imagine either party prioritizing balanced budgets, let alone both.

Instead, the best policy ideas on offer are wild swings like starting a strategic reserve of bitcoin, buying 10% of Intel and shaking down Nvidia for 15% of its sales to China.

The US government has so given up on balancing its budget that the president has been campaigning to make it the Federal Reserve’s problem.

That, at least, is the subtext of this week’s firing of Governor Lisa Cook — the president wants to replace her with someone who will vote for lower interest rates and make the national debt easier to finance.

In the president’s telling, the Fed should cut rates because “our Country would be saving Trillions of Dollars in Interest Cost.”

The Fed would have to keep interest rates artificially low for years before the savings amounted to “Trillions,” but it could be done — presumably at the cost of unleashing ruinous inflation.

As recently as the last FOMC meeting, Chair Powell reassured markets that “there should be no doubt that we’ll do what we have to do to keep inflation under control.”

The president’s campaign against Fed independence has since made people start to doubt, as evidenced by a steeping yield curve and rising inflation swaps.

Markets may simply be recognizing that asking the Fed to fight both inflation and finance the deficit is like asking it to drive with one foot on the gas and the other on the brake.

With annual interest payments at $1 trillion, raising rates — the Fed’s only real tool to fight inflation — has become counterproductive to deficit reduction: The first order effect of a rate rise is higher deficits because of higher interest costs.

So, unless we want to cross our fingers and pray for an AI productivity boom, it’s ultimately up to Congress to do something about the deficit — some combination of higher taxes and lower spending is the only thing for it.

Which means that, ultimately, ultimately, it’s up to voters.

Unfortunately, it’s unimaginable that a third party candidate could get 19% of the popular vote by promising to cut the deficit.

The debt will only keep rising until it no longer is.

Let’s check the charts.

The unbalanced budget, in a picture:

This infographic, via @MikeZaccardi, neatly summarizes the US government’s incoming revenue (on the left) and outgoing expenses (on the right). It’s not easy to see which items on the right Congress would be willing to cut. And the ascent of “net interest” makes it harder for the Fed to fight inflation.

Inflation still needs fighting:

This morning’s PCE data showed that at 2.9%, core inflation remained well above the Fed’s 2% target in July, and the Cleveland Fed’s model (above) suggests it will stay that way in August. And likely beyond: The Wall Street Journal reports that President Trump’s tariffs are only now starting to “trickle down to American shoppers.”

Getting concerned?

Markets have been confident that Chair Powell really will do “whatever it takes” to keep inflation under control. But they may be starting to question if he really can. Two-year inflation swaps (the best indicator of the market’s expectations for inflation) have risen above 3%.

Tell me your party affiliation and I’ll tell you your interest rate outlook:

Republicans are nearly 50 percentage points more likely than Democrats to expect interest rates to fall.

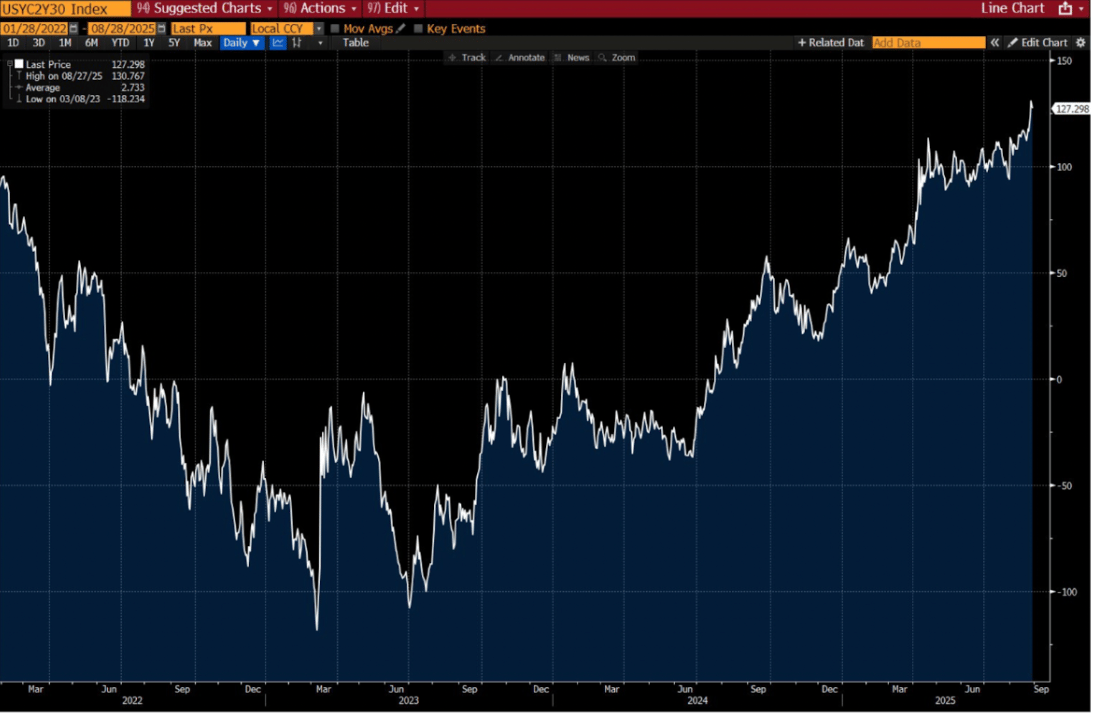

The yield curve:

Another indication that markets are getting concerned about inflation: Lisa Abramowicz notes that the US yield curve is steepening, with the differential between 30-year and 2-year Treasury yields at its widest since 2022.

Rising mortgage costs:

Over 20% of US mortgages now cost homeowners more than 6%. Those most expensive loans (in red) will soon pass the ZIRP-era, sub-3% loans (in blue).

Housing is a buyers’ market:

Data from Redfin shows that home sellers now outnumber buyers by over 500,000.

6%+ feels like a lot to pay for a mortgage.

But if voters don’t make Congress do something about the deficit, you might want the biggest fixed-rate loan you can get.

Have a great weekend, budget-balancing readers.

Brought to you by:

Is your treasury losing value to inflation?

A new report from Liquid Collective and EigenCloud outlines a practical guide for making digital assets like ETH and SOL productive with uncorrelated, protocol-driven staking rewards.

Learn how to integrate institutional-grade staking and restaking to build a future-ready treasury.

|

By Ben Strack |  |

By Casey Wagner |  |

By Donovan Choy |  |

|