- The Breakdown

- Posts

- 🟪 Thursday links

Thursday links: Anarchy, crime and stablecoins

What would Timothy May think of “Crypto Week”?

If the OG cypherpunk and author of The Crypto Anarchist Manifesto were here to read the statement from the House of Representatives — itself a kind of manifesto — declaring this to be Crypto Week, I expect he’d have mixed feelings about it.

He’d certainly object to the idea of a “Crypto Czar,” appointed by the president of the very government whose authority he hoped to undermine.

(“Cryptologic methods,” he believed, would undermine “government interference in economic transactions.”)

On the other hand, he’d be pleasantly surprised, if not shocked, to learn that the US government is banning itself from issuing a central bank digital currency.

But he’d be most surprised to learn that the US government’s stated aim is to accelerate the adoption of cryptocurrency.

“The State will of course try to slow or halt the spread of this technology,” he wrote in the manifesto.

I guess not!

He’d have reservations, sure.

Markets, he thought, should self-police via mathematics, not laws, and that’s not what’s being promoted this week.

The CLARITY Act, for example, applies the Bank Secrecy Act (public enemy No. 1 for financial cypherpunks) and other KYC/AML rules to most intermediaries.

But “intermediaries” is the key word there: The Act also preserves the right to hold and use digital assets in personal wallets.

May’s vision was that “two persons may exchange messages, conduct business, and negotiate electronic contracts without ever knowing the True Name, or legal identity, of the other.”

Insert an intermediary, though, and even May might think the government is right to regulate.

What might shock him most, though, is some of the rhetoric.

“Ensuring the future of the digital economy,” Representative Tom Emmer says in the official House statement, “reflects our values of privacy, individual sovereignty and free-market competitiveness.”

Privacy and individual sovereignty are crypto-anarchist values, too.

In that sense, Crypto Week feels like a surprising vindication for May and the community of cypherpunks he inspired (Bitcoiners included).

He would, however, take note of the multiple mentions of “protecting consumers” in the House statement and see that as evidence that the State is not surrendering its surveillance powers anytime soon.

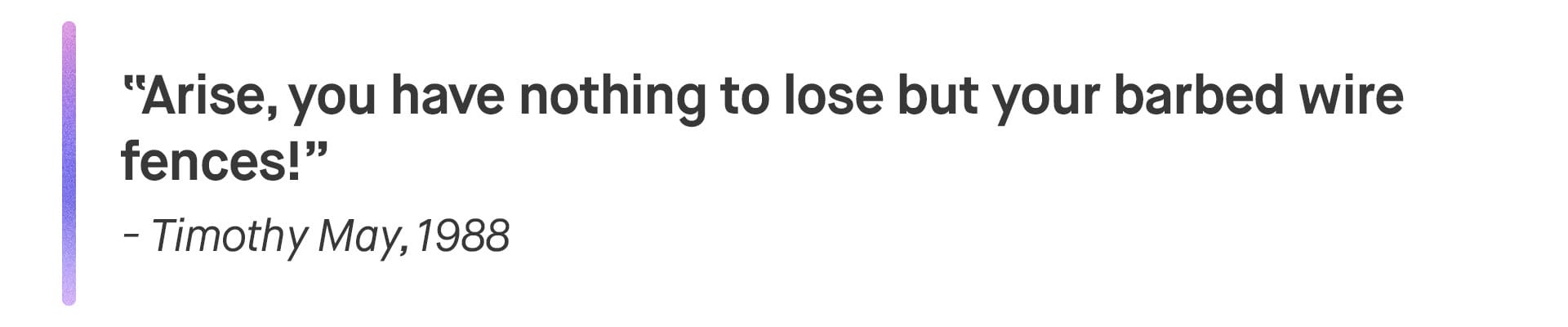

May ends his manifesto with a vivid image: governments fencing in citizens like livestock on a barbed-wire ranch.

Even after Crypto Week, I’m sure he’d say the fences remain up.

In its latest report on crypto crime, onchain analytics firm Elliptic reports that the crypto ecosystem is “increasingly being exploited by illicit actors.”

Specifically, it estimates that the all-time total of “cross-chain criminal and high-risk” crypto transactions has risen to $21.8 billion, including over $2.17 billion in the first half of 2025.

