- The Breakdown

- Posts

- 🟪 This week’s guaranteed winner: Prediction markets

🟪 This week’s guaranteed winner: Prediction markets

Prediction markets can only be efficient if people think they are inefficient

Byron Gilliam

November 05, 2024

Brought to you by:

“What I needed to get ahead was to compete against idiots. Luckily, there’s a large supply.”

— Charlie Munger

This week’s guaranteed winner: Prediction markets

This weekend, a poll of 808 Iowans by the highly regarded pollster Ann Selzer spiked Harris’s odds of winning the Hawkeye State by nine percentage points, as measured by Nate Silver’s election model.

Harris remains an extreme long shot in deep-red Iowa with just a 17% chance to win, but the poll also moved Harris’s Polymarket odds of winning the whole election by five full percentage points.

That attention-getting swing seemed like a disproportionate reaction to a poll of just 808 souls, and has since been reversed.

But the volatility added to a growing perception that Polymarket is less about predicting the election and more about gamifying it.

This, however, is the best possible advertisement for prediction markets — and also what makes them work.

Whatever the outcome this week, prediction markets are sure to take some flak for being “wrong” because it had Trump’s odds ping-ponging from 66% to 45% to 66% to 55% — a level of volatility that seemed to be well in excess of how much the polls were moving.

But prediction markets are, well, markets, not models, and markets require price discovery: Odds have to move far enough in one direction that enough people think they are wrong enough to be worth making a bet in the other direction.

There is no other way to do this — if everyone thinks a market’s odds are exactly right, no one would bet and there would be no market.

In other words, prediction markets can only be efficient if people think they are inefficient.

Fortunately, Polymarket’s big swings have made people think it’s inefficient.

This perception has attracted a lot of “fish,” like the big bettor that moved Polymarket odds to an extreme in Trump’s favor — and the fish, in turn, have attracted “sharks,” the professional (or just better-informed) gamblers that then moved the odds back in the direction of polling models.

This volatility is not just Polymarket bettors being silly, however.

One of the big takeaways from this election cycle, I think, is that polls are imprecise and election odds are therefore highly tradeable.

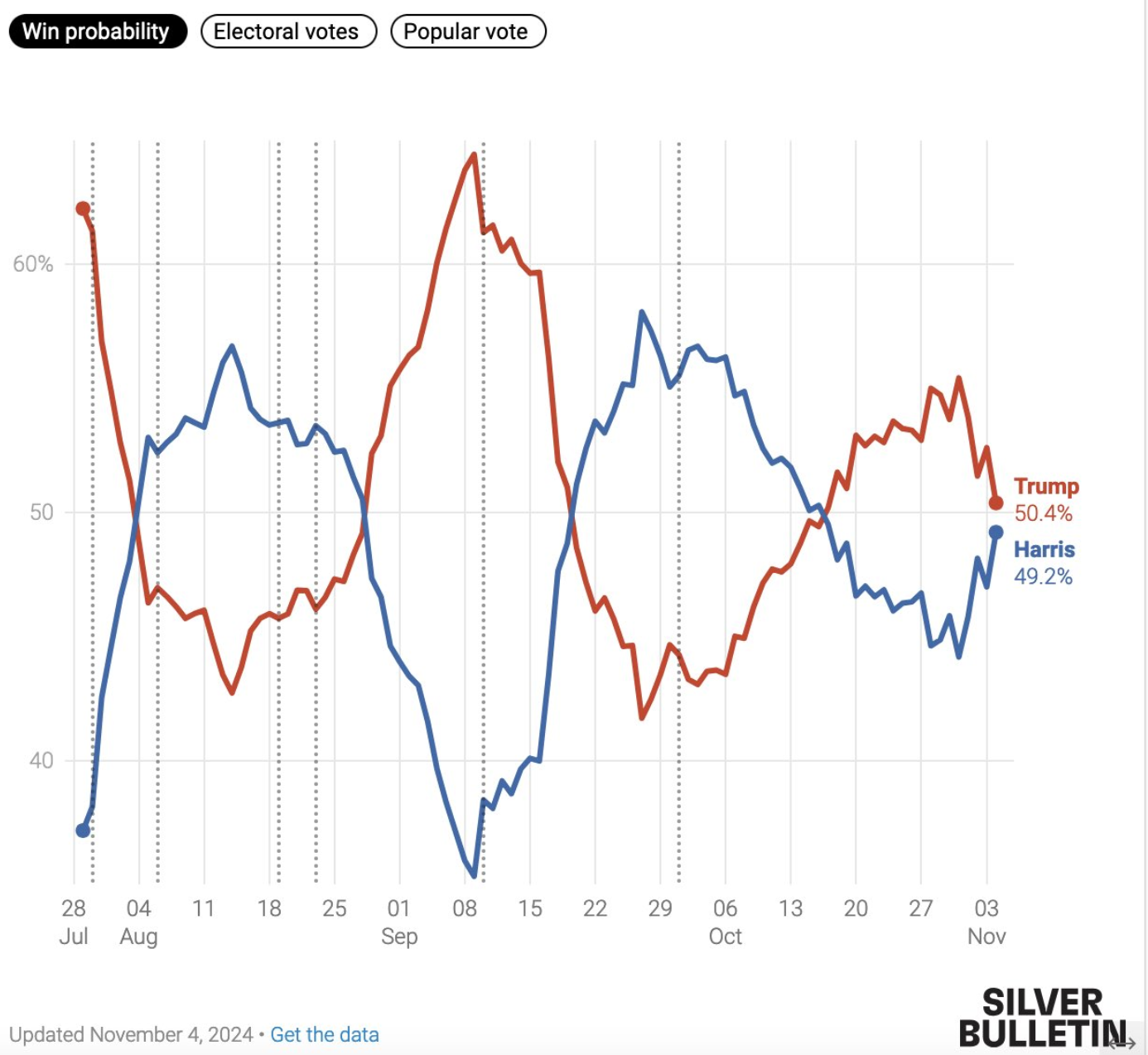

This chart of Nate Silver’s win probabilities, for example, is a trader’s dream:

