- The Breakdown

- Posts

- 🟪 The US was built to borrow

The US was built to borrow

Thomas Sargent’s Nobel Prize lecture is a history lesson that makes America 12 years younger than it thinks it is.

In July, America will celebrate its semiquincentennial, citing the 1776 Declaration of Independence as its date of birth.

But it might better have been considered a Declaration of Intent — an intent that wasn’t fulfilled until the ratification of the Articles of Confederation in 1781 turned the colonies into States.

Sargent wouldn’t start there either, however — because that’s not the country we live in now.

Instead, he’d date the country’s birth to the 1788 ratification of the US Constitution — the governing document that made the country so radically different from what it would have been under the Articles of Confederation that it effectively created a brand-new nation.

The difference is about money.

“Our framers abandoned our first constitution in favor of our second,” Sargent explains, “because they wanted to break the prevailing statistical process for the net-of-interest government surplus and replace it with another one that could service a bigger government debt.”

In other words, the purpose of starting over in 1788 was to create a country that could borrow money: We the People of the United States, in Order to take on more debt…

The previous iteration of the United States, governed by the Articles of Confederation, could not borrow because it had no hope of repaying. The power to tax was reserved by the states.

Investors knew this. When Continental bonds traded for pennies on the dollar during the 1780s, the market was sending a clear message to the federal government: We don’t believe you can pay us back.

That pricing reflected an iron law of credit markets: Debt is only worth the borrower’s ability to generate future repayments.

Sargent won the Nobel in economics in part for showing that this is how investors think about government debt, and how savers think about currency, too.

“The value of government debt,” Sargent explained, “equals the discounted present value of current and future government surpluses.”

Markets don’t seem to act that way, though.

When gold and silver crashed last week, the move was attributed to the news that the next Fed Chair will be Kevin Warsh, who has some history of being hawkish on interest rates and is opposed to quantitative easing (a.k.a. money printing).

This reflects monetarist thinking: We assume that inflation is caused by central banks that keep interest rates too low and print too much money.

In Sargent’s telling, however, the monetary policy that Mr. Warsh will soon guide has very little to do with the demand for US government debt or the value of the US dollar.

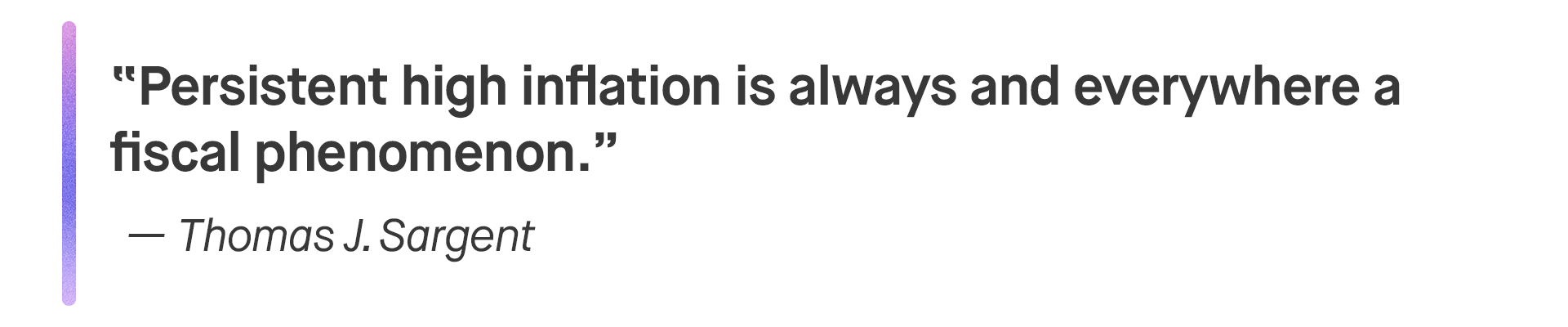

Instead, he says inflation is ultimately a fiscal phenomenon: “With a profligate fiscal policy,” Sargent writes, “it is impossible for a monetary authority to sustain low inflation because the intertemporal government budget then implies that the monetary authority must sooner or later impose a sufficiently large inflation tax to finance the budget.”

Or, to reverse Milton Friedman’s famous adage, “Persistent high inflation is always and everywhere a fiscal phenomenon.”

To demonstrate this empirically, Sargent studied how the hyperinflation that plagued Europe in the 1920s was eventually resolved in several countries.

“Once it became widely understood that the government would not rely on the central bank for its finances,” Sargent found, “the inflation terminated and the exchanges stabilized.”

Makes sense, sure.

But here’s the revelatory detail: “In each case the note circulation continued to grow rapidly after the exchange rate price level had stabilized.”

After prices had stabilized!

To end hyperinflation, then, governments didn’t have to stop printing money. They only had to convince markets they would someday collect enough in taxes to retire their debt.

Taxes, of course, are fiscal policy, not monetary.

Writing in 1982, Sargent reported that people dismissed his findings because the incidents he studied were “so extreme and bizarre that they do not bear on the subject of inflation in the contemporary United States.”

In 2026, with the federal government running a $2 trillion deficit even when tax receipts are high, his findings feel increasingly relevant.

Will the US government ever run surpluses again?

It doesn’t seem like it.

And yet, inflation is only 3%, and there are willing buyers of seemingly unlimited amounts of US government debt. The money-borrowing machine created in 1788 works far better than the founding fathers ever could have imagined.

But Sargent’s work suggests there are limits — and the booming price of gold and silver suggests more and more people think the US government is pushing them.

If still more investors get the sense that the government won’t ever balance its budget, US government debt will have to be repriced.

The net present value of surpluses that will never happen is zero.

Crypto’s premier institutional conference is back this March 24–26 in NYC.

Don’t miss SEC Chairman Paul S. Atkins’ keynote on Day 1.