- The Breakdown

- Posts

- 🟪 Stuck in the m(ud)

🟪 Stuck in the m(ud)

What to watch for next week's FOMC

June’s big FOMC meeting

Next week is FOMC Day, and it feels like it’s going to be a highly contentious one.

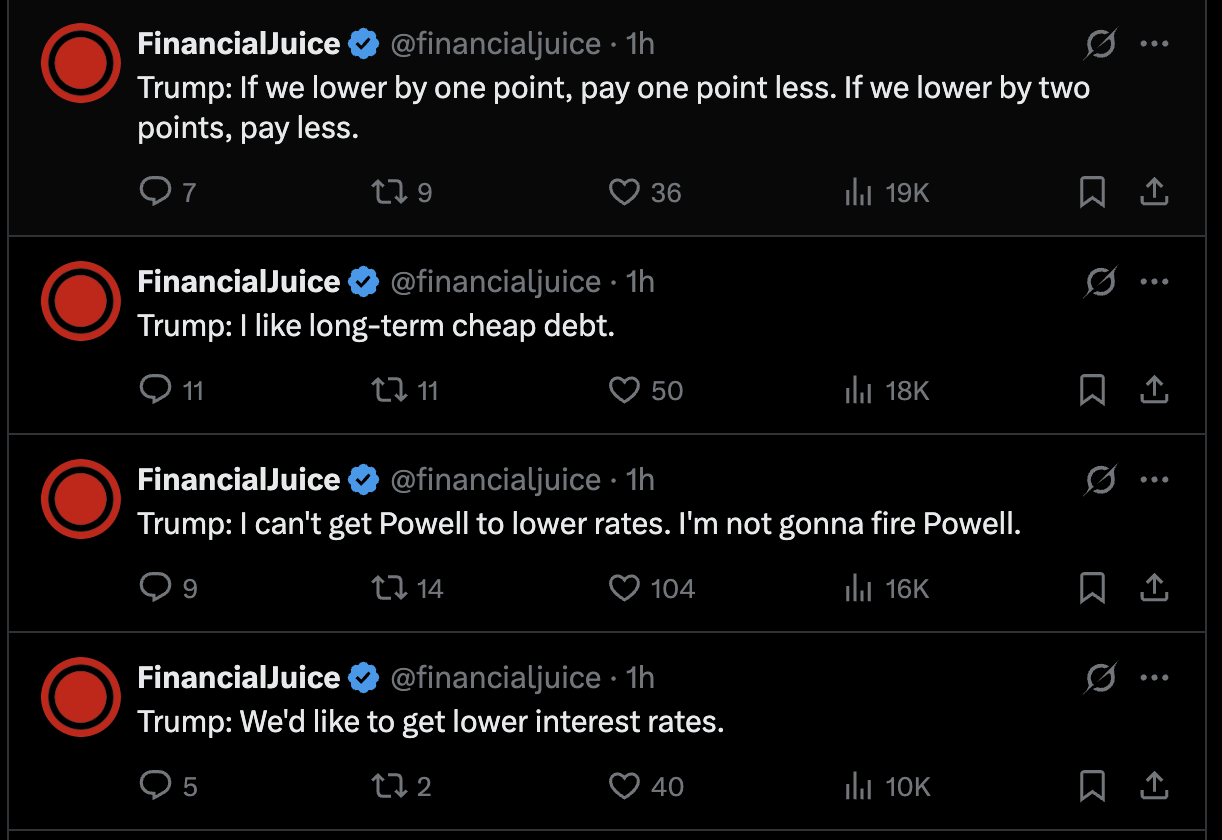

On one hand, you have President Trump pressing Chair Jerome Powell to cut rates by 100bps as soon as possible:

On the other hand, you have the FOMC towing the line that they’re in a “wait-and-see” mode. This is because they don’t want to react in either a dovish or hawkish direction until they have a better idea of where the tariff policy will net out.

However, doing nothing is also a policy decision.

Currently, there’s a 97% implied probability for the Fed to pause, so there’s almost no expectation for it to cut next week:

However, next week will also have a dot plot meeting wherein we’ll receive an update on the Fed’s summary of economic projections (SEP). If the Fed wanted to signal a dovish tilt, the SEP is what will be used to signal that.

To gauge whether that will be the case, let’s take a look at some of the most recent economic data that will drive the FOMC’s thinking next week.