The inverse correlation between the two lines is of course mechanical (and the Y-axis is truncated for dramatic effect), but traders love mean reversion and this has been a highly mean-reverting market (even down to the last hours with odds now reverting back in Trump’s favor).

The late volatility, especially, has been a reminder that you don’t have to wait for the binary outcome of a prediction market to make a profit — you can just trade it.

(I’d also note that because the upside is capped at $1, there is no risk of getting stopped out on a short position — every short seller’s dream.)

Polymarket has attracted over $3 billion of election wagers and after watching all the volatility, I expect it’ll attract many more next time.

In fact, Trump vs. Harris has been so eventful for election bettors, I predict there will be a surprisingly active market for the midterm elections in 2026.

Much of this will be bets made for entertainment purposes, but some of it will serve a purpose.

With increased liquidity, hedge funds will be able to pair bets in prediction markets with positions in crypto or equities: long Kamala to hedge a long BTC position, for example.

That will inject another dose of volatility, which will, in turn, attract more fish that in turn attract more sharks — a virtuous cycle that will make prediction markets both more efficient and more profitable.

The other big winners here are pollsters, who stand to have a much larger audience for their polling results next time around.

We’ve all learned that, for example, an Ann Selzer poll of 808 people in Iowa can be a market-moving event, so we’ll all be paying extra attention to whatever she says next.

This is a good thing.

People have been fretting that our perception of an election can be easily manipulated by moving prediction markets, but the media has long been flooded with partisan polls that attempt to do the same thing.

The societally beneficial result of prediction-market volatility is that it teaches us to resist manipulation.

There’s never been much reason to get into the minutiae of polling before, but now — in large part thanks to prediction markets — we’ve learned about “herding” (in which pollsters adjust their polls to match all the other polls), “weighting on recalled vote” (which may risk overcorrecting polling results), which pollsters to listen to (Ann Selzer), and which ones to ignore (most of them).

As a result, election betting — a negative-sum activity for bettors — might turn out to be a positive-sum activity for society because of 1) the better information it offers and 2) the incentive it provides to educate ourselves.

That won’t be enough for those who worry that Polymarket is having an influence on the outcome of the election it's meant to only be predicting.

That is probably an unfalsifiable claim, so I imagine both sides may try to manipulate markets in their direction next time around.

This, too, would be great news for the prediction markets.

The Frenchman who pushed Trump to 66% on Polymarket was probably not trying to manipulate the market, but it certainly looked like he was.

With that in mind, when there’s a similarly big move in 2028, people will be quick to take the other side — what better bet is there to take than the other side of someone who’s betting for non-economic reasons?

Those non-economic bettors will attract new participants to prediction markets like a deep-pocketed fish attracts sharks to a poker table.

This is what makes prediction markets efficient — but not too efficient.

Political prognosticating is a minefield of confirmation bias and everyone seems to lose about 40 points of IQ when they attempt it (myself included).

Markets on politics should therefore offer us an unusual number of opportunities to bet against dumb people (or, better yet, otherwise smart people temporarily struck dumb by politics).

So, if Charlie Munger is correct in that the way to get ahead is to compete against idiots, know that prediction markets may be the best place to find them.

Erratum: Speaking of people doing dumb things, I incorrectly stated yesterday that it cost an unreasonable 20% in fees to trade the PNUT memecoin on Raydium and suggested that this is unsustainable. Unfortunately, my mental math was off by a factor of 10: It costs just 2% — which seems both reasonable and sustainable. My apologies to Raydium! (And also to Peanut the Squirrel, RIP.)

Brought to you by:

MANTRA Chain’s mainnet has officially launched, marking a significant step towards their vision of becoming the preferred ledger of record for tokenized RWAs. While features of the Mainnet will continue to develop, users can already access the following notable activities:

Bridge $OM from ERC-20 to Mainnet to gain access to future RWA drops

Stake $OM to help secure the network and earn onchain staking rewards

Earn KARMA by completing new missions on mainnet

While 2024 has been a landmark year for MANTRA, including strategic collaborations with UAE real estate giant MAG and Zand Bank, the launch of the Mainnet will open the door for significant movement in the real-world asset space.

Unlocking Undercollateralized Lending

Wildcat Finance co-founder Laurence Day joins the episode to discuss undercollateralized lending and RWAs in DeFi, the impacts of capital efficiency and how privacy comes into play.

Listen to Bell Curve on Spotify, Apple Podcasts or YouTube.

Americans doing some last minute research by Googling "who is running for president" on Election Day

— Hunter📈🌈📊 (@StatisticUrban)

4:34 PM • Nov 5, 2024

GS: Under our baseline assumptions, debt-to-GDP rises to 130% by 2034 from 97% currently

— Mike Zaccardi, CFA, CMT 🍖 (@MikeZaccardi)

7:12 PM • Nov 5, 2024