- The Breakdown

- Posts

- 🟪 Thursday mailbag

Brought to you by:

“You make most of your money in a bear market, you just don’t realize it at the time.”

— Shelby Davis

Thursday bearish mailbag

Q: Is the cycle over?

In the sense that it will take something new to get investors re-interested in crypto, I think it is.

Bitcoin and ether ETFs, which started the bull market, are now seeing big outflows.

The idea that the US government will soon be buying bitcoin is fading.

The LIBRA token launch has exposed memecoins as an insiders’ game.

President Trump’s memecoin and his proposal for a crypto strategic reserve are widely derided, even within crypto.

The Trump family DeFi project has been exposed as a Trump family grift.

Mostly, though, there’s just a distinct lack of FOMO at the moment.

It can’t be a crypto bull market without the fear of missing out and there doesn’t seem to be anything to fear at the moment.

Q: What’s the next narrative?

I’m hopeful that the next narrative will be productive, cash-flowing protocols.

One attendee at ETHDenver, for example, found that “almost everyone agrees that the future is protocols and tokens backed by real revenues and cash flows.”

That could make for the best kind of crypto bull market, where traditional investors start fearing that they’re missing out on the cash flows being generated by protocols.

It’s also the most difficult kind of bull market, because someone has to build said protocols, which is a lot harder than launching a memecoin on pump.fun.

Q: What did we accomplish this cycle?

The infrastructure is better: Memecoins have stress-tested the chains and it’s now a lot cheaper and faster to transact.

A lot of traditional investors have bought into bitcoin’s “digital gold” narrative.

And the industry helped elect the first crypto president.

But I’d argue that the defining feature of this cycle is that its biggest winners are the three owners of the privately held memecoin factory pump.fun.

Pump.fun has generated $528 million of revenue in its one year of existence (nearly all of which is profit, I’m guessing).

It’s good that they stress-tested the chains for us, but let’s hope the next cycle’s big winners are rewarded for building something a bit more productive.