The Fed has insisted on being data dependent while trying to navigate an inflation rate above its 2% target for multiple years now. Looking at the Taylor Rule — a historically accurate model for gauging how tight or loose monetary policy is based on the Fed’s dual-mandate of maximum employment and stable prices — the Fed should be cutting right now, but isn’t:

Labor

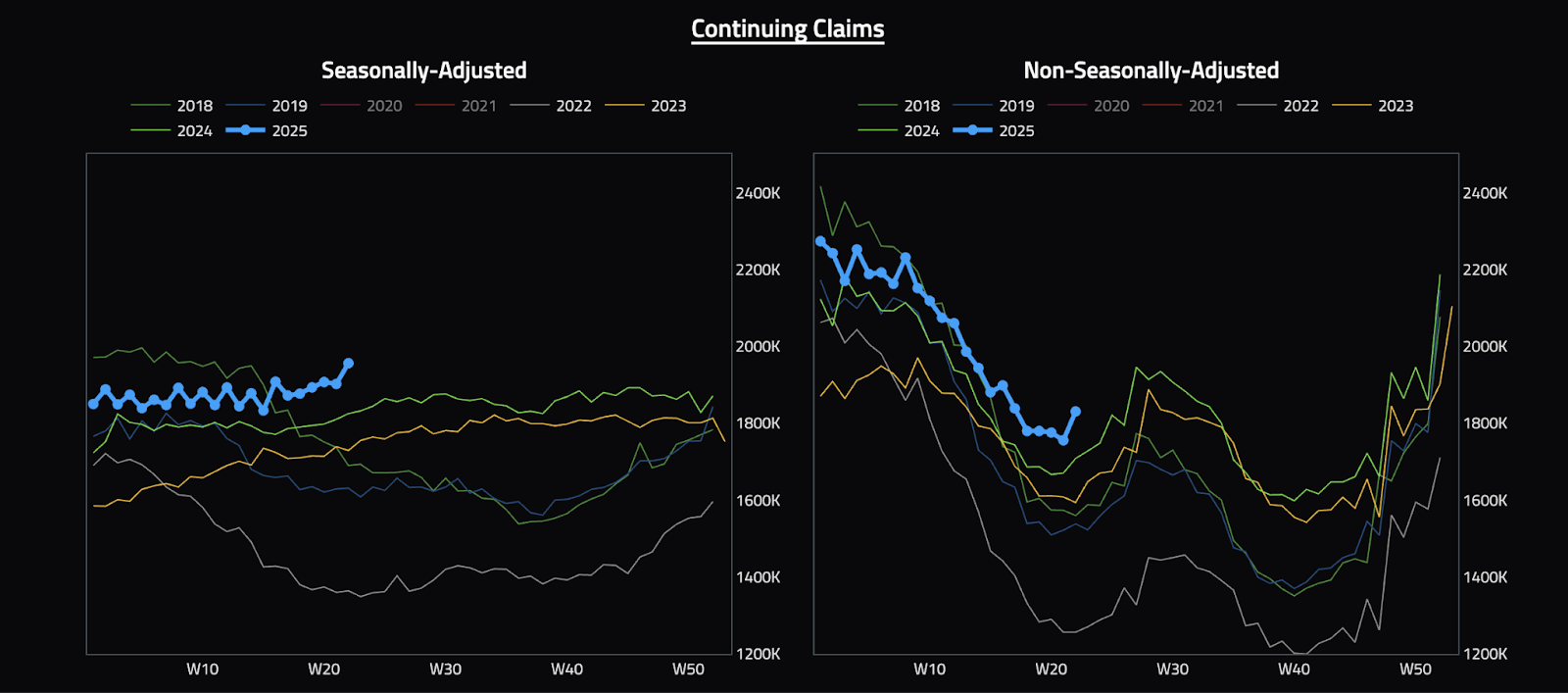

This week we saw a huge uptick in continuing jobless claims, emphasizing just how hard it is to get a job when you lose one.

Although we have not seen the same surge in the unemployment rate nor for initial jobless claims, this uptick further validates how little companies are hiring right now. But they’re not at the point of layoffs, either. We are in a regime of attrition right now.

This is a precarious place to be. By the time the labor market deteriorates to the point where we see a surge in the unemployment rate and negative payroll numbers, the Fed will be very behind with respect to a Taylor Rule-like model, as shown earlier.