Elliptic attributes 12% of the total to North Korean hackers (which, I imagine, is how Kim Jong Un paid for his new beach resort).

Blockchains remain transparent, but the report suggests that following crypto money trails may be getting harder: 20% of money laundering actions, it notes, move crypto across more than 10 blockchains.

The result is that crypto continues to play its role in the disturbing rise of “industrial-scale fraud.”

The most recent example came this week, when the DEA announced that it had seized more than $10 million in cryptocurrency from Mexico's Sinaloa cartel, in raids that also netted massive quantities of fentanyl.

(Tariffs on fentanyl still aren’t high enough, I guess.)

Timothy May would be unperturbed. “Various criminal and foreign elements will be active users of CryptoNet,” he wrote. “But this will not halt the spread of crypto anarchy.”

But the crypto industry still needs to do more to police itself.

After researching the ByBit hack in March, the onchain sleuth ZachXBT wrote in his Telegram channel that the industry “is unbelievably cooked when it comes to exploits/hacks.”

Attempting to retrieve funds from the ByBit hack was “eye-opening,” he wrote, noting that “several ‘decentralized’ protocols have recently had nearly 100% of their monthly volume/fees derived from [North Korea] and refuse to take any accountability.”

Centralized exchanges, he added, are even worse because they take “multiple hours” to respond to his inquiries, which is far too slow: “It only takes minutes to launder.”

The industry, he warned, is so negligent in policing itself that it risks inviting much tighter government regulation.

Maybe not this week, though.

Lee Reiners takes exception to all of the “techno-utopian soundbites” DC politicians have been using to promote stablecoins recently.

The idea that stablecoins will extend the reign of the US dollar as the world’s reserve currency has been repeated so often that it’s become received wisdom both in and out of crypto circles.

But Reiners takes the opposite view, arguing that stablecoins will have “no impact on the dollar’s status as a global reserve currency.”

“By imposing stricter requirements,” he argues, the GENIUS Act “could actually diminish dollar dominance if it drives stablecoin users and issuers toward non-USD alternatives that remain unregulated or offshore.”

In other words, he thinks stablecoins will lose their appeal for “bad actors” once they’ve been regulated.

(I doubt it, though. They’ll still be dollars that are not subject to KYC checks.)

But even if dollar-pegged stablecoins are used more frequently, he continues, “that growth would likely cannibalize existing dollar instruments…rather than expand the overall footprint of the dollar.”

I still think stablecoins could help at the margin by encouraging more international transactions to be done in dollars, basically.

But if the US government so debases the dollar that people question its value, stablecoins won’t be nearly enough to save it.

The one thing that Citi is truly good at is global payments: Its Trade and Treasury Services business, which moves money around for large customers, is the world’s biggest.

So I think it’s telling that Citi has advanced plans to issue a stablecoin and integrate it into its global payments offering.

CEO Jane Fraser noted that only 6% of stablecoin volume is related to payments, which she attributes to the high cost of on- and off-ramping them into and out of fiat — costs that add up to 7%, she says.

Citi expects to change all that, offering to move stablecoins across borders and in and out of fiat at near-zero cost, she implied (“without incurring that transaction cost”).

She also suggested, however, that it's more likely to use tokenized deposits than stablecoins.

Tokenized deposits might prove difficult for the crypto industry to compete with.

The GENIUS Act, Fraser added, levels the playing field for banks to get involved in digital assets and Citi is enthusiastic about it.

Of that, I’m certain Timothy May would not approve.

Brought to you by:

Trade stocks or crypto fully onchain all from your pocket with Helix Mobile.

Helix is the fastest growing decentralized order book exchange with over $13.5B in year-to-date volume!

Helix Mobile enables you to trade stocks like $HOOD, $TSLA, and $CRCL or crypto like $BTC and $ETH onchain with up to 50x leverage from your smartphone. Download now!

By Jack Kubinec |  |

By Felix Jauvin |  |

By Casey Wagner |  |

By Casey Wagner |  |

|

Brought to you by:

Katana is a DeFi chain built for higher sustainable yield and deep liquidity. It concentrates liquidity into core applications and channels the chain’s revenue back to the users.

Creating a better DeFi experience that benefits the active users on the chain.

Earn KAT tokens: Pre-deposit with turtle club