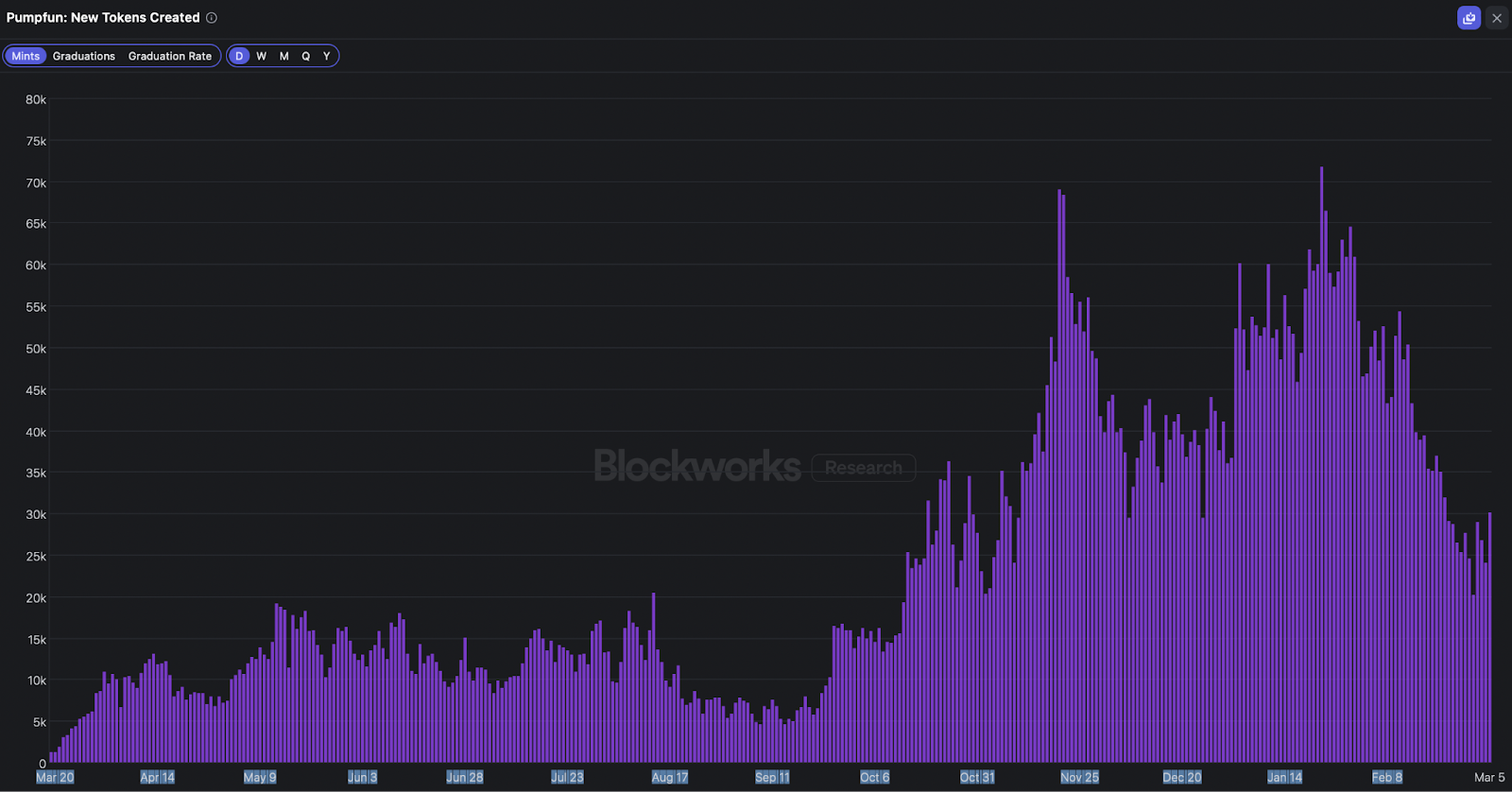

Q: Are memecoins over?

At the start of this cycle, you could still believe that Peanut the Squirrel would be the next PEPE or that Fartcoin would be the next DOGE.

I’m not sure that will be believable for much longer.

Doge and Pepe both feel like relics of a pre-pump.fun era when memecoins were not trivially easy to launch.

Post pump.fun, it seems likely that the memecoin manias will be increasingly ephemeral.

On the other hand, memecoin sentiment is about as low as it can get and people are still creating and buying them in significant numbers:

There are roughly 30,000 new memecoins created on pump.fun every day and 0.8% of them still attract enough buyers to “graduate” to the decentralized exchange Raydium (down from a high of 1.8%).

Perhaps most tellingly, pump.fun collected $1.3 million in revenue yesterday.

It’s not the revenue anyone was hoping for, but it’s the revenue we deserved this cycle.

Q: Should memecoins be securities?

They might not strictly qualify according to the Howey test, but the SEC’s new explanation for why memecoins are not securities makes me think that they should.

“Memecoins typically are purchased for entertainment, social interaction and cultural purposes,” the SEC explained in a staff memo last week. “In this regard, memecoins are akin to collectibles.”

But no one “collects” memecoins.

If they did, they’d only need one of each for their “collection” — which no one would ever want to see. (Or 0.0000001 of each, for that matter.)

Instead, people buy memecoins for the same reason they buy securities: to make money.

This, in my opinion, makes memecoins functionally equivalent to stocks — and things that are functionally equivalent should also be regulatorily equivalent.

(Yes, “regulatorily” is a word — I looked it up so I wouldn’t have to rewrite that sentence.)

If crypto investors insist on treating memecoins like securities, they should probably be regulated like securities, too.

Q: How hard is it to launder crypto?

Not as hard as people thought, it seems.

The CEO of Bybit shared this week that about 20% of the $1.4 billion of ETH that North Korea stole from his exchange has “gone dark” and that only 3% has been “frozen.”

That 20% number will keep rising and the 3% number is likely to stay, well, frozen — because all of the stolen ETH has already been swapped for BTC, where it’s still traceable but easier to off-ramp and less likely to be frozen.

This is happening faster than anyone seemed to expect — and that suggests the industry hasn’t made much, if any, progress in deterring money launderers.