Inflation

The reason the Fed isn’t pre-emptively cutting rates from the perspective of the labor market is due to a concern about tariffs passing through into higher inflation — thus questioning the Fed’s mandate of stable prices.

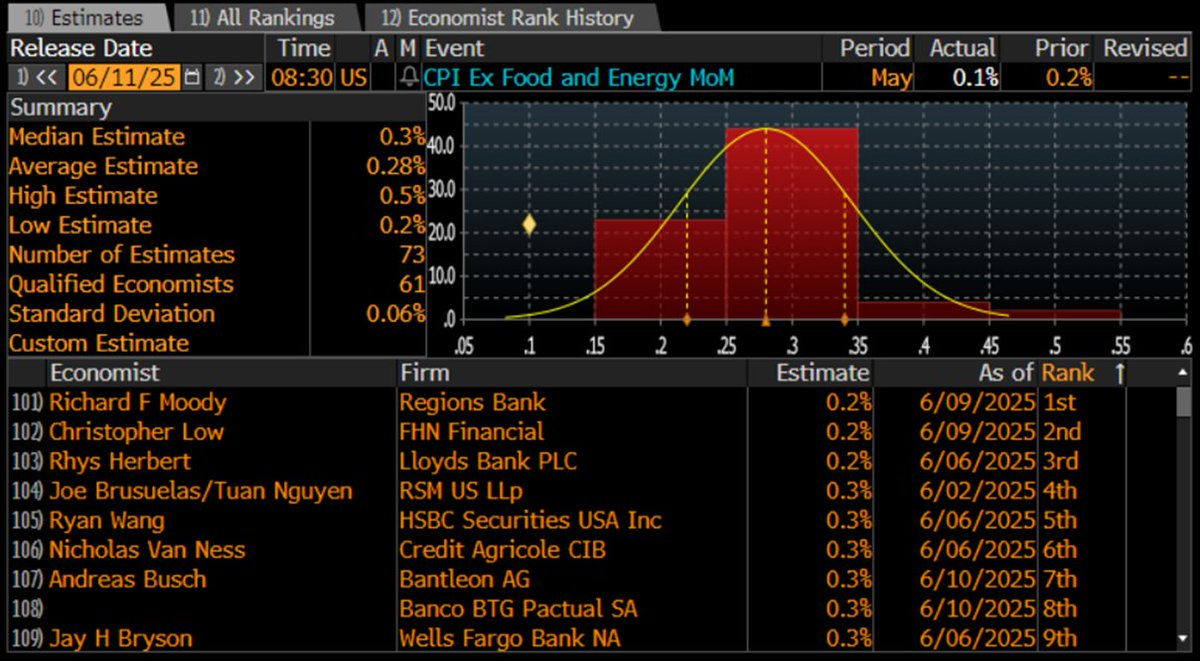

This week’s CPI data, however, calls into question how large the impact of tariffs will be on inflation.

Core CPI came in at 0.1% month over month, a huge downside miss that not one economist out of the 73 surveyed anticipated:

On its own, this would be enough for the Fed to sigh in relief that inflation is on its way to the 2% target.

The issue, however, is inflation expectation in light of surging tariffs:

After being burned too many times in cutting before it became clear that inflation was on its path to 2%, the Fed does not want to make the same mistake.

Putting it all together, we have a unique situation with a significant risk of a potential policy error.

By sitting on their hands and speculating on future data as opposed to reacting to the data that we are getting today, FOMC members are effectively making an intentional decision to be as late as possible in their reaction function.

That’s not a great place to be in.

Brought to you by:

ZKsync is accelerating institutional blockchain adoption and the rise of tokenization. Institutions choose ZKsync to move tokenized assets securely across enterprises while preserving privacy and governance.

With gasless transactions, seamless onboarding, and scalable ZK infrastructure, enterprises can transfer financial products and data privately using ZK Stack — an open-source, trustless blockchain platform designed for speed, low costs, security, and interoperability without sacrificing control.

By Jack Kubinec |  |

|

By Kate Irwin |  |

|

|

Less than 3 weeks away!

Hear from leaders like Peter Todd, Joseph Lubin, and Joshua Tobkin — and be a part of our largest hackathon yet with over $100K+ on the line.

Hackers enter free; every minute counts.

June 24-26 | Brooklyn, NY