Crypto remains the best money to steal.

Q: Does the president need Congressional approval for a strategic crypto reserve?

It’s hard to say because this doesn’t seem to be a matter of settled law.

But the strategic petroleum reserve was created by an act of Congress, so it seems like a strategic bitcoin reserve would need to be, too.

I’m guessing that Senator Lummis would concede as much, because her proposed Bitcoin Act implies that Congressional approval is necessary (why ask permission if you don’t need it?).

Lummis also noted recently that her proposal was not yet getting the support it needed in Congress.

President Trump might try to bypass Congress and simply order the US Treasury to start buying, but I imagine that would be challenged in court.

If the Fed wanted to buy bitcoin, on the other hand, I’m sure it could — it seems to buy whatever it wants in a crisis — but I’m also sure it doesn’t want to.

Bitcoin might prove to be a rare instance of the president not getting what he wants.

(We might find out after Friday’s White House crypto summit.)

Q: Will Congress eventually approve a bitcoin strategic reserve?

It’s looking less likely.

At the state level, Wyoming, Montana and both the Dakotas have rejected proposals to create bitcoin reserves (wisely, in my opinion).

If states as Trump-aligned as those four aren’t interested in buying bitcoin, I can’t imagine the US Senate will be, either.

Q: Should capital gains on crypto be tax free?

President Trump has proposed making crypto gains tax free, but this seems at odds with his desire for the government to be long crypto via a strategic reserve.

The government has an equity stake in everything, via taxes.

If the president believes it’s important for US taxpayers to own crypto, giving up its share of everyone’s crypto gains seems like the exact opposite of what he should be proposing.

Q: Should TikTok be onchain?

Reddit co-founder Alexis Ohanian thinks it should be: “I'm officially now one of the people trying to buy TikTok US," he announced this week, “and bring it onchain.”

But I don’t think there’s any reason to because data isn’t oil, it’s sand, as Tim O'Reilly explained: Unlike oil, data is only valuable in aggregate quantities, similar to how sand is valuable in large amounts but not individually.

Or, as Benedict Evans writes, data isn’t really anything at all.

Your TikTok followers, for example, only have value within the context of TikTok — they wouldn’t be worth anything to you anywhere else.

So, onchain TikTok, unfortunately, is not the thing to get the next crypto bull market going.

Brought to you by:

Good reasons NOT to stake your SOL: Wanting full custody of your crypto (& sole access to your wallet). Not having enough time in the day to figure out which validator has the best rewards rates (or enough bandwidth to constantly chase higher APYs).

All the more reason to try Marinade Native.

Non-custodial Solana staking, directly from your wallet, automatically adjusted to earn the most competitive staking rewards rates. No smart contracts, no liquid staking tokens, and no extra work.

Hivemind: Macro News Bearish, Crypto News Bullish and What We’re Bidding

The Hivemind team discusses the effect of crypto scams and grifting on sentiment. Get insights on whether the Trump admin is actually better for crypto and the key macro factors driving markets.

Listen to Empire on Spotify, Apple Podcasts or YouTube.

Investors, policymakers, and industry leaders — make the calls that shape the future of digital assets. 3 weeks out, the room is filling up.

Mohamed El-Erian (Allianz) on how institutional capital is navigating uncertainty.

Nathan McCauley (Anchorage Digital) on the state of crypto banking and custody.

Jessica Peck (US Department of Justice) on where enforcement is headed next.

Rep. Tom Emmer (R-MN) on the regulatory fights that will define the industry.

📅 March 18-20 | NYC

Here we go.

This is how you start a nation’s strategic reserve, by the people for the people.

Japan is mobilizing to play their own tariffs war: subsidize non-US financial asset ownership.

— Jeff Park (@dgt10011)

12:42 PM • Mar 6, 2025

What we're seeing today -- at the ECB, in Germany, and in China -- is that the instant reaction to any sort of economic volatility is to print money. This is why all roads lead to bitcoin.

— Matt Hougan (@Matt_Hougan)

2:20 PM • Mar 6, 2025